- Updated:

- Published:

India’s iGaming ban: what changed and what didn’t

Blask data show that despite increased pressure from Indian authorities, iGaming demand in 2025 followed 2024’s pattern, with operators adapting rather than the market breaking.

India started 2025 without a nationwide licensing framework for iGaming, so the policy shift was never a clean “licensed market closes” moment. Parliament passed a ban on online money games in August, and it took effect on 1 October. The story, however, is not an October cliff. The turning point in Blask Index comes earlier, and the clear signal of tightening is how attention redistributed among operators.

A year of tightening

The ban formalized a tougher stance on real-money play, and it arrived after months of pressure. By March, authorities had already blocked hundreds of offshore URLs and frozen dozens of bank accounts linked to illegal online gaming.

That sequence matters because it spreads the impact across the year. Operators and users adjusted before the law was introduced, then tested the new rules once they took effect.

Demand moved forward in 2025

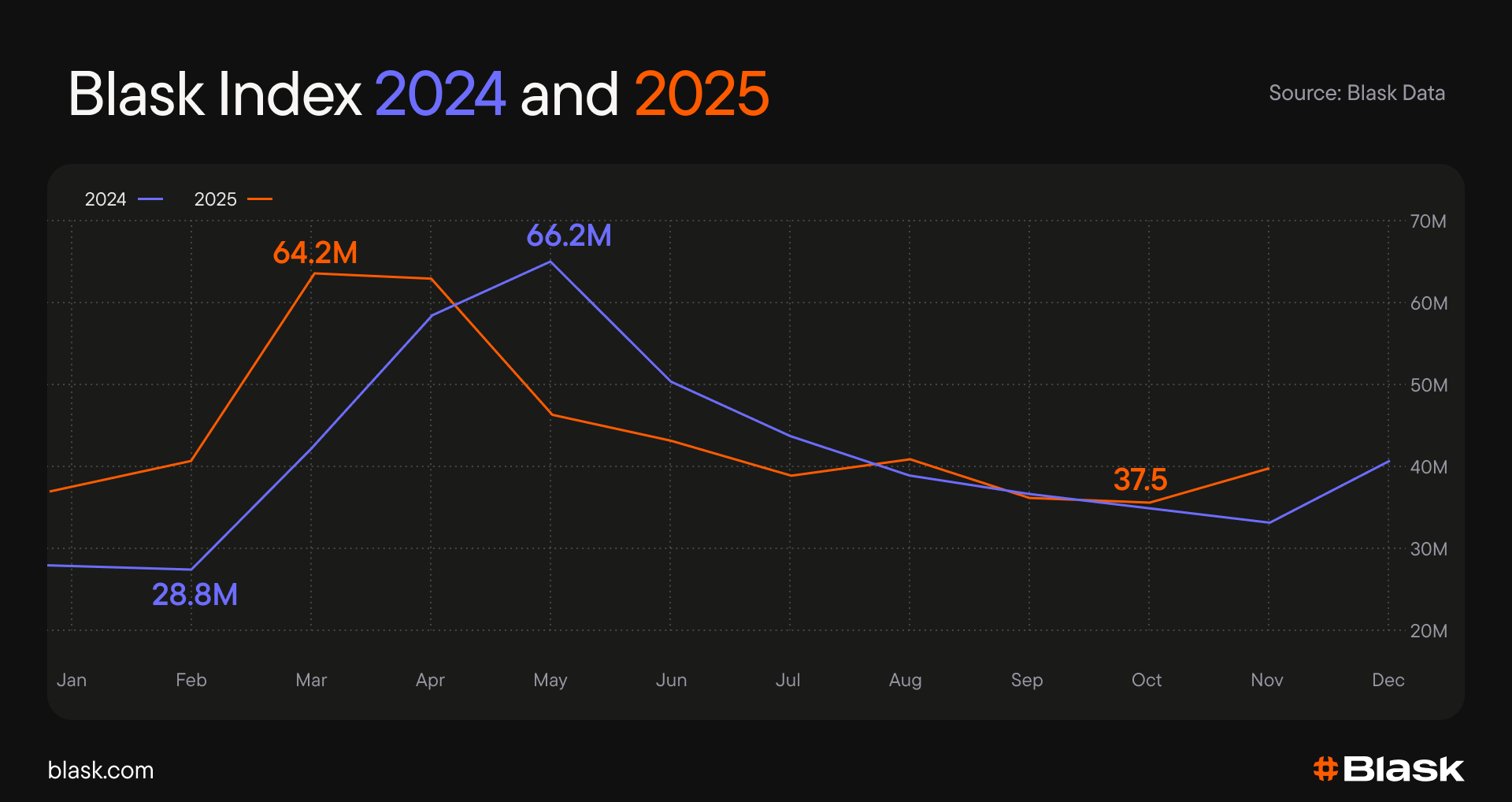

Blask Index shows 2025 running far above 2024 in the first quarter. March 2025 reached 64.19m, versus 42.92m a year earlier.

The calendar offers a simple explanation for part of that shift. The ICC Champions Trophy, an international cricket tournament, ran from 19 February to 9 March 2025, adding a major betting window before the Indian Premier League (IPL), India’s flagship Twenty20 cricket league.

