- Updated:

- Published:

Global iGaming acquisition leaders vs global revenue leaders 2026

betPawa dominates the APS metric in emerging markets, while US-facing brands command larger CEB. Only two operators bridge both worlds.

Blask data reveals an interesting divide: the brands dominating APS are rarely the same ones leading in CEB. It’s a classic trade-off between volume and value. This article breaks down the top 10 iGaming operators across both metrics, comparing these market leaders to uncover the hidden global and local patterns shaping the industry today.

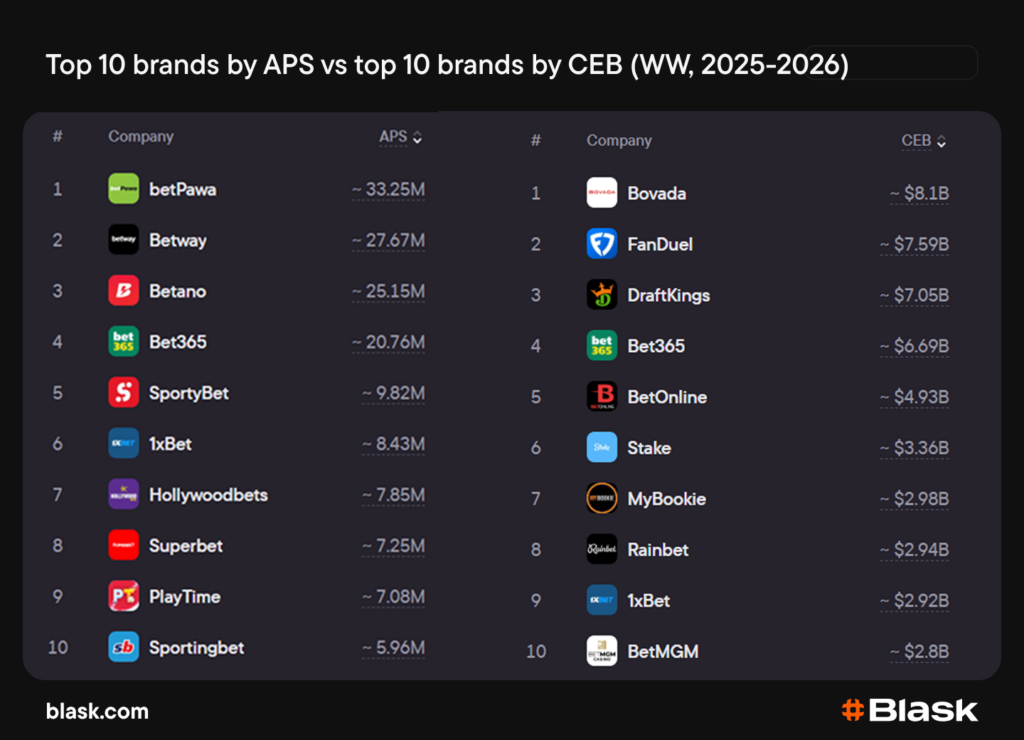

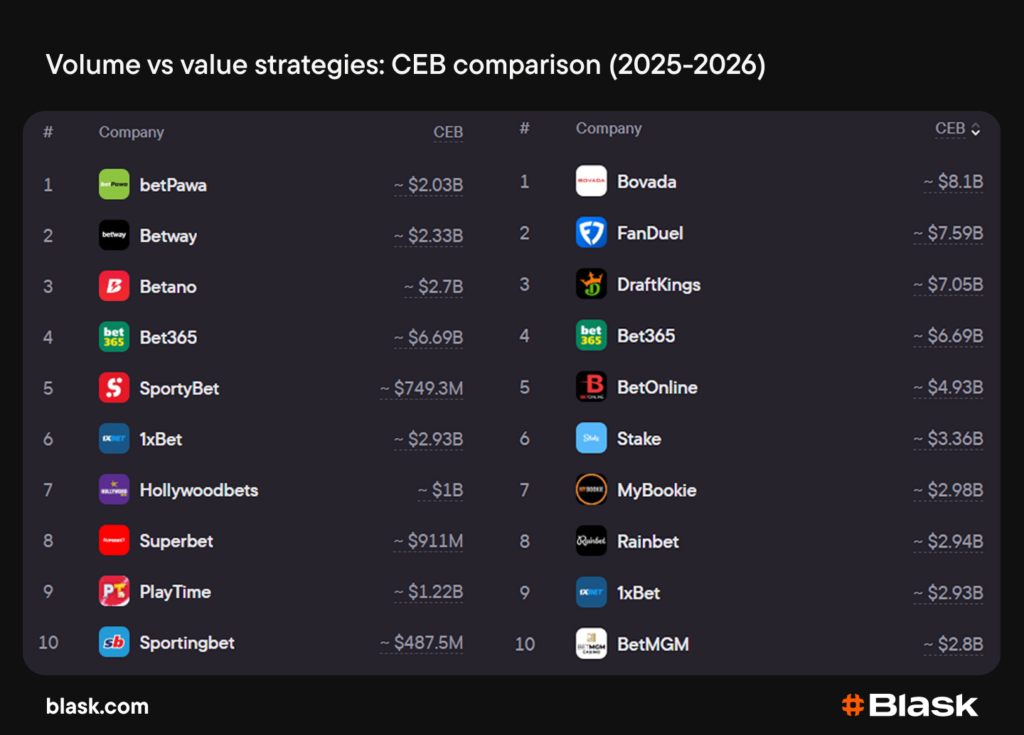

Top brands by APS vs top brands by CEB

The two rankings share just two names: Bet365 and 1xBet. Most brands from the APS leaderboard work in emerging markets with a huge population but low-stake gambling. CEB leaders work in expensive markets, where stakes are usually higher.

APS leaderboard: African brands at the top

In this ranking, African and Latin American markets dictate the pace.

