- Updated:

- Published:

Uganda’s gambling revenues grew 18x in a decade. Now parliament wants 30% from every operator

Uganda has tabled two bills that would raise the betting tax rate to match casino, add a player-level levy on net winnings, and put the country among the highest-taxed gambling markets in Africa.

Finance Minister Matia Kasaija published the Lotteries and Gaming (Amendment) Bill, 2026 in the Uganda Gazette on March 27. The bill proposes to harmonise betting and gaming under a single 30% GGR rate. A second measure, the Income Tax (Amendment) Bill 2026, would add a 15% withholding tax on net winnings from both betting and gaming. Both bills were received by parliament on March 31. If passed, they take effect on 1 July 2026.

The wider context is a regional shift. Kenya’s Finance Act 2025 introduced a 5% excise duty on wallet deposits and a 5% tax on withdrawals from betting accounts, effective July 2025. In February 2026, the Lagos State Lotteries and Gaming Authority implemented a 5% withholding tax on online betting winnings. Uganda’s proposals are more aggressive on the operator side — 30% GGR is well above what most African markets impose — but the player-facing charge follows the same pattern.

How Uganda regulates gambling

Uganda’s gambling sector is overseen by the National Lotteries and Gaming Regulatory Board (NLGRB), operating under the Lotteries and Gaming Act 2016. The NLGRB licenses operators, oversees tax collection, and runs enforcement against illegal activity.

The current tax structure dates from the 2023 amendment, which introduced a two-tier model based on perceived harm and operator margin:

— Casino and gaming: 30% GGR

— Sports betting: 20% GGR

The 2026 bill closes the gap by applying 30% to betting as well. The accompanying Income Tax bill adds a new 15% withholding on net player winnings — a second tax layer that the 2023 framework did not include.

The government’s rationale is explicitly fiscal. Government data shows gaming-related tax revenues grew from Shs17.4 billion in the 2015/16 financial year to Shs323 billion in 2024/25 — an 18x increase over nine years, with collections accelerating sharply: Shs110 billion in 2021/22, Shs194 billion in 2023/24, and Shs323 billion in the latest year. The sector is described by officials as a significant contributor to domestic revenue, supporting more than 10,000 jobs.

The Ugandan gambling market in numbers

Uganda generated a projected $119.4M in CEB in 2025, according to Blask data — placing it fifth among major African markets.

| Market | CEB 2025 (avg) |

|---|---|

| South Africa | $3.1B |

| Nigeria | $633.6M |

| Tanzania | $442.1M |

| Kenya | $413.5M |

| Uganda | $119.4M |

| Zambia | $108.9M |

| Ethiopia | $47.8M |

| Ghana | $46.3M |

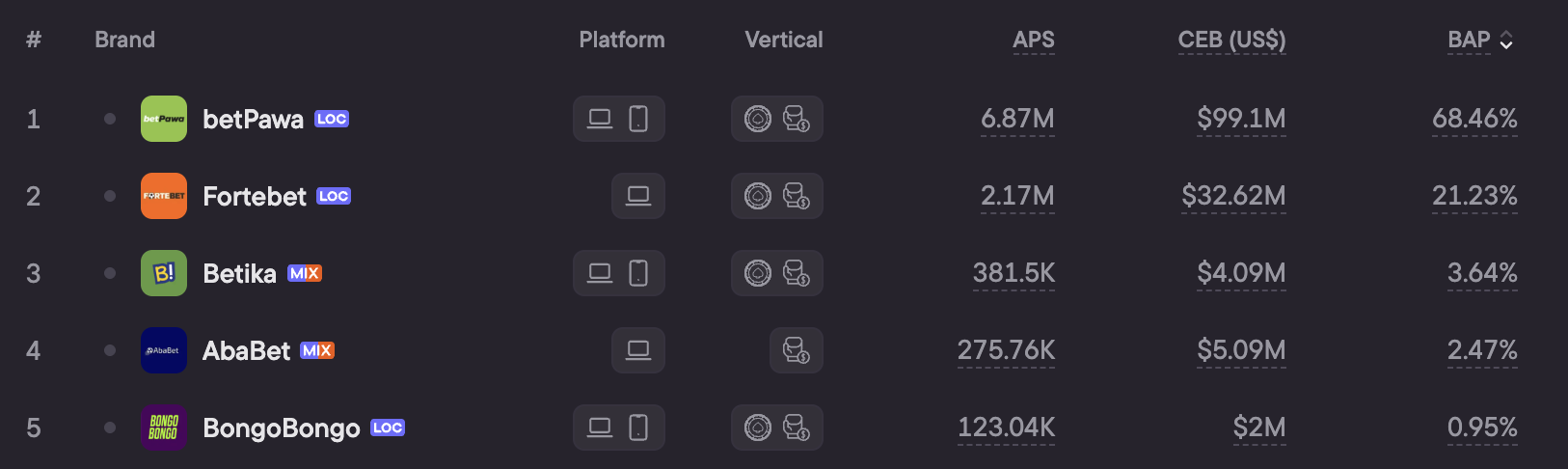

The market is tightly concentrated. betPawa led in 2025 with a projected CEB of $77.7M — 65% of the national total — posting 5.4% year-over-year growth. Fortebet held second place at $26.2M, down 2.6% YoY. The 84 remaining active brands shared roughly $15M between them, averaging under $200K in CEB per operator.

