- Updated:

- Published:

Peru casino games in 2026

Pragmatic Play owns the shelf, but player demand has moved elsewhere

Peru’s online casino market is large, well stocked, and structurally layered. Roughly 12,400 games are listed across about 50 active brands tracked by Blask, giving operators enough depth to build extensive slot catalogs while still maintaining meaningful space for crash, live, instant-win, and other specialist formats.

At first glance, the market still looks like a conventional slot ecosystem. Slots dominate the catalog, and familiar franchise titles occupy much of the visible shelf. But Peru is no longer defined by slot depth alone. Player attention is increasingly shaped by a wider mix of mechanics: mine-style games, crash formats, live entertainment, and high-recognition standalone titles.

Peru is strategically interesting because the market is evolving beyond its slot-first foundation, with attention becoming more varied than the shelf structure alone would suggest.

Blask game metrics overview

GVR (Game Visibility Rank) — Blask’s daily measure of how games are positioned across operator lobbies. Lower GVR means higher placement.

SoI (Share of Interest) — a search-based metric that shows how much player attention each game captures within a market, expressed as a percentage of total casino game interest.

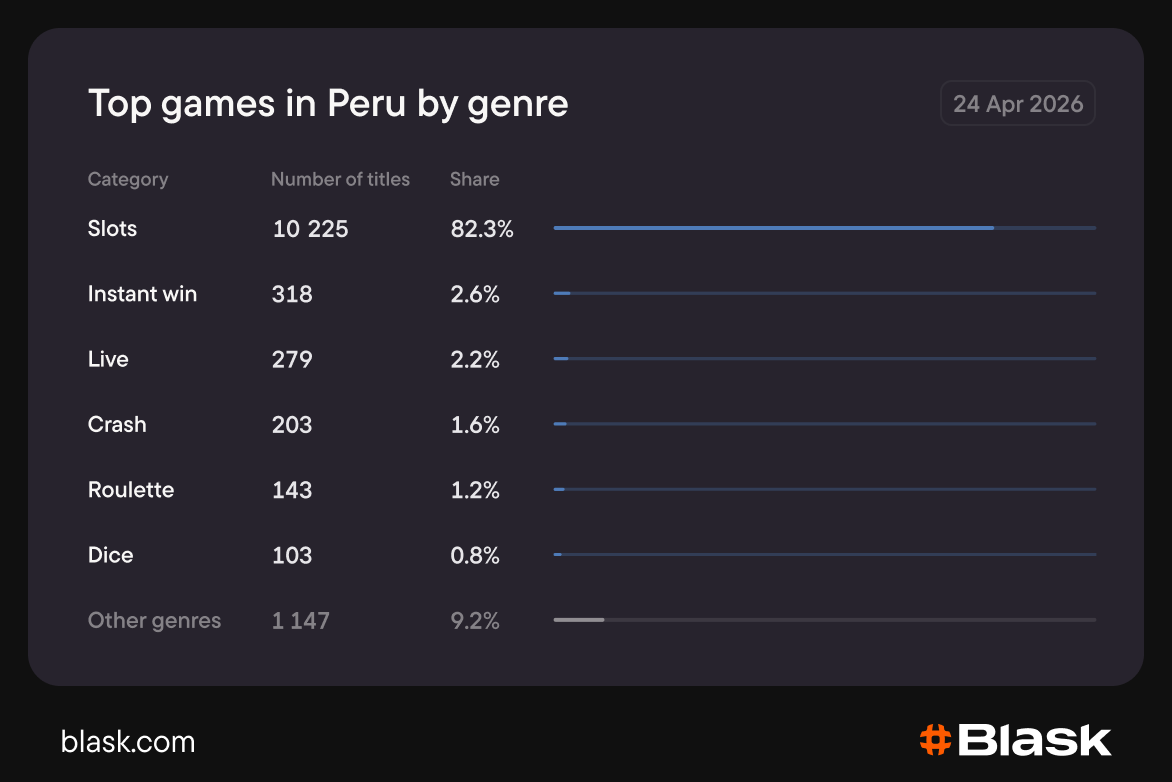

Genre distribution: a slot-first market with room for alternative mechanics

Peru is still unmistakably a slot-led market. Slots form the backbone of operator inventories and define the overall shape of the catalog. That remains the standard commercial playbook: build scale through slot depth, then use smaller categories to add rotation, novelty, and session variety.

The secondary layer is broad enough to matter. Instant win, live, and crash all have visible catalog presence, while roulette, dice, and other niche formats continue to occupy smaller specialist pockets. The market maintains a meaningful experimentation layer around the same slot-heavy template.

