- Updated:

- Published:

Online gambling market forecast 2026: what the numbers actually say

In the span of a single decade, online gambling transformed from a regulatory afterthought into one of the fastest-growing industries on earth. And if iGaming industry trends 2026 show anything clearly, it is that growth is no longer the story on its own. By the end of 2026, the global market is expected to surpass $143 billion in revenue — nearly double what it was five years ago. Governments that once banned the practice are now writing licensing frameworks. Brands that did not exist in 2022 are already ranked among the top five in markets the size of Germany.

The growth is real. But where it is happening, and which operators are actually capturing it, is a more complicated story.

The baseline: $143 billion in 2026, $212 billion by 2030

The global online gambling market is projected to reach $143.17 billion in 2026, up from $130.2 billion in 2025. The CAGR consensus lands around 10–12% through the decade, with most estimates placing the market between $153B and $212B by 2030 depending on regulatory pace.

Eastern Europe is flagged as the fastest-growing region. Asia-Pacific remains the largest. Latin America is the story everyone keeps calling “emerging” even though Brazil alone moved 79 million new customers through online gambling platforms in 2025.

Let’s look at what’s actually happening, market by market.

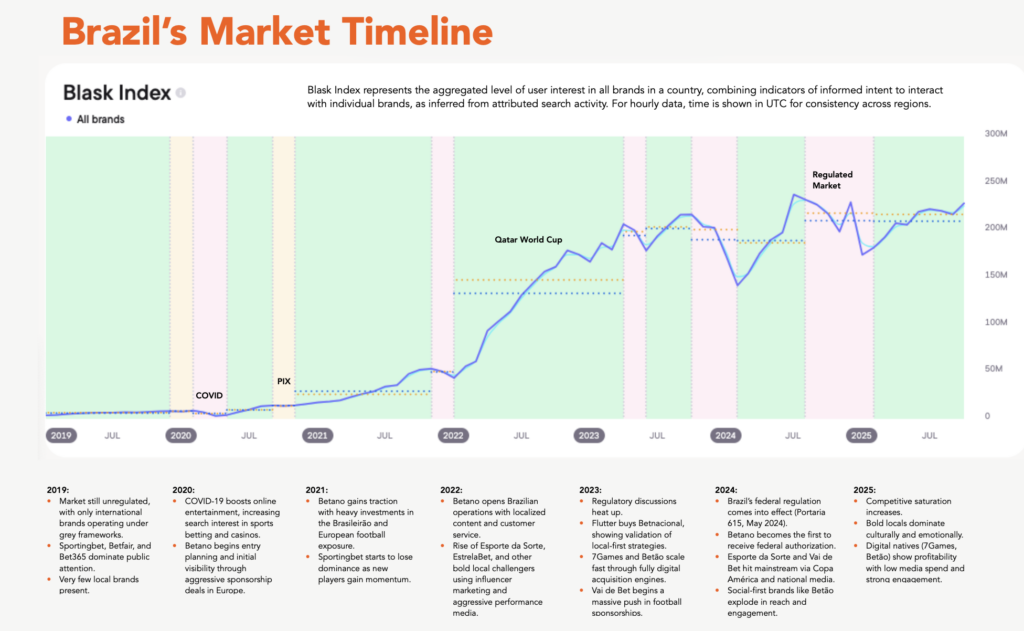

Brazil: 542 brands, 79 million new customers

Brazil is one of the fastest growing online casino markets regulated and from 2025 regulated. Then it exploded.

According to Blask data for 2025, the Brazilian market now has 542 active brands competing for consumer demand — more than any other single regulated market tracked. Full-year APS (Acquisition Power Score): 79.2 million new customers. CEB (Competitive Earning Baseline): $6.3 billion.

Betano is #1 — 16.3 million new customers, +21% YoY. Bet365 is #2.

What’s interesting isn’t just the scale. It’s the pace. Brazil went from unregulated to one of the highest-demand markets on earth in under two years, and the brands that moved early are already building structural moats. The window to establish meaningful brand equity in Brazil exists right now. Whether it stays open through 2027 is a different question.

