- Updated:

- Published:

Argentina’s iGaming market: local brands lead demand, but most revenue goes offshore

Blask data shows that LatAm’s third-largest iGaming market is leaking revenue offshore despite a high channelization rate.

Argentina built one of Latin America’s fastest-growing iGaming markets without a national regulator. Each of its 24 jurisdictions issues its own licenses and sets its own rules. By 2025, the market reached $1.44B in projected revenue — and offshore operators captured over 60% of it.

The fastest-growing major market in Latin America

Argentina is the third-largest iGaming market in Latin America after Brazil and Mexico by CEB (Competitive Earning Baseline, Blask metric for projected revenue). In 2025 the country’s CEB nearly doubled compared to 2023 and reached $1.44B. That was the fastest growth for the period among Latin America’s top five markets — Chile grew 52%, Colombia 51%, Mexico 39%, Brazil 23%.

Argentina does not have a national regulatory framework for iGaming — each of the 24 jurisdictions sets its own tax rate, product rules, and licensing requirements. Operators with licenses in Buenos Aires Province and in the Autonomous City of Buenos Aires reach the largest urban concentrations in the country.

According to Blask data, the vast majority of iGaming brands in Argentina are offshore, but local operators manage to catch most of the user demand.

Licensed brands are winning demand

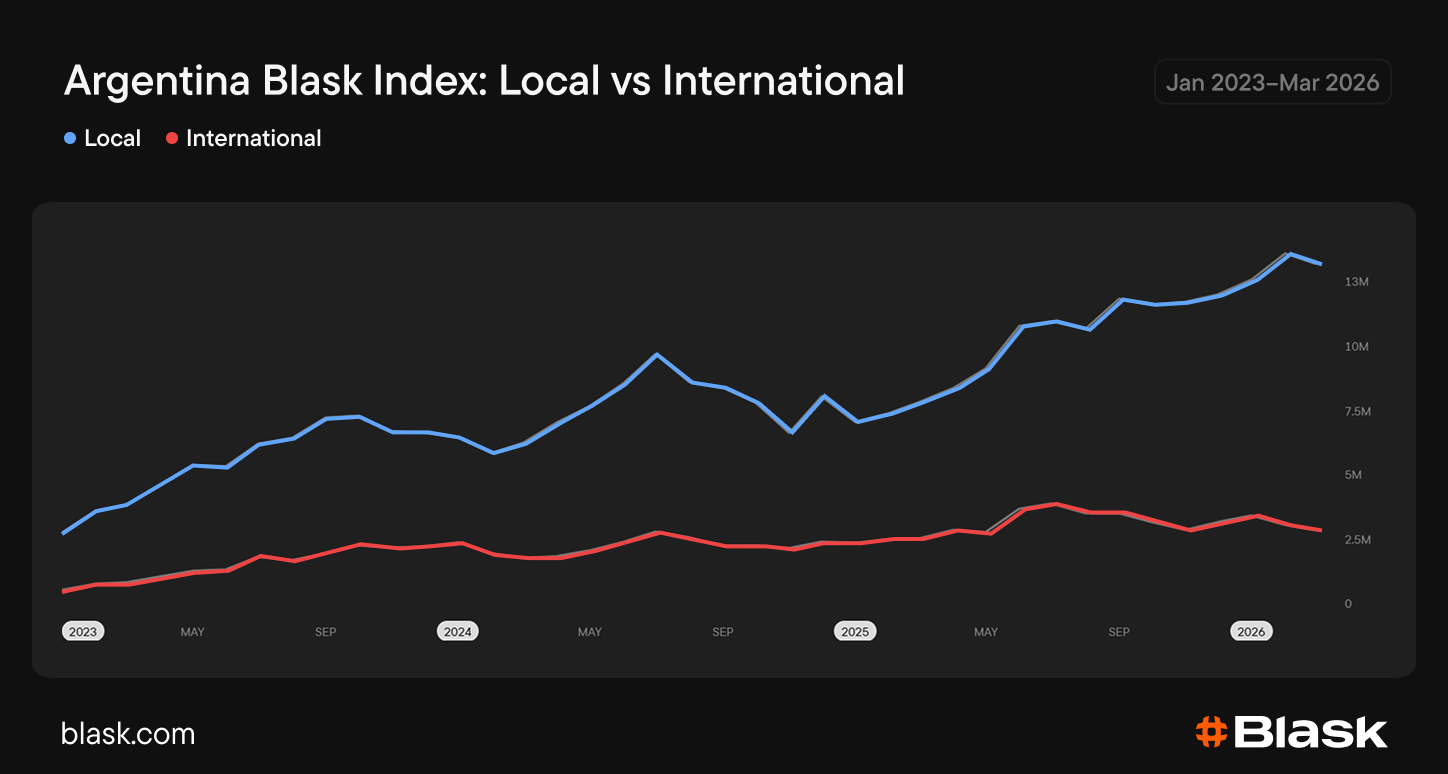

Argentina’s Blask Index rose nearly 4.5x from January 2023 to March 2026. Licensed brands captured most of that growth. Offshore brands’ share of Blask Index peaked at 27.9% in January 2024 and fell to 18.5% by March 2026.

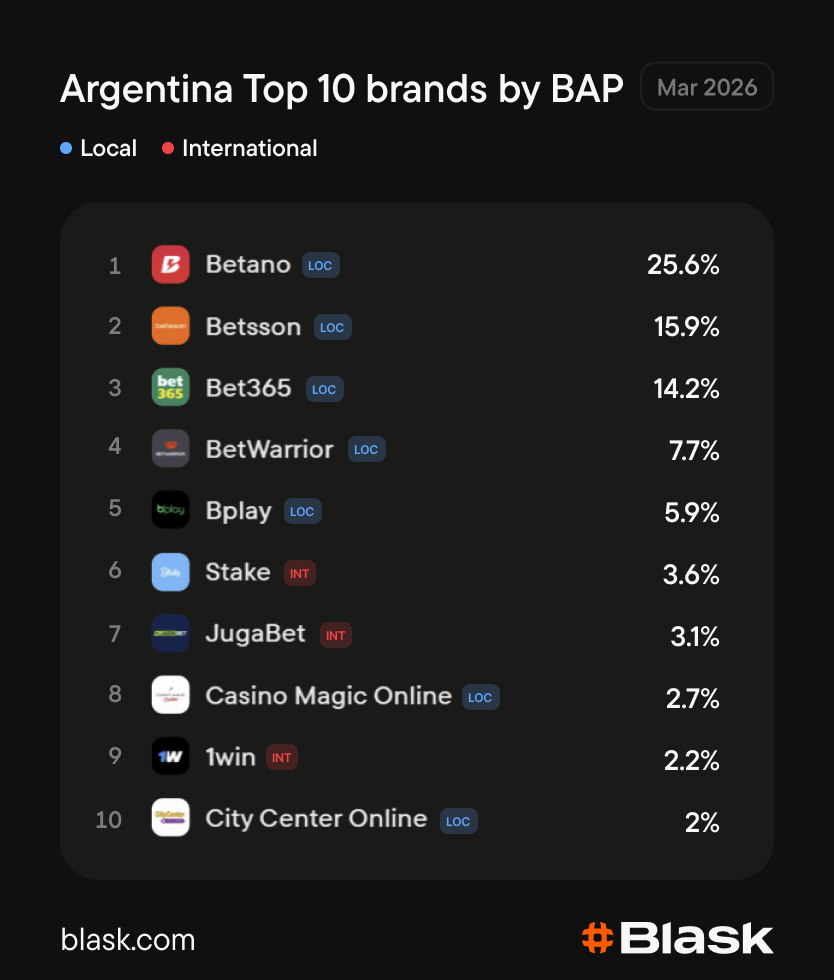

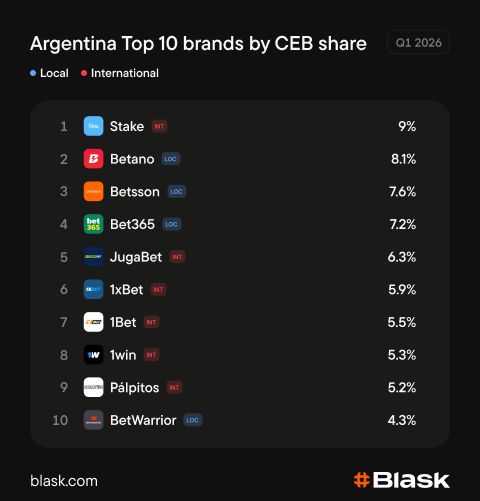

The current market leader by BAP (Brand Accumulated Power, share of country’s Blask Index) is Betano, which officially entered the Argentine market only in early 2024. By March 2026, its BAP reached 25.6%. That means Betano’s share of iGaming demand in Argentina went from zero to a quarter of market total in just 26 months.