Peru’s catalog is still built like a slot market, but the titles capturing player attention come disproportionately from the smaller categories and from games that do not dominate the top shelf in the usual way.

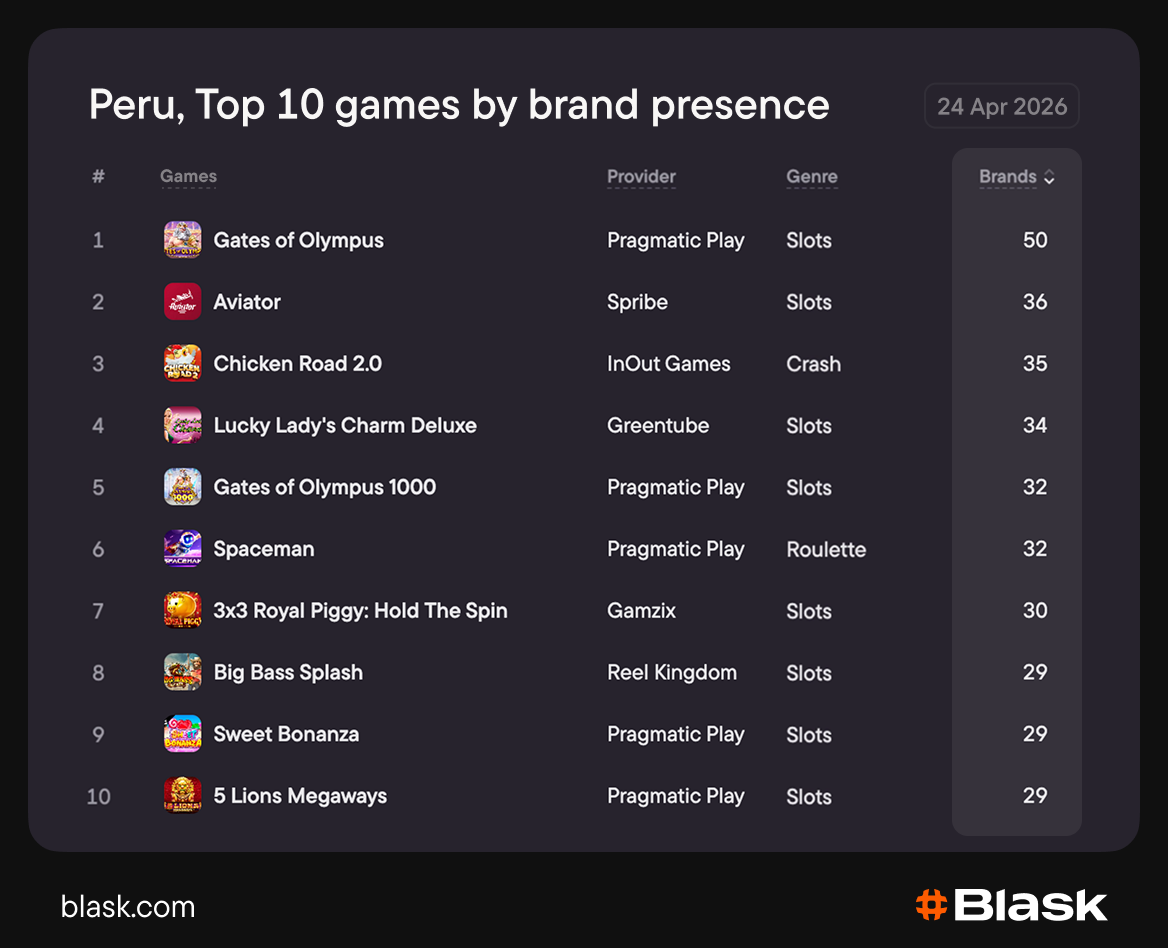

The distribution table: most-carried titles

Pragmatic Play has the strongest single-provider footprint, with several titles spread across the top tier of brand presence. This pattern is about franchise scale: the provider extends shelf control through a cluster of recognizable titles, covering both slots and crash.

At the same time, Peru’s supply is mixed. Aviator, Chicken Road 2.0, and Lucky Lady’s Charm Deluxe all hold strong cross-brand distribution, giving the top table a more varied shape than in markets where one provider occupies nearly every visible position.

Pragmatic Play remains the market’s main merchandising force, but operators are not building the shelf around a single slot ecosystem alone. They are also allocating meaningful space to crash titles and to a small group of non-Pragmatic slot products that have proved portable across brands.

