- Updated:

- Published:

Peru iGaming market Q1 2026: brands, demand, and what changed

Peru’s iGaming demand grew 36% year-over-year in Q1 2026, Betano doubled its market share at the expense of legacy local operators, and offshore revenue share collapsed from 3.85% to 1.62% as formalisation under Law No. 31557 accelerated.

Peru entered 2026 with momentum already built.

Blask Index — a demand signal derived from search activity across all iGaming brands — reached 93.3M for Q1 2026, up from 68.4M in the same period a year earlier. That 36% jump is not a base effect. It reflects genuine market expansion: more licensed platforms, growing player acquisition, and a regulatory framework that has steadily pulled activity out of the grey zone since Mincetur began enforcing its online gambling rules in 2024.

Track Peru in real time at blask.com/market/peru

Three stories define Q1 2026. Apuesta Total extended its dominance with high-profile sponsorship and payment infrastructure moves, holding more than half of all market demand. Betano, the Kaizen Gaming platform that launched locally in 2022, nearly doubled its BAP position — the biggest share gain in the top 10. And the offshore compression story accelerated: unlicensed international operators, who held 3.85% of estimated market revenue in Q1 2025, are down to 1.62%.

About the data: The Blask Index measures consumer search demand for iGaming brands, derived from Google Keyword Planner and Google Trends. BAP (Brand Accumulated Power) shows each brand’s share of total market demand. CEB (Competitive Earning Baseline) and APS (Acquisition Power Score) are revenue and acquisition benchmarks based on brand strength and competitive positioning, not operator-reported figures. All data for Peru, Q1 2026 (January–March).

Market demand in Q1 2026

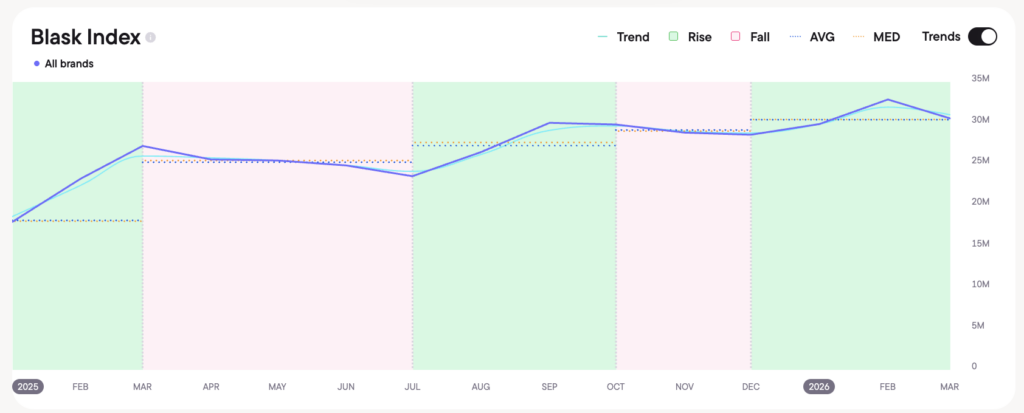

Peru’s Blask Index reached 93.3M in Q1 2026. A year earlier it stood at 68.4M. The 36% year-over-year gain is the strongest Q1 growth the market has posted. Quarter-on-quarter the increase was more modest — up 7% from 87.3M in Q4 2025 — but meaningful given that Q1 is typically a softer period following the football season peaks of October–November.

Competitive Earning Baseline (CEB) — Blask’s market-based revenue benchmark built from brand strength and competitive dynamics — averaged $54.0M per month in Q1 2026 ($40.3M–$95.2M range), up from $42.0M a month in Q1 2025 ($31.1M–$74.6M). That 29% increase in estimated monthly revenue potential tracks closely with the demand growth.

Acquisition Power Score (APS) — Blask’s estimate of how many new customers a market’s competitive position should deliver — reached 993K new sign-ups per month on average in Q1 2026 (743K–1.74M), up 32% from 752K a year earlier (562K–1.32M). Peru added roughly 241K monthly APS points year-over-year, almost entirely absorbed by licensed operators.

One number to carry from this section: 93.3M in Blask Index terms, up 36%, driven by 163 active brands competing for a growing and increasingly formalised player base.

