- Updated:

- Published:

Brazil iGaming market Q1 2026: brands, demand, and what changed

Brazil’s regulated betting market posted a 22% demand increase year-over-year in Q1 2026, but growth is concentrated: Betano now holds nearly a quarter of total market demand while Esportes da Sorte lost 37% of its signal following a year of licensing turbulence.

Brazil entered 2026 with its first full year of regulated sports betting behind it. The market generated BRL37 billion ($7 billion) in GGR over that first year — a figure that validated what many operators bet on when they entered. Player demand held into Q1 2026: the Blask Index hit 679 million, up 21.8% from 558 million in Q1 2025.

But the growth isn’t distributed evenly. Betano stretched its lead. Superbet nearly doubled its demand signal. And Esportes da Sorte, which spent January 2025 operating under a court injunction rather than a formal license, shed over a third of its player demand.

Three things define Q1 2026 in Brazil: the regulatory filter is working, concentration is rising, and the market entry window is closing fast.

About the data: The Blask Index measures consumer search demand for iGaming brands, derived from Google Keyword Planner and Google Trends. BAP (Brand Accumulated Power) shows each brand’s share of total market demand, accumulated over time. All figures for Brazil, Q1 2026 (January–March).

Market demand in Q1 2026

Brazil’s total Blask Index reached 679 million in Q1 2026, up 21.8% year-over-year from 558 million in Q1 2025. That’s a market still in active expansion — 45 more brands became active over 12 months, bringing the total to 502.

The QoQ picture is less dramatic. Q4 2025 clocked 699 million — Q1 2026 came in 2.9% lower. That’s a normal seasonal adjustment: Q4 benefits from year-end promotions and holiday-period activity. The underlying growth trajectory is intact.

Player acquisition grew in step with demand. The market’s Acquisition Power Score (APS) — Blask’s benchmark for how many new customers the market’s brand positions should deliver — averaged 20.77 million in Q1 2026 (15.28M–37.23M range), up 20.7% from 17.2 million in Q1 2025. The range reflects seasonal and competitive variability: the floor assumes conservative conditions, the ceiling assumes peak campaign momentum.

Revenue benchmarks were more sobering. The market’s Competitive Earning Baseline (CEB) — Blask’s estimate of what operators collectively should be earning given their market positions — held at $1.31 billion on average ($893M–$2.58B range), essentially flat year-over-year despite the 21% rise in player demand. More players, same revenue pool. In a market where the number of licensed competitors grew from 457 to 502 active brands, each brand is fighting harder for a share that isn’t expanding as fast as the field.

Track Brazil’s full market data at blask.com/market/brazil.