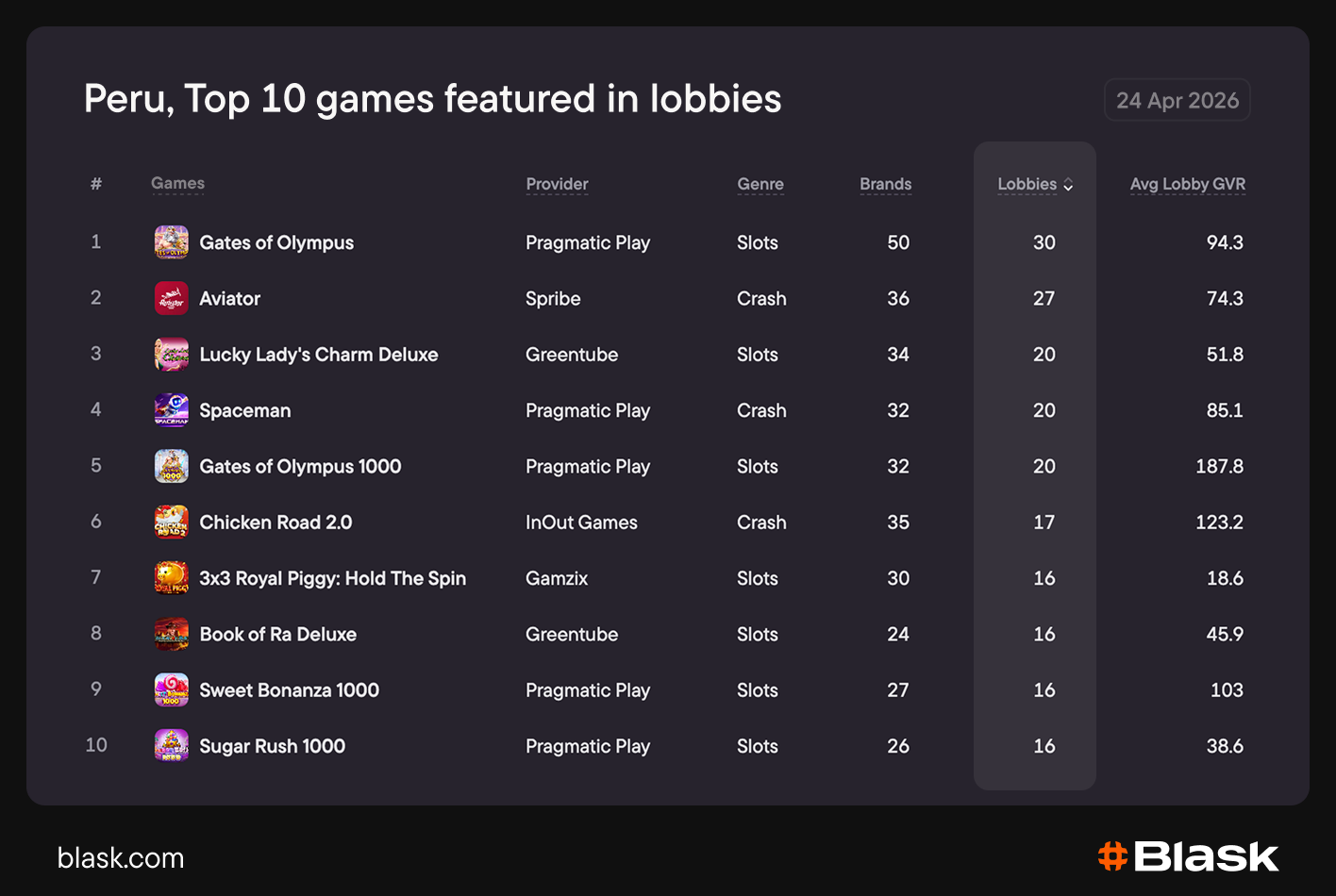

Who gets the lobby’s hero tiles

Gates of Olympus clearly functions as a hero title in Peru: it appears broadly across operator front screens, but its placement quality is weaker than that visibility alone would suggest. In other words, it is widely featured, yet not consistently anchored near the top rail.

That tension runs through much of the upper lobby table. Aviator, Spaceman, and Chicken Road 2.0 all secure meaningful lobby presence, confirming that crash titles are part of the hero inventory. But in most cases they operate more as visible support titles than as true front-screen anchors.

The clearest outlier is 3×3 Royal Piggy: Hold The Spin. It appears on fewer lobbies than the most widely featured titles, yet earns the strongest placement quality in the top group. It is the market’s best high-conviction merchandising pick: less broadly distributed, but placed far more prominently when selected.