Local vs international: how the market splits

Peru’s licensing framework is producing one of the fastest offshore compression trends in Latin America.

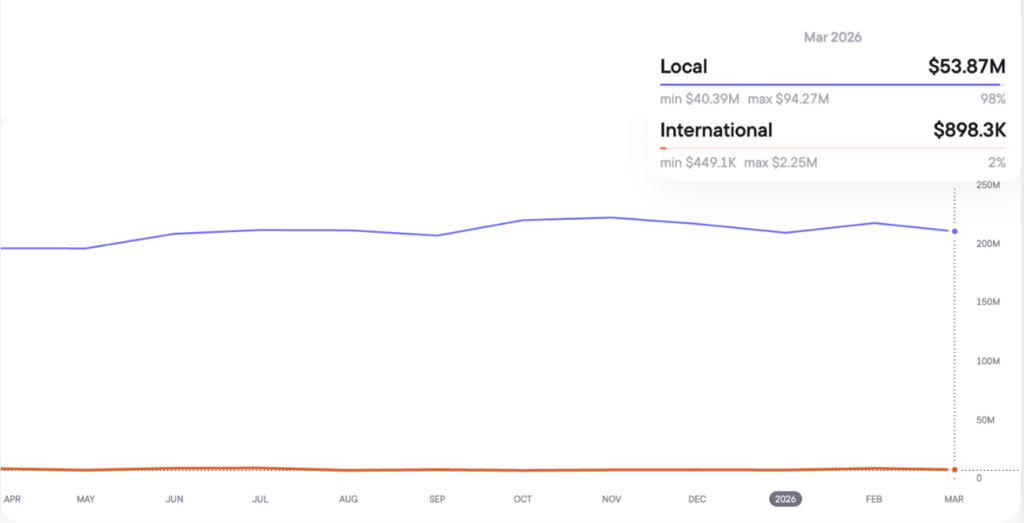

In Q1 2025, offshore operators — international platforms operating without a Mincetur licence — held 0.52% of Blask Index demand but 3.85% of estimated CEB revenue.

That gap (roughly 7x efficiency premium) reflects higher per-player revenue from less-regulated environments. By Q1 2026, offshore demand dropped to 0.23% and revenue share to 1.62%.

| Q1 2025 | Q1 2026 | Change | |

|---|---|---|---|

| Blask Index — local (licensed) | 99.48% | 99.77% | +0.29pp |

| Blask Index — international | 0.52% | 0.23% | –0.29pp |

| CEB — local avg/month | $40.3M (96.1%) | $53.2M (98.4%) | +32% |

| CEB — international avg/month | $1.6M (3.9%) | $0.87M (1.6%) | –46% |

In absolute terms, offshore monthly estimated revenue halved from $1.6M to $0.87M. Licensed operators grew from $40.3M to $53.2M per month. The 7x offshore efficiency premium is holding, but the base is shrinking fast. Formalisation isn’t just redirecting demand, it is reducing the economic case for offshore operation.

Top brands in Q1 2026

| Brand | BAP % | Change vs Q1 2025 |

|---|---|---|

| Apuesta Total | 51.1% | ↑ +3.4pp |

| Betano | 14.2% | ↑ +7.0pp |

| DoradoBet | 6.9% | ↓ –3.6pp |

| Te Apuesto | 6.0% | ↓ –2.6pp |

| Betsson | 5.4% | ↓ –0.6pp |

| Inkabet | 3.2% | ↓ –0.8pp |

| Bet365 | 2.2% | –0.1pp |

| Olimpo.bet | 2.1% | –0.1pp |

| Betsafe | 2.1% | ↓ –0.5pp |

| Stake | 0.5% | – (↑ +135% YoY) |

The ranking is defined by two moves at the top.

- Apuesta Total, the dominant local operator since 2017, gained another 3.4 percentage points to reach 51.1% BAP. Half the market’s player attention flows to a single brand. That is an unusual concentration even by LATAM standards.

- Betano’s jump from 7.2% to 14.2% is the quarter’s headline at the brand level. The platform doubled its demand share in twelve months, pulling directly from DoradoBet (–3.6pp) and Te Apuesto (–2.6pp). Both legacy players are web-heavy and app-light, a structural disadvantage as Peru’s mobile penetration deepens.