Six of the other nine brands in the top 10 are also licensed. The seven local operators together hold almost 74% of total market demand. The three offshore brands in the top 10 hold less than 9%.

Licensed brands own the demand. But, surprisingly, international operators take the money.

Most of the revenue goes offshore

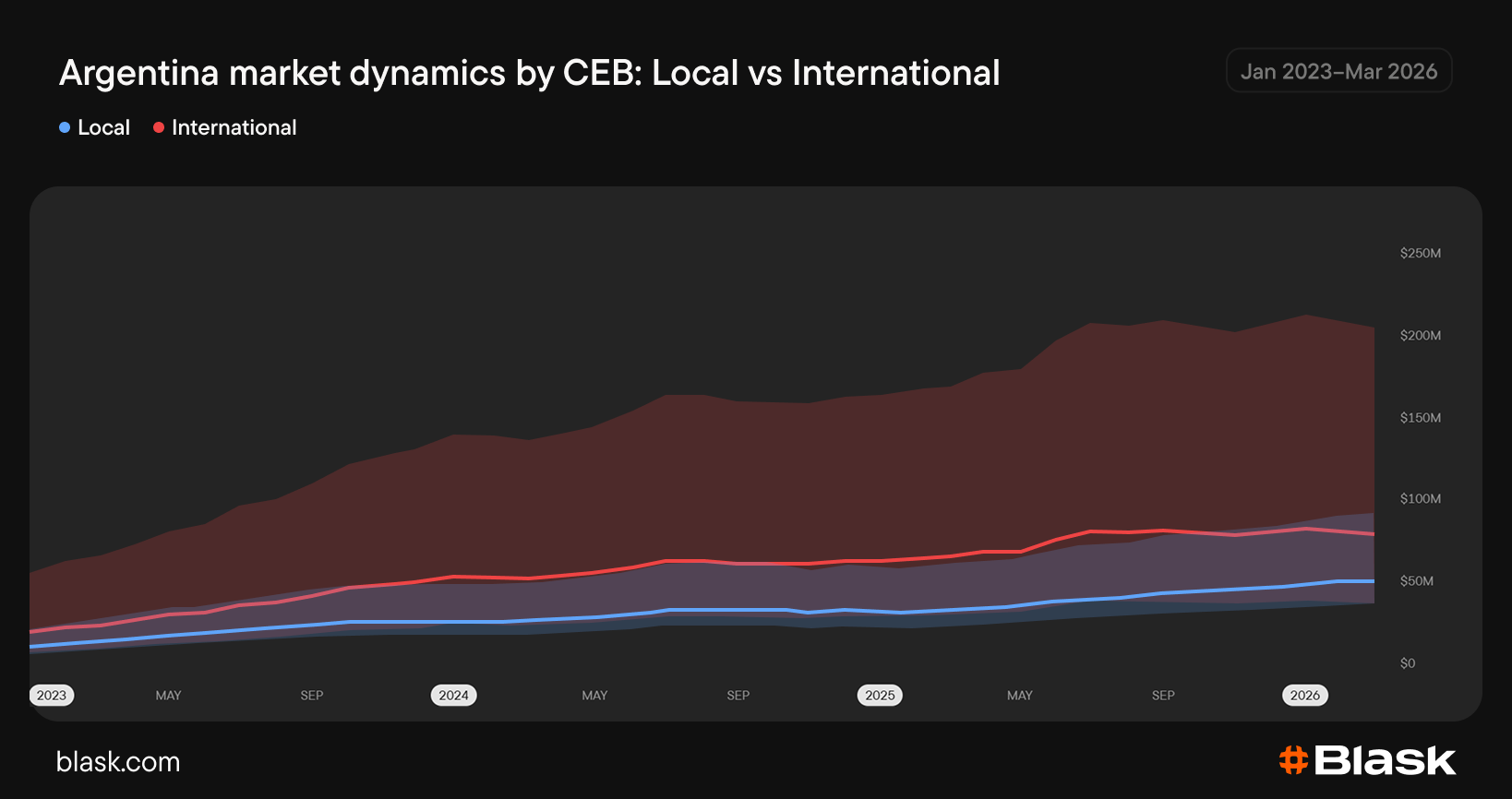

In March 2026, the offshore brands accounted for 60% of the country’s total CEB. That share was generally stable over the past three years, peaking at 66% in July 2025.