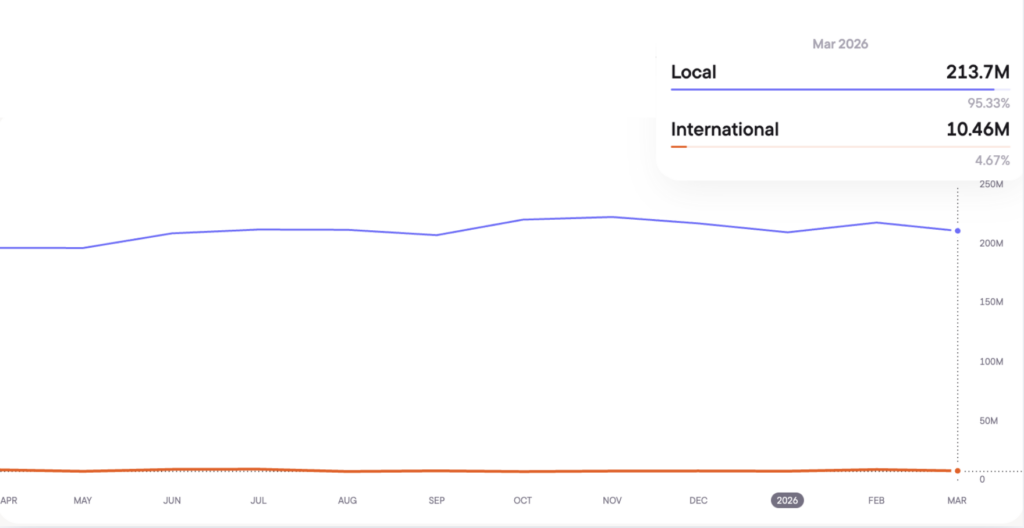

Local vs international: how the market splits

Brazil’s player demand is almost entirely domestic. Licensed local operators captured 95.3% of total Blask Index in Q1 2026, up from 93.0% in Q1 2025. That 2.3-point shift reflects a full year of enforcement: 25,000+ unlicensed sites blocked and 71 local authorizations issued.

The revenue picture is more complex. Local operators hold 95% of demand but only 71.8% of estimated CEB. International (offshore) operators generated $370.2M in average quarterly CEB — 28.2% of the total — despite accounting for just 4.7% of market demand. That gap reflects a higher revenue yield per player: offshore operators tend to attract higher-value bettors who aren’t being fully captured by local brands.

Both metrics are moving in the same direction.

| Q1 2025 | Q1 2026 | Change | |

|---|---|---|---|

| Blask Index — local | 518.3M (93.0%) | 646.8M (95.3%) | +24.8% |

| Blask Index — international | 39.3M (7.0%) | 32.2M (4.7%) | –18.1% |

| CEB — local (avg/month) | $267.7M (61.3%) | $314.7M (71.8%) | +17.6% |

| CEB — international (avg/month) | $169.2M (38.7%) | $123.4M (28.2%) | –27.0% |

International operators lost 10.5 percentage points of CEB share in 12 months. Offshore demand fell 18.1% as players migrated to licensed platforms. The trajectory is clear: each quarter of regulatory consolidation transfers both players and revenue to the licensed local tier. For international operators still weighing Brazil market investment, the window to build a defensible position on local terms is narrowing.

Top brands in Q1 2026

Rankings by BAP (Brand Accumulated Power). Blask Index estimates are calculated from quarterly Blask data; BAP reflects long-term accumulated demand and may diverge from single-quarter snapshots.

| Rank | Brand | BAP % | Blask Index Q1 2026 | YoY change |

|---|---|---|---|---|

| 1 | Betano | ~25.0% | ~169.5M | ↑ +30.3% |

| 2 | Bet365 | ~10.9% | ~74.1M | ↑ +12.2% |

| 3 | Sportingbet | ~6.5% | ~43.9M | → +0.1% |

| 4 | Superbet | ~7.4% | ~50.3M | ↑ +98.1% |

| 5 | 7Games | ~4.9% | ~33.0M | ↑ +29.5% |

| 6 | Esportes da Sorte | ~4.1% | ~27.5M | ↓ –37.4% |

| 7 | Betnacional | ~3.8% | ~25.7M | ↓ –15.9% |

| 8 | EstrelaBet | ~2.2% | ~15.1M | → 0% |

| 9 | Vaidebet | ~1.8% | ~12.1M | ↓ –14.6% |

| 10 | Onabet | ~1.8% | ~12.4M | ↓ –10.8% |

Betano is the undisputed market leader. Its +30.3% year-over-year growth reflects sustained brand investment and deep sports sponsorship across Brazil. At roughly 25% of all market demand, no other operator comes close.

The most striking move of the quarter belongs to Superbet.

The Romanian operator nearly doubled its Blask Index year-over-year (+98.1%), pushing its quarterly Blask demand above Sportingbet — even if accumulated BAP still has Sportingbet ranked third. Superbet entered Brazil in late 2023 and spent 18 months building brand presence through partnerships and marketing spend. Q1 2026 is the clearest sign yet that it’s converting.

Esportes da Sorte took the largest fall in the ranking group. The brand posted a –37.4% year-over-year decline — the steepest drop among major operators. That erosion didn’t happen in a single quarter: it’s the accumulated effect of spending the opening weeks of Brazil’s regulatory era operating under a court injunction rather than a formal SPA authorization. Player trust eroded across 2025, and it shows in the Q1 2026 numbers.