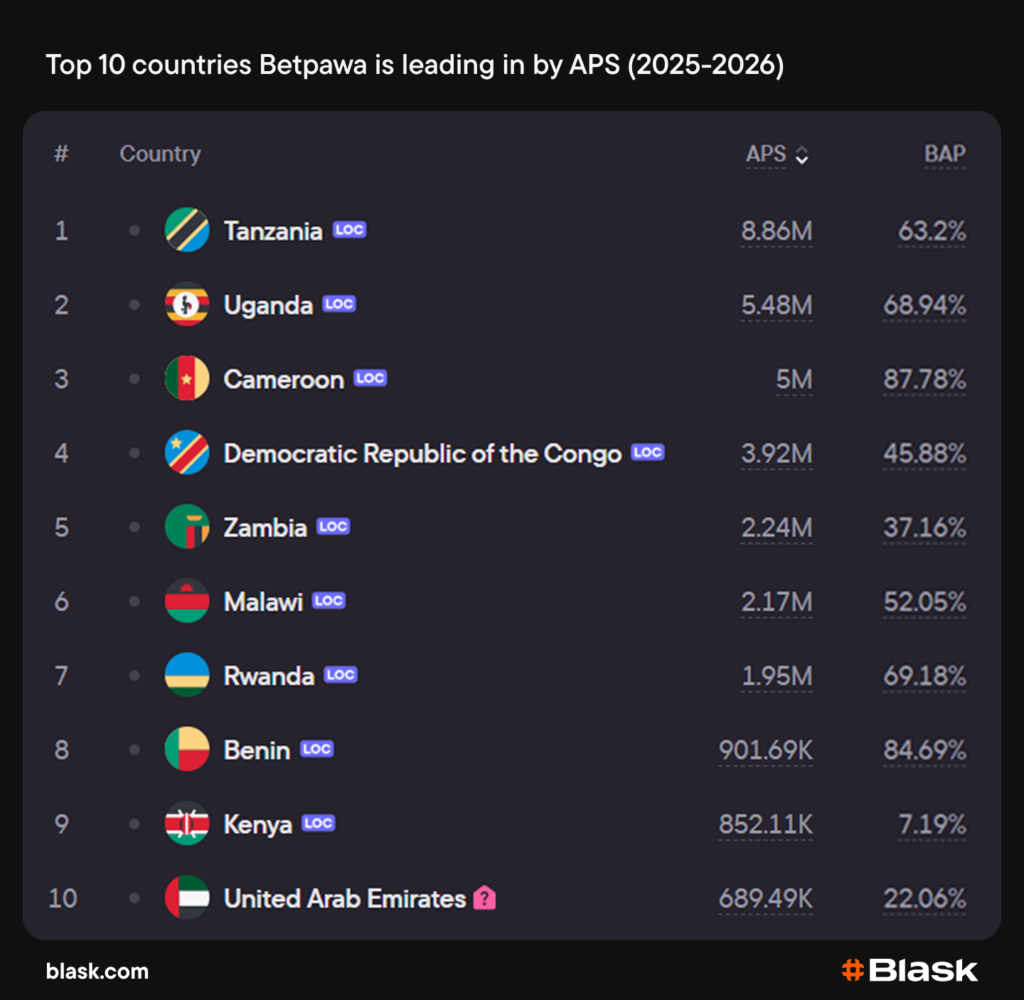

betPawa stands as the undisputed leader, generating 33.25M predicted signups across 34 countries. This creates an acquisition density that rivals struggle to match. Brand’s leading markets — Tanzania, Uganda, Cameroon — reflect a focused African expansion strategy.

Betway (~27.67M) and Betano (~25.15M) focus on high-growth regions: Africa and Latin America respectively.

APS leaders share a common playbook: target high-population GEOs, even if average stakes remain low. The top spot in this economy is secured firstly by extreme product-market fit and secondly by marketing budgets.

CEB leaderboard: US brands dominate the top

According to Blask data, the CEB ranking is captured by US-focused brands (Bovada, FanDuel, DraftKings, BetOnline) and Bet365, a global player.

Bovada commands the top spot with $8.09B in projected revenue.

FanDuel (~$7.59B) and DraftKings (~$7.05B) work in a highly regulated, high-ARPU environment, operating in just two countries each: the United States and Canada.

Expensive markets reward operators who focus on lifetime value over volume through premium UX and deep sportsbook integrations.

Why the APS ranking diverges from CEB leaders

The near-total absence of overlap between the APS and CEB leaderboards is a structural feature of the modern iGaming economy.It reflects two fundamentally different business models: volume-driven mass acquisition versus value-driven premium monetization. Two mechanics explain this gap.

