- Updated:

- Published:

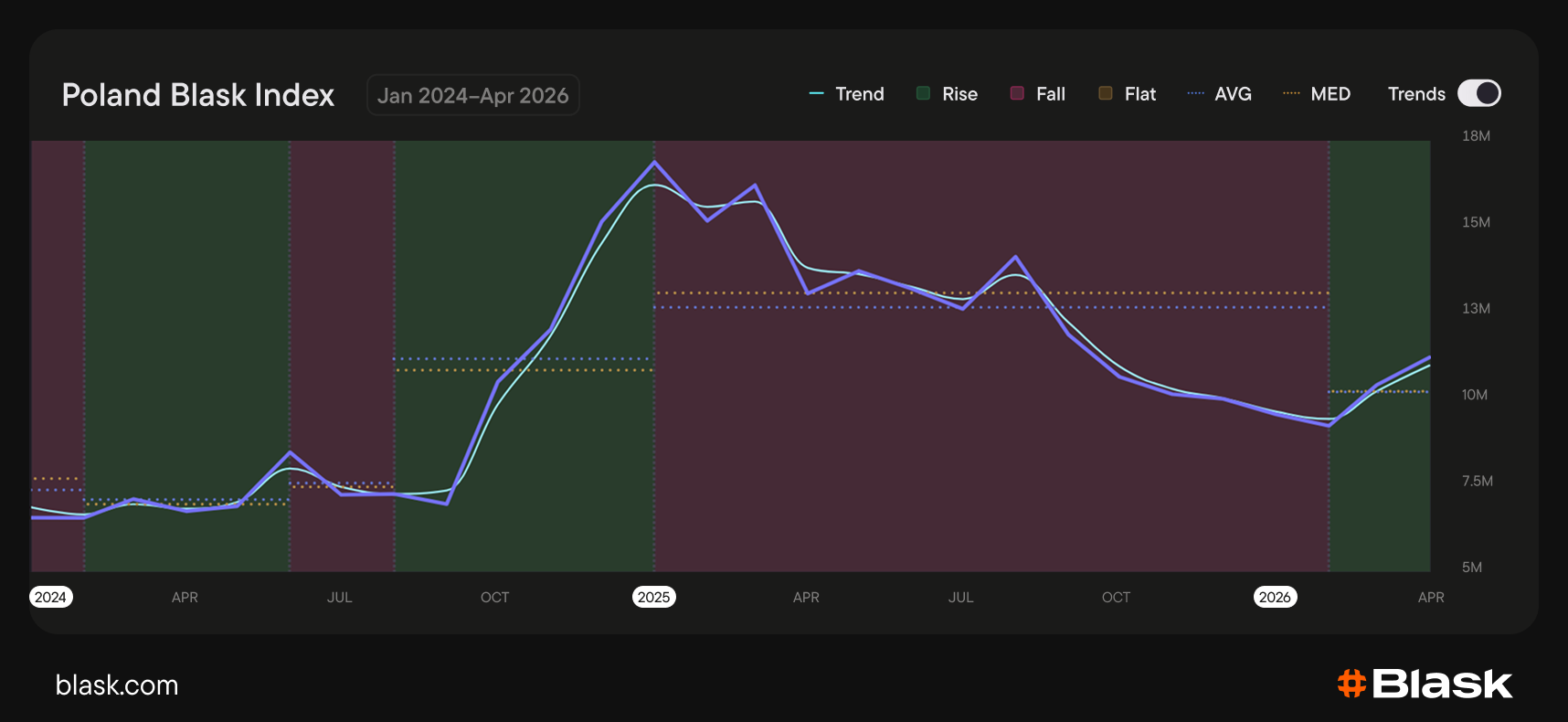

Poland’s iGaming market reversed a thirteen-month downtrend

The growth is driven by offshore brands that adapted to tightening regulatory pressure.

The demand for iGmaing in Poland fell for over a year. Offshore brands led the decline, losing ground to a regulatory campaign built to protect the country’s state-run online casino monopoly. April Blask data shows the downtrend has stopped — and offshore brands are the ones leading the market back up.

The market bottomed in February 2026

According to Blask data, Poland is one of the top 10 European iGaming markets by projected revenue, measured by CEB (Competitive Earning Baseline). Over the last 12 months, Poland’s CEB was $1.9B, level with Spain, so the two countries share 9th–10th place in Europe.

Demand for iGaming brands in Poland, measured by Blask Index, grew steadily from autumn 2024 and reached its peak in January 2025. From there it entered a thirteen-month downtrend, bottoming in February 2026. March and April reversed the direction.

