- Updated:

- Published:

Peru’s iGaming Market: at risk of duopoly

One brand holds half of the demand, and another is catching up.

Peru’s iGaming regulation framework came into force in early 2024. The licensed market it produced is now the most onshore-dominated of any major iGaming country in Latin America — but it didn’t grow evenly. Demand more than doubled, and most of the gain went to two brands.

The regulation brought activity onshore

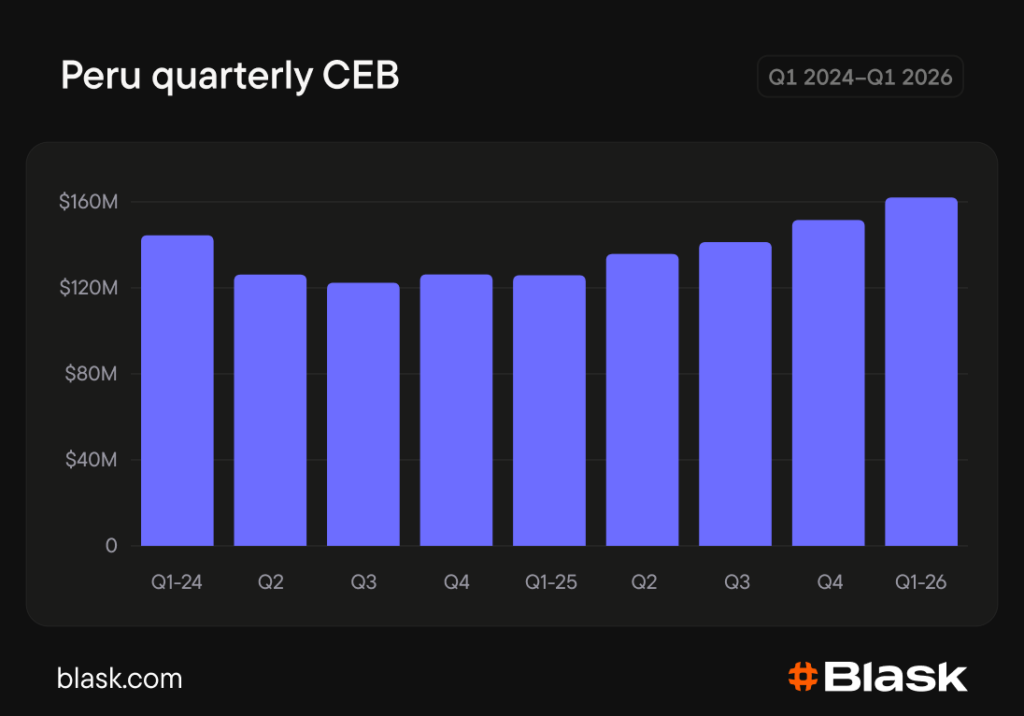

Peru is the fifth-largest iGaming market in Latin America by CEB (Competitive Earning Baseline, Blask metric for projected revenue). According to Blask data, the country’s Q1 2026 CEB exceeded $162M, up 6.9% from Q4 2025. The last two quarters are the two strongest by CEB since regulation in Peru came into force in February 2024.

Locally licensed brands accounted for 99.8% of Peru’s Blask Index (a metric used to measure iGaming demand in a given market) and 98% of CEB in March 2026. Onshore share has held above 95% across both Blask Index and CEB throughout 2025 and into 2026. Among Latin America’s other major iGaming markets, the closest onshore shares are Brazil at 95.7% of Blask Index and Mexico at 92% of CEB.

But the licensed market did not grow evenly across operators or across metrics.

Demand outran revenue

The activity the regulation framework brought onshore raced ahead of operators’ ability to monetize it. Quarterly Blask Index was 123.9% higher in Q1 2026 than in Q1 2024. CEB rose 12.2% over the same period.

The main demand driver in Peru is football. The all-time high for Peru’s Blask Index came in February 2026, the opening month of the domestic Liga 1 season. The previous high was registered in September 2025, when the country’s CONMEBOL World Cup qualifier campaign ended and Liga 1 was in full swing.