The ARPU chasm

The gap comes down to market economics. US-facing brands like FanDuel, DraftKings, and Bovada operate in high-GDP jurisdictions with a mature sports betting culture. These operators generate massive CEB from a modest player base because the average stake and lifetime value are exceptionally high.

Conversely, APS leaders like betPawa, SportyBet, and Betway focus on emerging markets in Africa and Latin America. These regions offer massive population pools but lower disposable incomes. To succeed, operators must rely on micro-betting and high-frequency, low-stake play.

Marketing mechanics and traffic sources

The cost of acquiring a player dictates the marketing strategy. In the high-CEB markets, customer acquisition costs (CAC) are enormous. Operators rely on expensive television advertising, major sports league sponsorships, and high-tier affiliate deals. This strategy builds immense brand equity but yields a lower volume of signups relative to the spend.

Volume leaders in the APS top-10 utilize highly efficient, localized acquisition channels. Grassroots marketing, SMS campaigns, local agent networks, and micro-influencer partnerships drive massive signup numbers at a fraction of the cost per acquisition.

Why Bet365 and 1xBet are in two leaderboards

Only two brands, Bet365 and 1xBet, appear in both top 10 leaderboards, demonstrating true hybrid dominance across 88 and 115 countries respectively. Yet they get there in completely different ways.