Poland’s Blask Index in April 2026 was still 33.6% below the January 2025 peak, and the recovery is concentrated in one segment of the market.

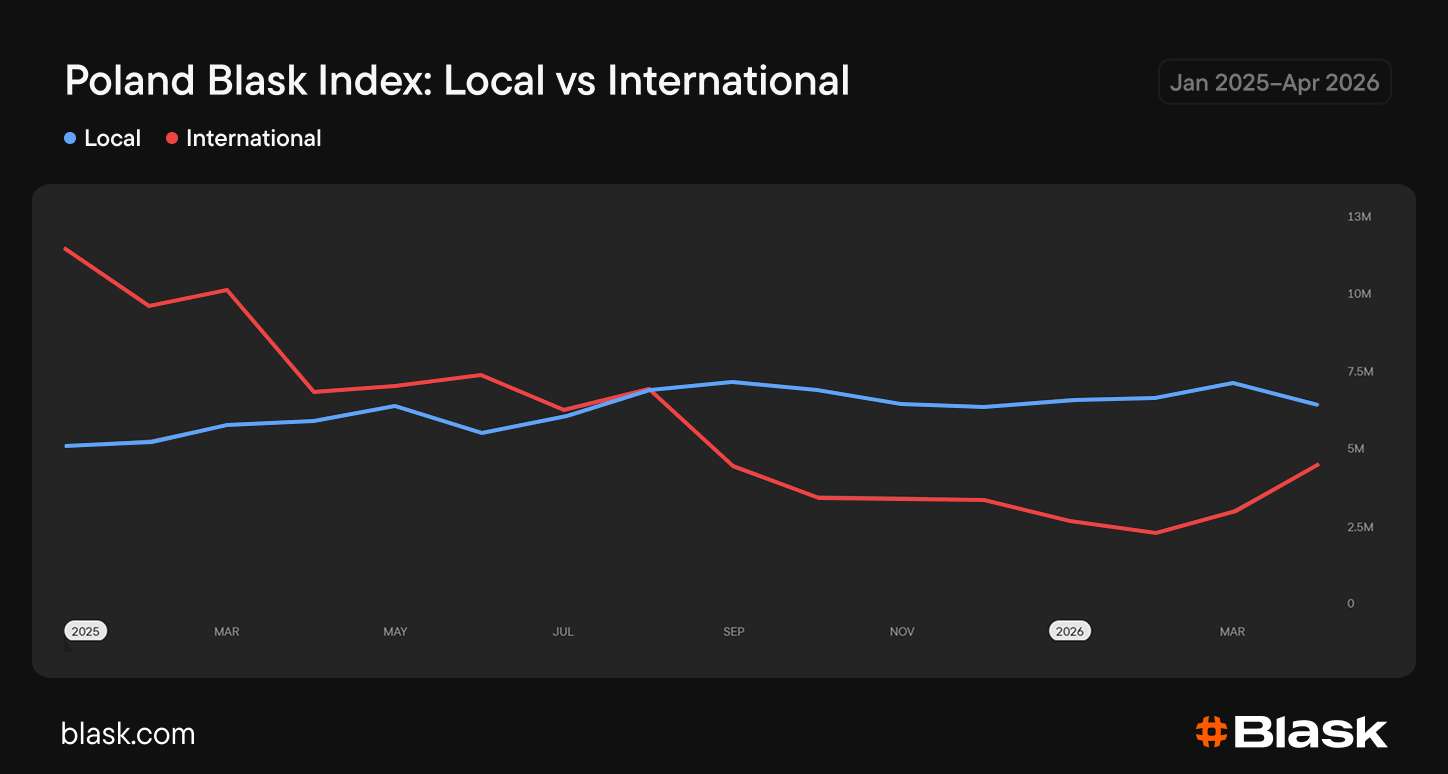

Offshore brands drove the swings

In Poland, private operators can apply for online sports betting licences only. The online casino licence is held under a legal monopoly by Totalizator Sportowy, the state operator running the Total Casino brand.

Locally licensed brands’ Blask Index has barely changed since January 2025. Blask Index of international brands fell sharply through 2025 as the Ministry of Finance expanded domain blocking, payment blocking and enforcement against the offshore segment of the market. Its Blask Index bottomed in February 2026 alongside the country’s total. In March and April it rose again — and the country-level rebound is almost entirely that rise.