Sportingbet’s position is quietly fragile. With +0.1% year-over-year growth in a market up 21.8%, flat is a relative decline. The brand holds its #3 rank on accumulated historical demand, but the gap to Superbet — which grew the quarterly Blask signal to ~50M vs Sportingbet’s ~44M in Q1 2026 — is closing.

What drove the quarter

- Regulation concentrated demand. Brazil’s Secretariat of Prizes and Bets (SPA) spent Q4 2025 through Q1 2026 hardening the licensing framework. By February 2026, SPA had approved 71 total operator authorizations, adding 21 in one batch. Simultaneously, Brazil blocked over 25,000 illegal betting sites during 2025. The effect is straightforward: shrink the gray zone, push demand toward licensed operators. Brands with proper authorizations from day one benefited directly.

- Esportes da Sorte’s license uncertainty cost it the year. The operator obtained a court injunction in January 2025 to continue operating while its formal license was in process. That legal ambiguity had lasting effects on player confidence. The –37.4% YoY decline in Q1 2026 reflects a year of brand erosion, not a Q1-specific event. Operators in legal gray zones in regulated markets pay a long-term demand tax.

- Superbet invested heavily into a growing market. The operator launched in Brazil in October 2023 and committed to local sports partnerships and marketing. In Q1 2025, its annual Blask Index was 86.5 million — up from virtually nothing in 2024. By Q1 2026, that figure had reached 171.3 million. Its +98% year-over-year growth in Q1 2026 puts it on a trajectory to challenge the top three within the next 12 months.

Q1 2026 vs Q1 2025 — year-over-year shift

| Metric | Q1 2025 | Q1 2026 | Change |

|---|---|---|---|

| Total Blask Index | 557.6M | 679.0M | +21.8% |

| Market leader | Betano | Betano | — |

| APS avg | 17.2M | 20.8M | +20.7% |

| CEB avg | $1.31B | $1.31B | +0.3% |

| Active brands | 457 | 502 | +45 |

The structural picture over 12 months: more brands, more players, flat revenue estimates. A market absorbing a wave of new operators, each fighting for a share that isn’t growing as fast as the number of competitors.

The concentration data is telling. Betano’s demand share climbed roughly 7 percentage points year-over-year. Esportes da Sorte’s share dropped by roughly 4. In a market with 500+ active brands, the top three control roughly 42% of all demand. That gap will keep widening as licensing compliance continues to sort operators.

What this means for operators

Brazil’s first-year chapter is over.

What starts in Q2 2026 is the consolidation phase. The licensing framework is set, the illegal sites are largely cleared, and the top brands have built clear demand advantages. Entry is still possible — 71 authorized operators and counting — but the cost of catching up in brand investment, sponsorships, and local partnerships rises every quarter.

For operators already in the market, Q1 2026 sends a clear signal. Betano and Superbet, both of which invested aggressively in brand visibility, are growing faster than the market. Sportingbet and several domestic operators that grew on early-mover advantage are now being outspent. In a market growing at 22% annually, flat is a declining real position.

The SPA’s 2026/27 regulatory agenda prioritizes license compliance reviews and responsible gambling enforcement. Operators with compliance gaps face risk; those with clean licenses and brand infrastructure face opportunity.

Conclusion

Q1 2026 confirmed what Q4 2025 implied: Brazil is a large, structurally growing market with a tightening competitive filter. Player demand is up 22% year-over-year, but that demand is concentrating around a smaller group of well-capitalized operators. Betano leads. Superbet is moving fast. The middle of the ranking is under pressure from both sides.

Q2 2026 will test whether the post-holiday slowdown was seasonal or structural. Later in the year, the FIFA World Cup will likely drive a demand surge — but the operators best positioned to capture it are the ones that already spent 18 months building brand presence and licensing certainty. That window has mostly closed.