Bet365 focuses on expensive and mature markets like the UK, while simultaneously deploying localized, high-volume acquisition strategies in emerging markets like Brazil.

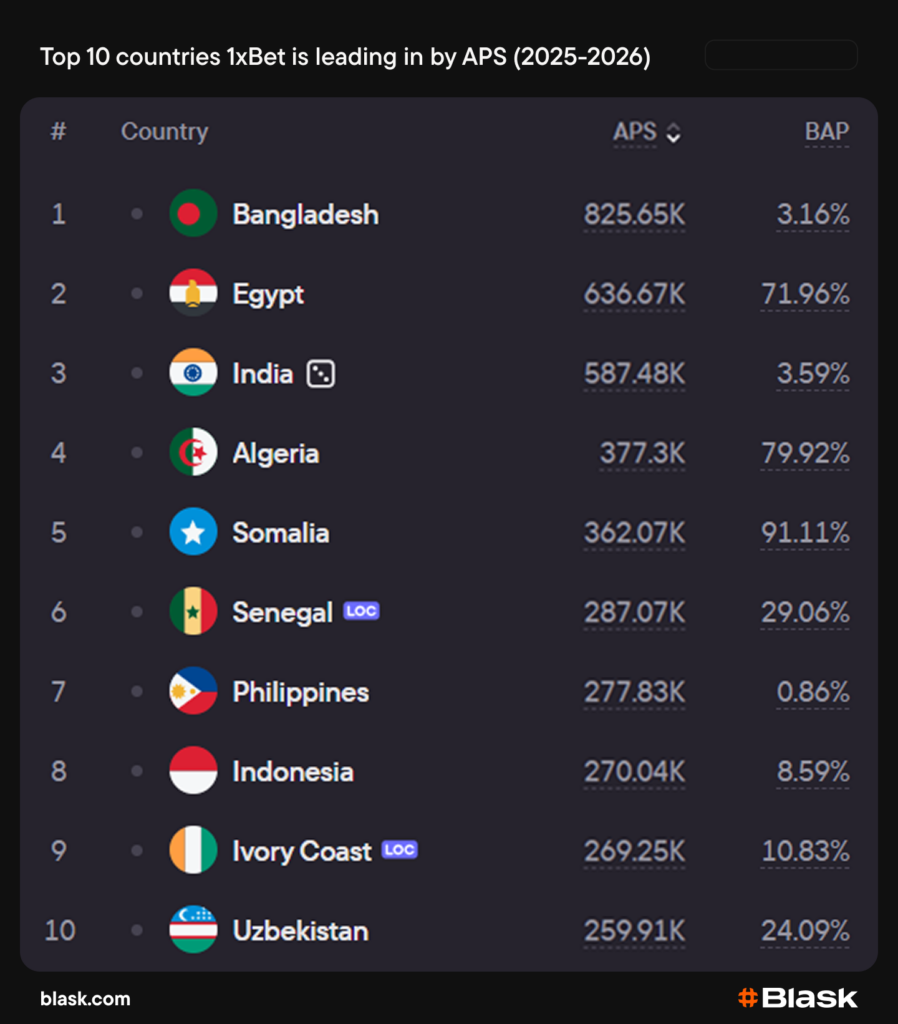

1xBet, conversely, focuses on tier-3 countries with a huge but low-income population. The brand spreads across 115 countries, capturing both volume and value through sheer geographic scale.

Bottom line

The iGaming market is split into two distinct economies: volume-driven mass acquisition in emerging markets and value-driven premium monetization in mature jurisdictions. While brands like betPawa dominate player signups through localized strategies in Africa and Latin America, US-facing giants like Bovada and FanDuel extract massive projected revenue from a smaller, high-ARPU user base.

With only Bet365 and 1xBet managing to be in both rankings, operators should choose their strategy carefully — either chasing scale in high-growth regions or maximizing lifetime value in wealthy, regulated markets.