Download the free report: Brazil’s top 20 operators in 2025

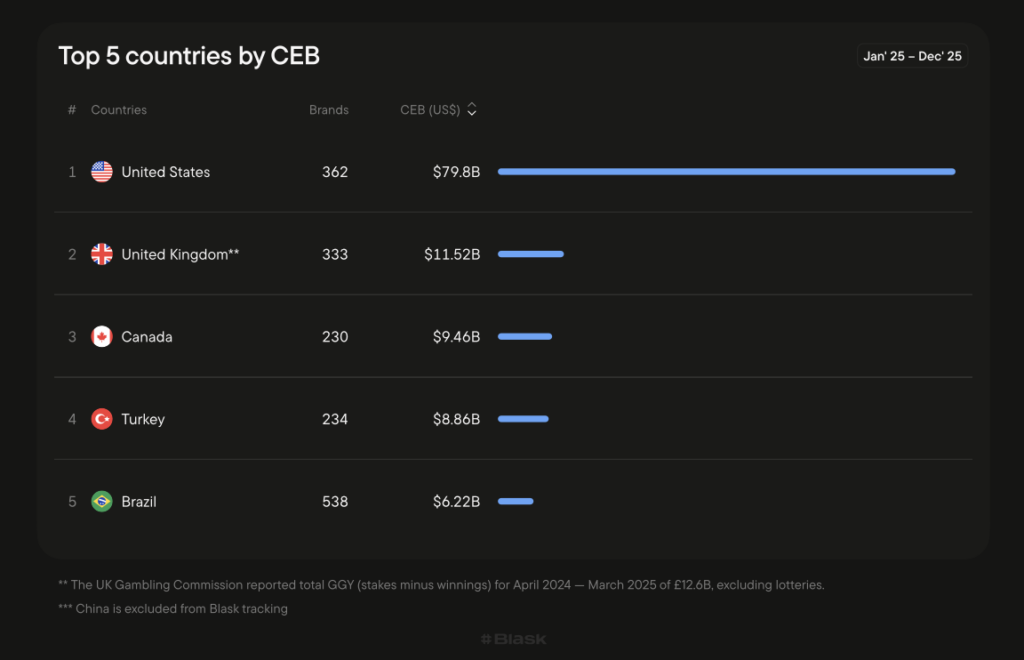

United States: the revenue outlier

The US is its own category, and the numbers are genuinely wild.

Total CEB across all US-tracked brands in 2025: $81 billion. The US market — a mix of state-licensed operators and offshore books — generates more nominal revenue than any other single-country market Blask tracks. By a large margin.

Bovada leads on demand: $9.2B CEB, 1.4M APS, +10.78% YoY. BetOnline sits at #2 (+28.88% YoY). DraftKings is #3.

The offshore/onshore split is complicated. Regulated brands (DraftKings, FanDuel, BetMGM) dominate licensed states. Offshore books quietly maintain their position everywhere else. State-by-state expansion continues — each new licensed jurisdiction adds demand signal and shifts BAP distribution. The affiliates who built organic presence in tier-2 states ahead of regulation are in a structurally strong position right now.

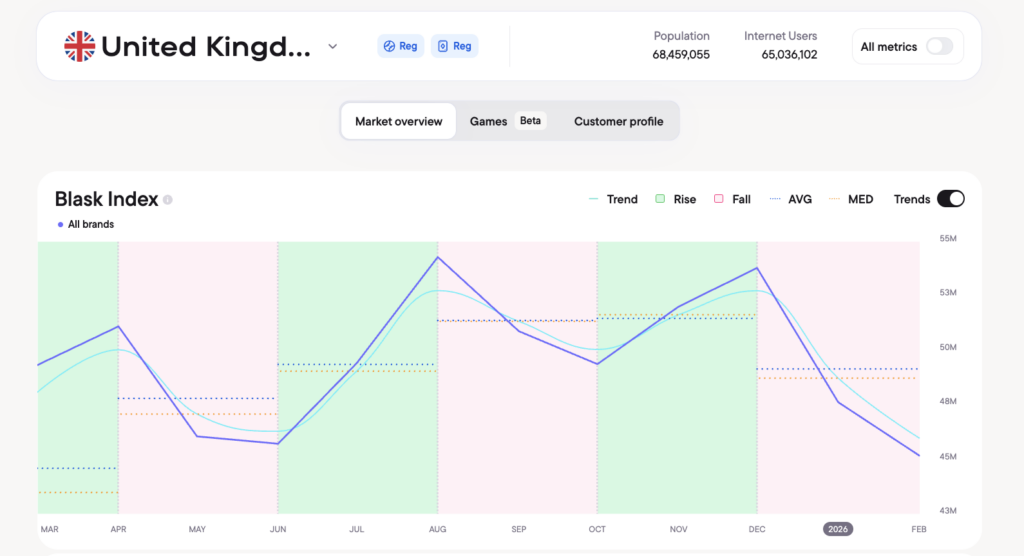

United Kingdom: mature, not done

The UK had 347 active brands generating $11.5B CEB and 19.8M APS in 2025 — the highest per-capita acquisition volume of any major regulated market tracked.