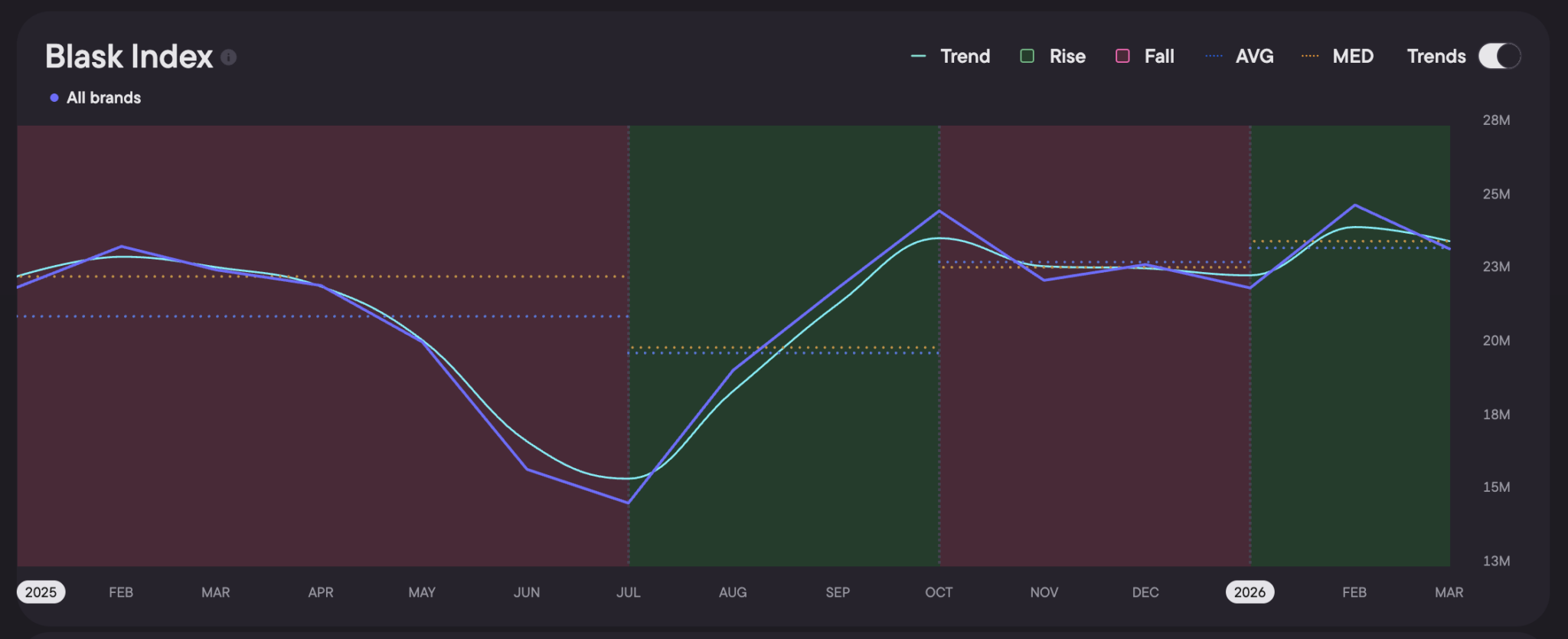

Blask Index demand in 2025 followed a seasonal curve with a sharp mid-year trough. Monthly demand held at 22–23M through Q1, then collapsed to 14.6M in July — a 37% drop from the February peak — before recovering strongly through Q4. By October, monthly demand reached 24.5M, the year’s high. Q1 2026 shows the market holding that momentum: CEB is tracking at $10.4–10.9M per month, in line with Q4 2025.