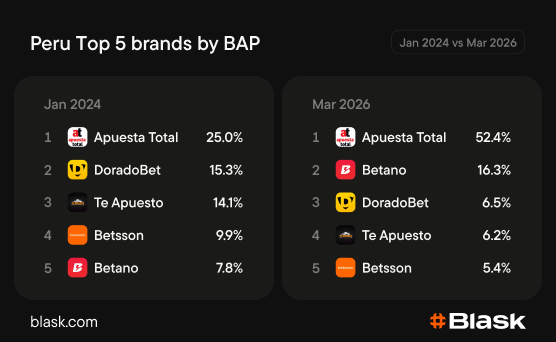

The number of active brands tracked by Blask in Peru was stable across the years — 171 brands in January 2024 and 165 in March 2026. The top 5 of them by BAP (Brand Accumulated Power, share of country’s Blask Index) changed only by order. But the concentration of demand rose significantly — from 72.1% to 86.8% for top 5 brands.

Three of the brands, DoradoBet, Te Apuesto and Betsson lost their BAP share. Their Blask Index also fell in absolute values while the country’s demand more than doubled.

Users’ attention went to the competitors — Apuesta Total and Betano. Both rose more than 4x in absolute Blask Index over the period.

Apuesta Total has dominated the market since December 2024. Together with Betano they were responsible for 68.7% of the country’s Blask Index in March 2026.

Regulation arrived at an already concentrated market and tightened it further, leaving less room for smaller brands.

A young, sports-first user base

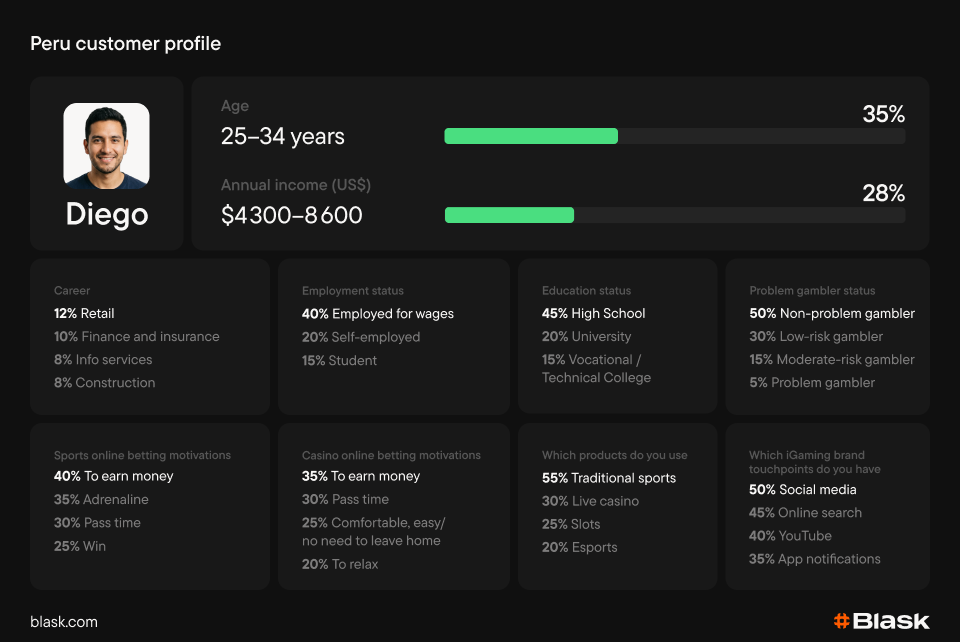

Blask’s customer profile data shows who the consolidated market is built around. 57% of Peru’s iGaming users are under 35. 60% are employed. The largest education group is high school, at 45%. Income is concentrated in the lower-to-middle bands.

The top motivation across both sports and casino betting is earning money. Traditional sports lead product use at 55%, with live casino at 30% and slots at 25%. The sports lead is wider than in Chile, and narrower than in Argentina.

The main touchpoints are social media, online search, YouTube and mobile app notifications. Peru’s iGaming users are reached primarily through high-frequency mobile channels.

Bottom line

Peru is the most onshore-dominated iGaming market among major Latin America countries, and one of the most concentrated. Demand is growing fast, and most of it sits with two operators. Betano’s share of Blask Index has more than doubled in the past year, while Apuesta Total continued to dominate — a trajectory that could turn the market into a duopoly.