The market leader by CEB is Stake — an offshore operator. It ranked sixth by BAP in Q1 2026 and held 9% of Argentina’s total projected revenue. Betano, first by demand, held 8.1%. Only 4 brands among the top 10 by CEB in Argentina are operating with local licenses — a complete opposite picture to BAP ratings.

Licensed operators pay provincial GGR taxes and absorb licensing costs, compliance requirements, and local operational overhead. Offshore brands pay none of this. But the cost gap does not explain players’ tendency to spend more on unlicensed sites.

Conrado Caon, iGaming generalist Consultant and founder of i9MktTech, a Brazilian digital services Martech serving iGaming operators among other industries, points to friction, ignorance, and illegal advertisement.

“The type of KYC that is mandatory in a regulated market is a lot more strict, and there is a little bit of friction in the process. Due to the inefficiencies to successfully block the illegal market, betting on offshore platforms, even being illegal, still presents smaller friction. There is still lack of proper consistent education and players are still wrongly induced by illegal influencers that the payout is supposedly bigger — which is unproven but unfortunately some influencers still find a way to advertise it this way (illegally)”.

Conrado Caon Founder i9MktTech

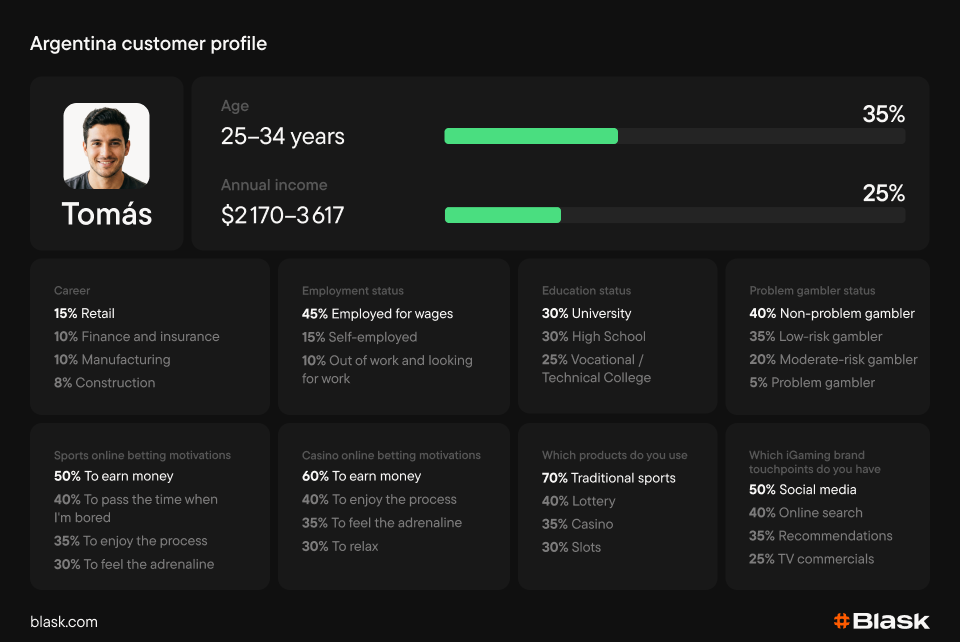

The players are young and ambitious

Blask’s customer profile reveals a rather young user base – 65% of iGaming players are under 35. And their primary motivation is earning money: 50% of sports bettors and 60% of casino players cite it first.

The most popular iGaming products are traditional sports betting, lottery and live casino. The main channels for iGaming brand touchpoints are social media and online search.

Bottom line

Argentina’s licensed iGaming segment won the search competition. Offshore brands kept most of the revenue. Betano’s fast rise from zero to over 25% demand share shows that brand investment works, but the brand still generates less CEB than Stake.

The BAP and the CEB leaderboards decoupling is structural: KYC friction, anonymity, and payout perception send money offshore even when players search more for licensed brands.