- Stake’s YoY growth of 135% is a signal worth watching, even though the brand’s absolute BAP remains small at 0.5%. Crypto-native platforms that sat outside the grey zone are beginning to test licensed pathways.

What drove the quarter

New AML requirements raised the compliance cost for offshore platforms. SBS Resolution No. 03622-2025, published in October 2025, introduced a sector-specific anti-money laundering framework. Operators are now required to report any transaction exceeding $2,500 to Peru’s Financial Intelligence Unit (UIF) within 24 hours, with direct sanctioning power granted to Mincetur for violations. For unlicensed offshore operators, the cost and risk calculus shifted materially. The Q1 2026 offshore CEB data reflects the result.

Apuesta Total invested aggressively in brand equity. In February 2026, the operator became the regional sponsor of Argentina’s national football team for Peruvian coverage, a high-visibility play ahead of the World Cup cycle. In March, it expanded payment access through a partnership with ProntoPaga. Both moves deepened the brand’s structural advantage with Peruvian players.

Market formalisation continued to expand the addressable base. By end-2025, Mincetur had authorized 54 online platforms, registered 320 suppliers, and licensed 4,583 physical betting venues nationwide. Tax receipts from remote sports betting and online gaming reached S/208.8M (~$56M) through November 2025, redirecting funds to sports development, health, and tourism infrastructure. The expanding formal ecosystem brought more players into trackable, licensed channels, which shows up directly in Q1’s Blask Index growth.

Q1 2026 vs Q1 2025: year-over-year shift

| Metric | Q1 2025 | Q1 2026 | Change |

|---|---|---|---|

| Total Blask Index | 68.4M | 93.3M | +36.4% |

| Blask Index — local share | 99.48% | 99.77% | +0.29pp |

| Blask Index — international share | 0.52% | 0.23% | –0.29pp |

| Market leader | Apuesta Total (47.7%) | Apuesta Total (51.1%) | +3.4pp |

| APS avg/month | 752K (562K–1.32M) | 993K (743K–1.74M) | +32.1% |

| CEB avg/month | $42.0M ($31.1M–$74.6M) | $54.0M ($40.3M–$95.2M) | +28.8% |

| CEB — local share | 96.1% | 98.4% | +2.3pp |

| CEB — international share | 3.9% | 1.6% | –2.3pp |

| Active brands | 161 | 163 | +2 |

Growth was universal in Q1 2026 versus Q1 2025, but the distribution was not. Apuesta Total and Betano captured the gains. DoradoBet and Te Apuesto gave up a combined 6.2 percentage points. Offshore operators shed nearly half their revenue position. The market grew 36%; within that growth, a consolidation was happening.

What this means for operators

Peru is not a market to test with minimal commitment. Apuesta Total controls more than half the demand and is growing its position through active brand and infrastructure investment. Betano has proved that an international operator with mobile-first execution can double its share in a single year, even against entrenched local competition.

The brands losing ground — DoradoBet, Te Apuesto — built their positions in an era when web presence and local trust were enough. That era is over. Mobile app coverage, payment breadth, and promotional depth now define acquisition competitiveness.

For operators considering entry: licensing is no longer a differentiator, it is the floor. The offshore revenue premium is eroding systematically. Q2 2026 will bring elevated sports betting activity around the FIFA World Cup, and surveys suggest 85% of Peruvian fans plan to bet online during the tournament. That spike will reward brands that built retention infrastructure, not just acquisition reach.

Conclusion

Peru’s Q1 2026 is a market growing on its own structural merits. Regulation is working. Demand grew 36%. Licensed operators are capturing the vast majority of both attention and estimated revenue. The competitive picture is narrowing around two dominant players, with everyone else competing for single-digit shares.

The next test comes in Q2–Q3 2026. The World Cup cycle will drive a traffic surge that every major operator in Peru is preparing for. The brands that added app coverage, payment integrations, and brand partnerships in Q1 are better positioned to convert that attention into long-term players. Those that didn’t will find the gap harder to close once the tournament ends.