The share of local brands in Blask Index rose from 31% in January 2025 to 56.8% in April 2026. Total Casino’s share is currently 19.9%.

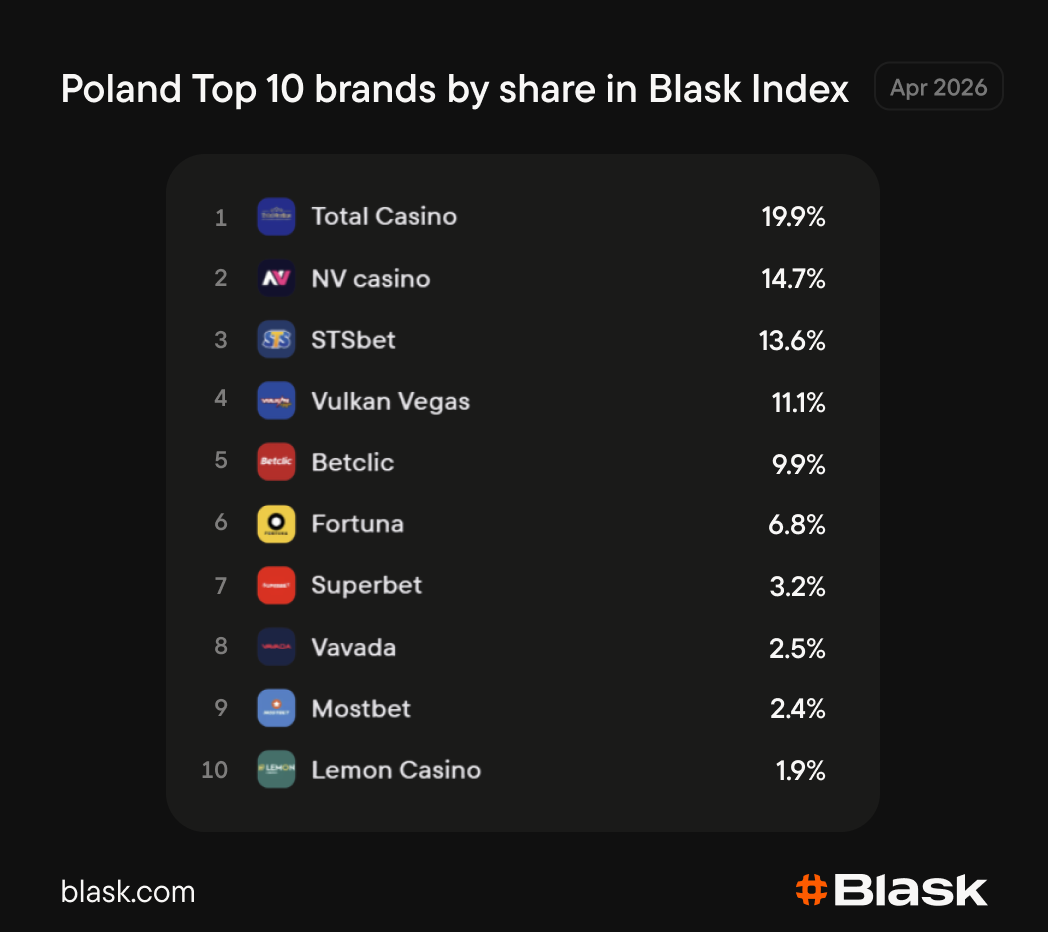

The top 10 brands account for 85.8% of Poland’s Blask Index. Only half of them are licensed, but they control 53.4% of the country’s iGaming demand, leaving only 3.4% to the other 16 licensed brands.

Industry is pushing for reform

Poland’s four largest private operators (STSbet, Betclic, Fortuna and Superbet) would be among the clearest beneficiaries if the country demonopolised the online casino vertical.

The licensed industry’s trade association has made the public case for a full multi-licence model in line with most of the EU, with a narrower sublicensing arrangement floated as a possible interim step. The argument is that casino channelisation under the monopoly sits at roughly 60%, with the remaining 40% moving to offshore operators.

The state has chosen a different path. The Ministry of Finance set up a dedicated gambling regulation department in October 2024 and an interministerial team for combating the grey market in April 2025 — both built around enforcement rather than reform.

Years of debate have produced no policy change.

Bottom line

Poland’s iGaming market is back to growth, with the recovery concentrated in the offshore segment. Licensed brands gained share through the downturn, but only because regulatory pressure squeezed unlicensed operators faster than the market shrank. When demand recovered, it returned to the same brands the regulatory framework is meant to push out.