Bet365 leads. The interesting movement is mid-table: Betway +33% YoY, BoyleSports +36%, Grosvenor +50%. The top stays stable; the second tier is fighting hard and winning market share.

UKGC affordability checks and stake restrictions continue to pressure unit economics. Operators built on high-value player segments are recalibrating. The market isn’t shrinking — but how you extract value from it is changing. Anyone still running a UK affiliate strategy from 2022 is doing it wrong.

Read also: European iGaming market outlook 2026: where demand is growing

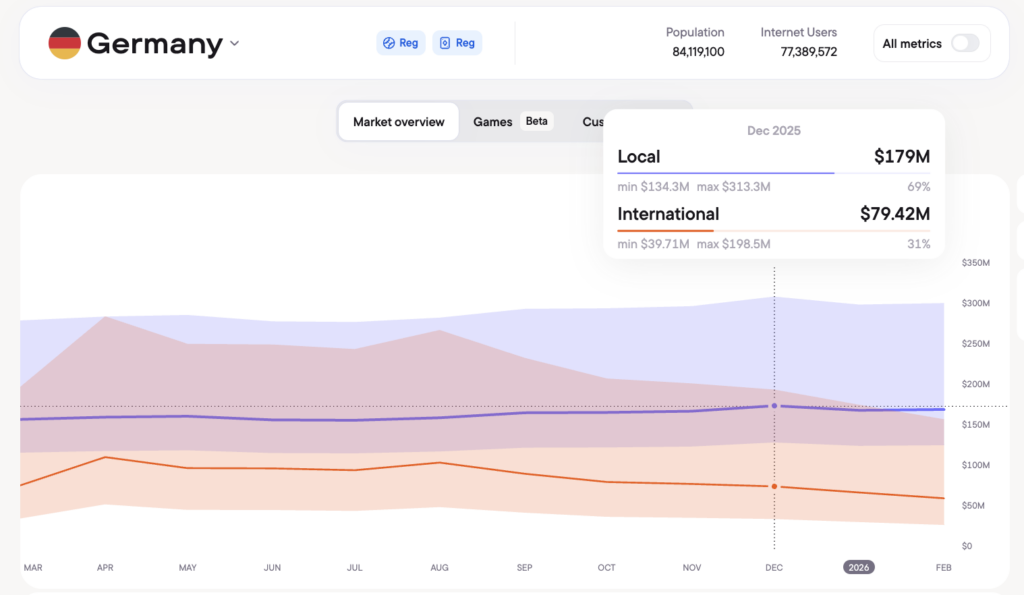

Germany: offshore disruption in real time

This is the one worth watching.

Vulkan Vegas grew +719% YoY in Germany in 2025. NV Casino launched in November 2024 and is already ranked #2 in the German market by BAP — $347M CEB in its first year of operation. Verde Casino launched in February 2025 and is already at #5.

Tipico is still #1. Dominant, stable, +2.6% YoY. But the challengers are not operating by legacy rules. They’re offshore, moving fast, and capturing demand that compliant operators are leaving on the table due to licensing constraints.

Germany’s regulated framework (GlüNeuRStV) was designed to channel consumer demand into licensed operators. The data suggests a meaningful share of that demand is going elsewhere. That’s the regulatory paradox German operators are living with in 2026 — and it’s getting louder, not quieter.

What to do with this in 2026

If you’re an operator:

- Brazil and LatAm are the highest-ROI acquisition markets right now. The window is real, not analyst-speak.

- US state expansion is a compounding asset. Every new licensed state becomes a structural advantage for brands already present in neighboring ones.

- Germany is a consolidation market — fight hard for shelf position or accept being slowly squeezed by offshore challengers who don’t have your compliance overhead.

If you’re an affiliate:

- Markets with high total APS and moderate brand concentration (Germany, Brazil) offer the clearest opportunity. You don’t need to beat Bet365 — you need to capture the demand they’re not converting.

- UK is crowded but deep. The mid-tier growth stories signal where operator budgets are actually moving. Follow the money.

Tracking this in real time

Market forecasts are useful for context. What actually drives decisions is live brand-level demand data — who is growing, where, and why. That is especially true when evaluating the top iGaming markets in 2026, where momentum can shift faster than most static reports can capture.

Blask’s Market pages show current rankings, APS, and CEB for every major market. Market Explanation tells you why a market moved — not just that it did. The Blask Index tracks consumer demand signals derived directly from search behavior and updates continuously.

If the numbers in this post were useful, the live version is even more so.