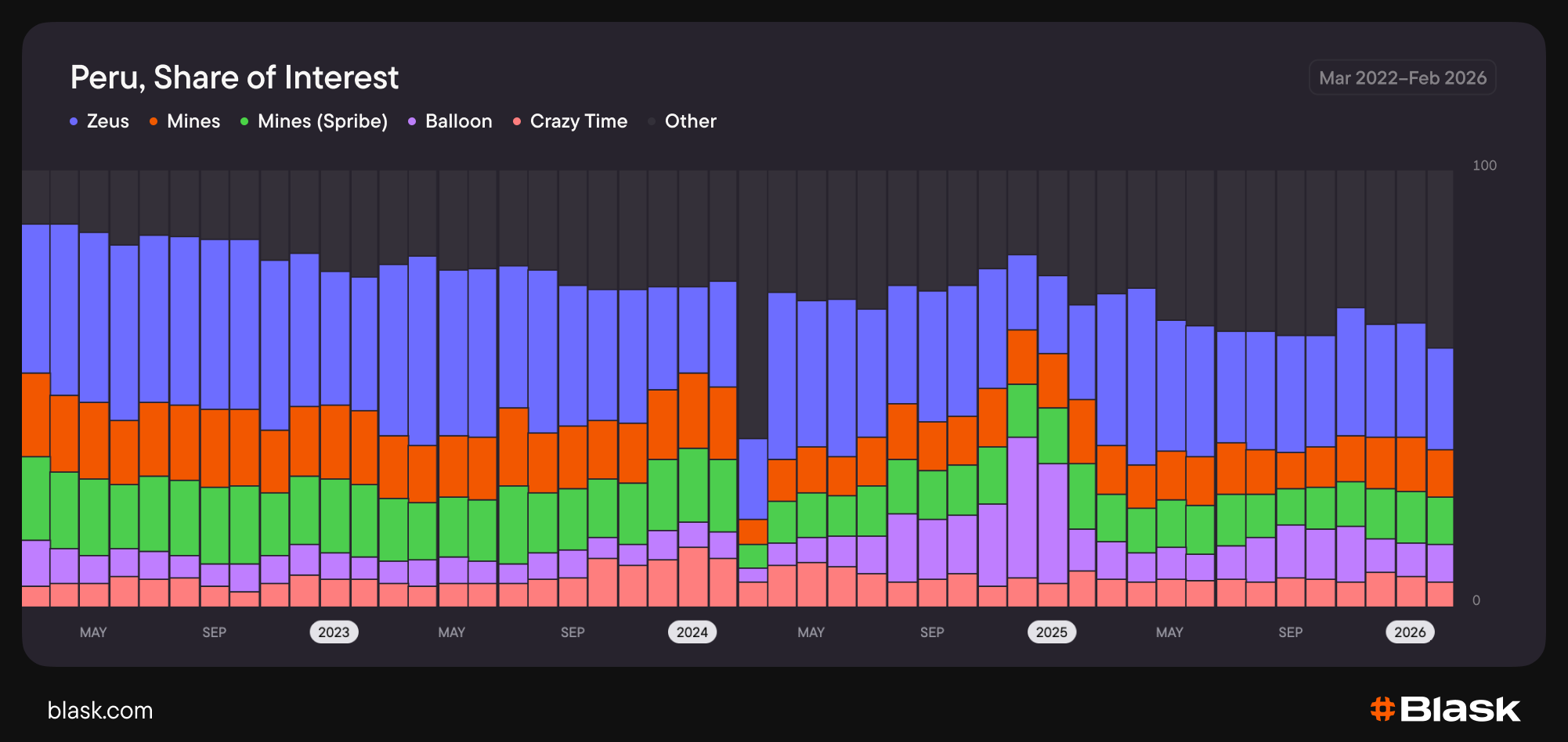

Historical share of interest: from fragmented attention to new mechanic-led demand

Peru’s long-term demand is spread across several titles. The market has repeatedly rotated through different mechanics.

From 2022 into 2023, Zeus already held the leading share of player interest, though within a more competitive field than later in the period. Over time, its position strengthened and became more clearly defined, but still without turning the market into a single-title system.

Across 2024 and into 2025, alternative mechanics rose. Mines, Balloon, and Crazy Time all expanded their presence in the interest mix, while the “Other” layer continued to occupy a meaningful share rather than collapsing under one runaway winner. Early 2025 shows the clearest break: the distribution of interest becomes more mechanic-led, with crash and mine-style products taking a larger role in the market narrative.

The market is more diversified than the shelf suggests. Demand is shaped by a rotating mix of slots, crash formats, mine-style products, and live entertainment.