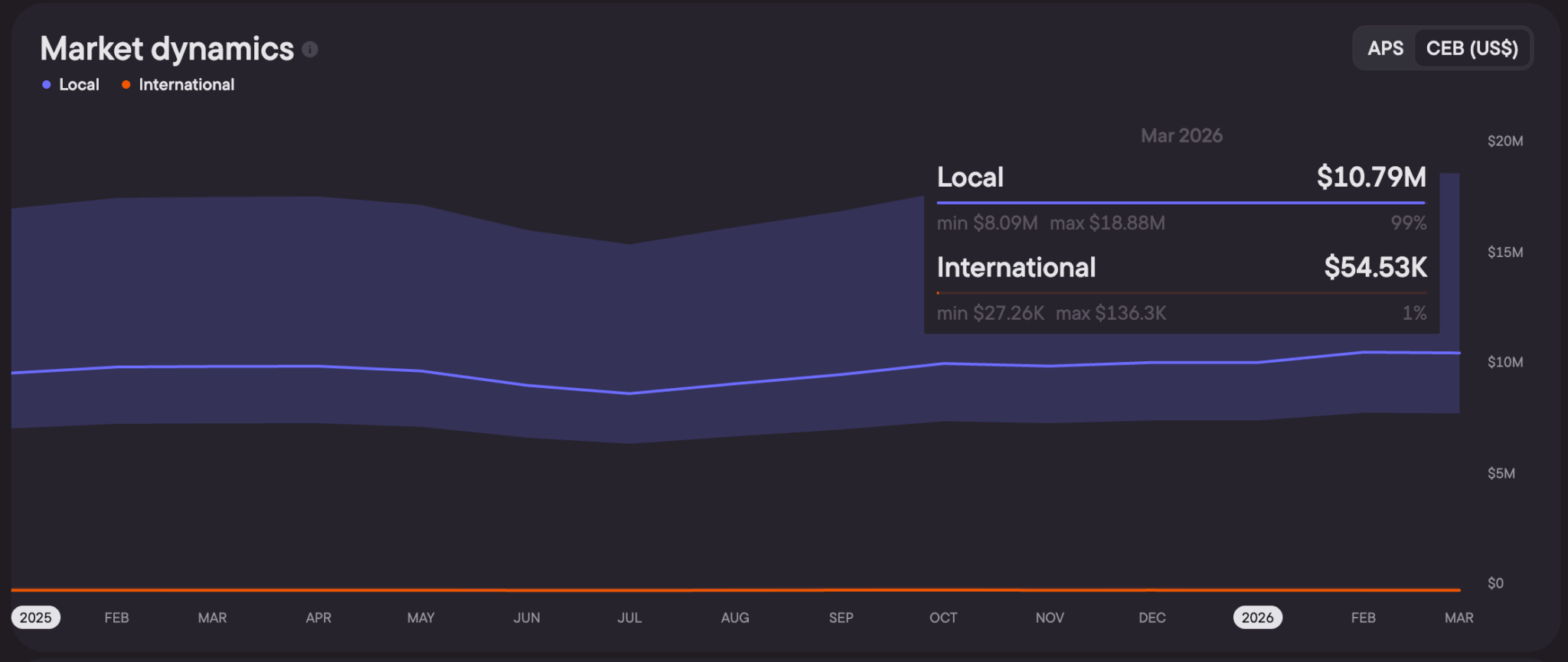

On the onshore/offshore split: licensed operators account for 99.7% of Uganda’s Blask Index demand, with offshore brands holding a stable 0.3% BAP throughout 2025. In CEB terms, that translates to roughly $700K out of $119.4M — under 1%. Industry estimates from H2 Gambling Capital place offshore gross win at around 26% of total interactive GGR. The gap reflects channel differences: informal operators run largely through retail, USSD, and SMS, which generate no search signal. By digital demand, the licensed market is essentially unchallenged.

Where the market stands

Uganda is not an emerging market. betPawa and Fortebet have operated since 2015 and 2016 respectively. The NLGRB framework is established. There are 86 active tracked brands, the structure is fixed.

But it is also not a mature, high-ceiling market. At $119M in projected CEB, Uganda sits well below Kenya ($413M) and Tanzania ($442M) despite comparable population size. Growth in 2025 was modest at best: the market leader grew just over 5%, most others were flat or declining, and the Blask Index ended the year only marginally above where it started.

The market is in a settled phase — demand is stable, the competitive hierarchy is clear, and there is no visible disruption on the horizon. That makes the timing of the tax increase notable. A 30% unified GGR rate plus a 15% player levy lands on a market that is not in a growth phase. Outside the top two operators, the CEB math is already thin.

Whether the tax change triggers consolidation, pushes activity into informal channels, or is simply absorbed without structural change depends largely on how well the NLGRB enforces it. The Board has historically operated under tight budget constraints — a factor that has limited both regional office coverage and digital monitoring capacity. If enforcement is uneven, the new rate could widen the economics gap between licensed and unlicensed operators in the opposite direction from what the government intends.