The more telling move is what happens next. After the early peak, Blask Index steps down sharply in May and stays softer than 2024 through October, before picking up again in November.

Two things line up with that break. The IPL was paused in early May during an India–Pakistan flare-up, then resumed later in the month. Late April also brought a burst of enforcement, including arrests of social-media promoters of gambling and wider scrutiny of offshore betting networks and payment routes.

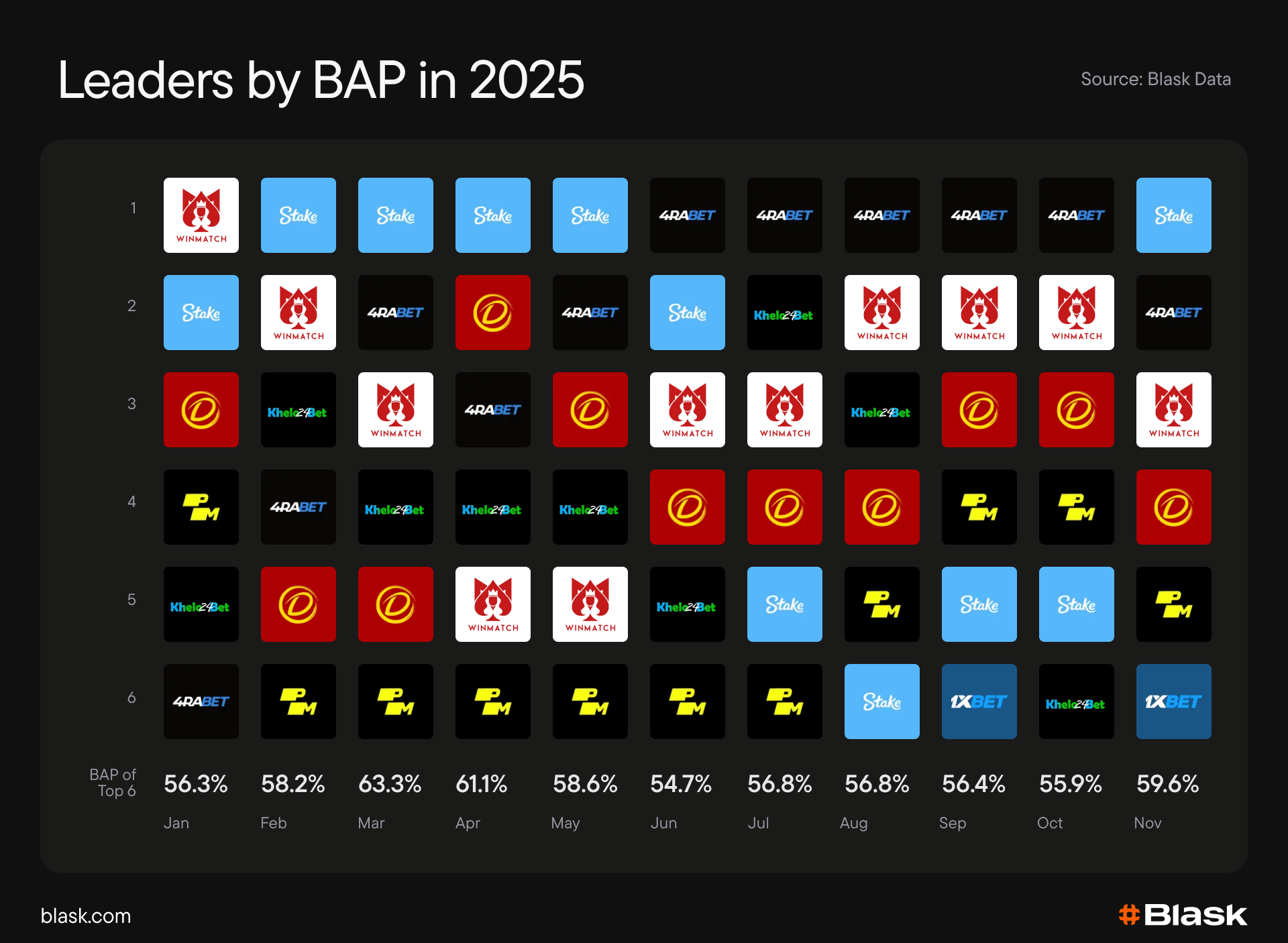

The same leaders, different order

Blask BAP data show rotation inside a stable top tier rather than a changing cast. Leadership shifts between the same heavyweight brands over the year, with 4RABET taking the lead through the summer and Stake reclaiming it late in the year.

Brand power shifted among the top operators. The market became more concentrated late in the year, as the leading brands lost some share mid-year but regained it by November.

Those shifts are difficult to match one-to-one with public enforcement headlines. Actions in India often target access routes and payment channels rather than a single brand name, and operators can reappear via mirrors and new domains.

What changed, and what didn’t

Blask Index does not show a single demand shock at the policy milestones. The decisive cooling arrives in May, and the market looks steadier by November than the early autumn low.

What tightening seems to have changed is allocation. The leader changes, the same names remain dominant, and the top tier ends the year taking a slightly larger share again.