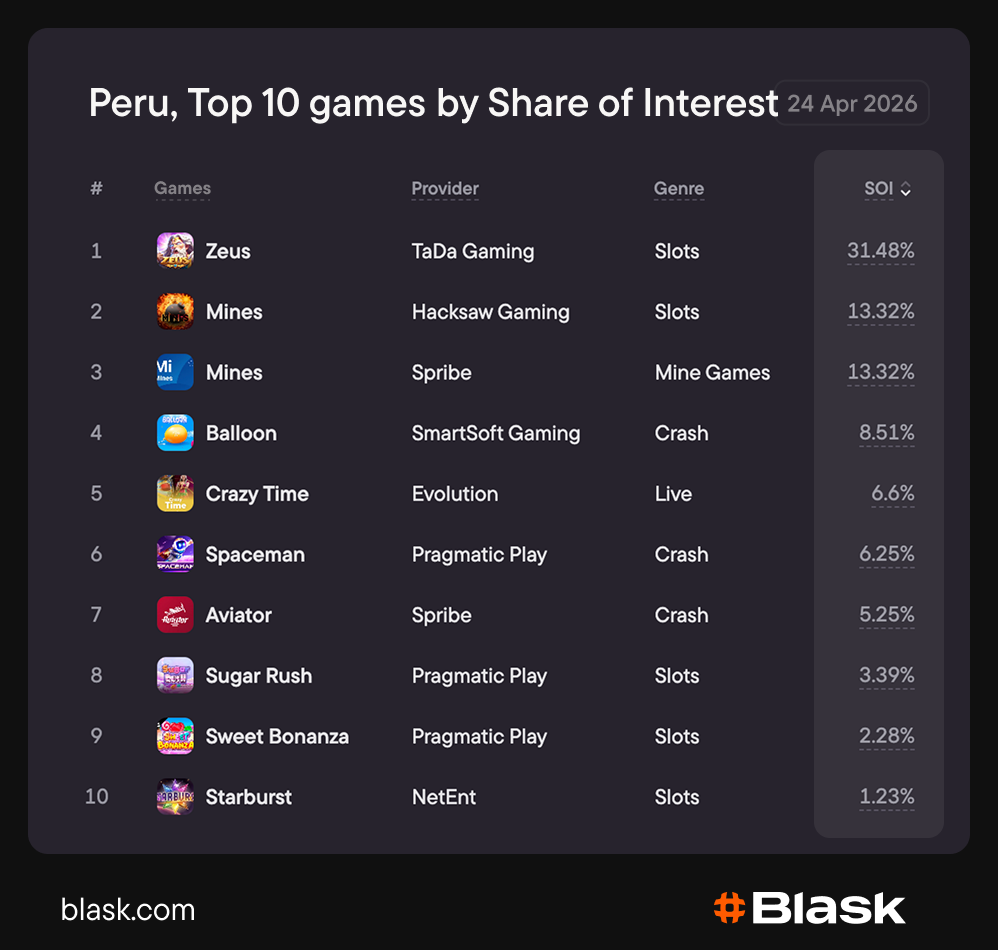

Share of interest — current snapshot (April 2026)

Peru’s current demand is shaped less by classic slot hierarchy and more by a small group of games with strong, repeatable engagement loops. Zeus remains the clearest attention leader, while two separate Mines products, Balloon, and CrazyTime form the rest of the market’s core interest cluster.

The mix itself is the point. Peru’s demand layer combines slots, mine-style products, crash mechanics, and live entertainment. Peru has a broader behavioral profile than a typical slot-led market, with player attention spreading across different play patterns rather than concentrating around a single content model.

Pragmatic Play still holds a visible place in the interest table through Spaceman, Sugar Rush, and Sweet Bonanza, but the market’s center of gravity sits elsewhere. The strongest attention drivers are the games that deliver sharper mechanics, faster decision cycles, and more distinctive session logic.

The key point is composition. Peru’s market is still built on slot depth, yet player attention is organized by a more varied set of formats. Peru is more flexible, more rotation-driven, and more open to breakout products than a standard franchise-led casino ecosystem.

The bigger picture

Peru is still built like a slot market, but it no longer behaves like one in a narrow sense.

Operators continue to rely on the familiar commercial logic of slot depth, franchise visibility, and broad catalog coverage. That remains the foundation of the market. But player interest is no longer shaped primarily by one provider, one franchise family, or even one category.

That makes Peru more flexible than the average franchise-led casino ecosystem. The market still rewards recognizable shelf brands, but it is increasingly open to games that create sharper engagement loops and stronger standalone identity. The key shift is away from a slot-defined attention model.

For operators and providers, that changes the meaning of competitiveness. In Peru, scale still matters — but so does format diversity, placement conviction, and the ability to break into a market where player attention rotates more freely than the catalog structure suggests.