- Updated:

- Published:

Canada iGaming market 2026: why Alberta’s launch won’t fix the 89% offshore problem overnight

On July 13, Alberta became the second province after Ontario to open a licensed market. Blask data shows that displacing offshore operators in Canada takes years, not a single regulatory launch.

Canada is the fourth-largest iGaming market among the 135 countries tracked by Blask, valued at $10.25B in CEB over the past 12 months — behind only the US, UK and Turkey — and it is growing faster than any other market in the global top five. But that scale does not translate into high channelization: most provinces outside Ontario still rely on closed monopoly models that capture only a limited share of demand.

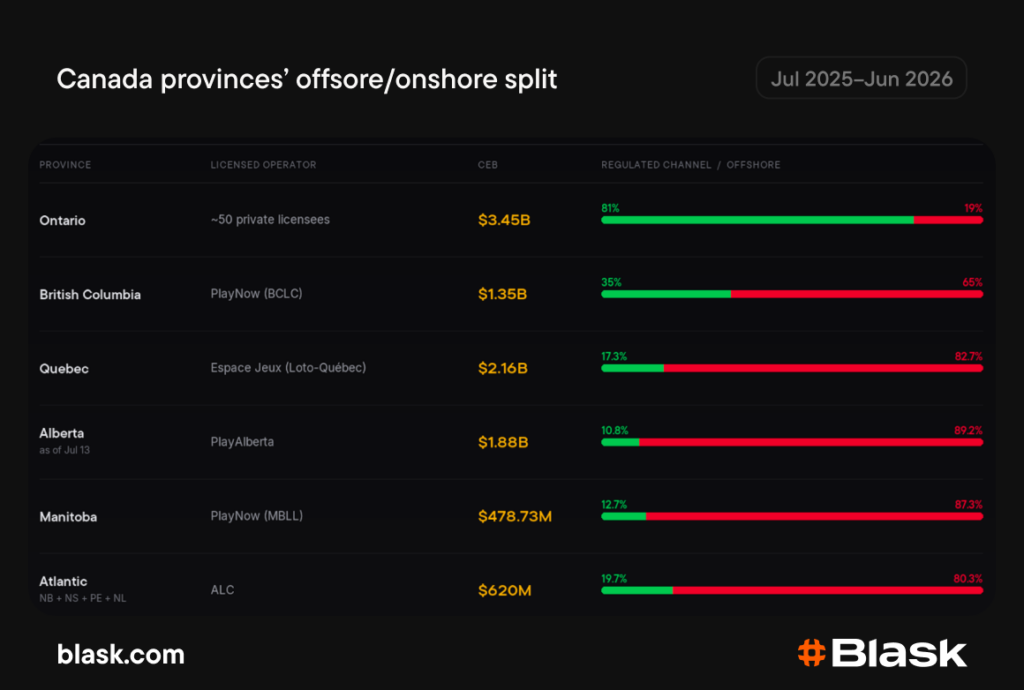

Offshore dominates almost the entire market except Ontario

For the Canada iGaming market, Blask uses CEB to estimate the potential revenue a brand can realistically capture based on search demand, visibility and competitor data.

Data for the past 12 months, from July 2025 to June 2026, shows a sharp gap between provinces:

The Canada iGaming channelization rate varies sharply by province: Ontario is the only market where the regulated channel truly dominates. That’s why the national offshore share looks noticeably lower than the often-cited 59–60%: Ontario’s large market pulls the average down. Without it, offshore controls 64.5% of the rest of Canada — close to British Columbia’s level, but still below Quebec and the other monopoly provinces.

Comparing official estimates with Blask data reveals a notable gap:

- British Columbia: Finance Minister Brenda Bailey put BCLC’s share at 51%, comparing $454M in legal turnover with $441M in illegal turnover. Blask shows 35% CEB for the regulated segment and 65% for offshore. The difference comes down to methodology: BCLC counts turnover, while Blask estimates potential revenue based on demand.

- Quebec: the operator coalition QOGC estimates the province loses more than $300M in tax revenue a year, and a Mainstreet Research survey found that only 25–27% of online players use Espace Jeux. Blask puts the regulated segment’s CEB share at 17.3%.

Ontario’s lesson: channelization started fast, but took years to mature

Ontario opened its market to private operators on April 4, 2022: as iGaming Ontario reported, the number of operators grew from 12 on launch day to 46 by the end of the first year. Four years later, an Ipsos study found that 91.1% of online players used regulated platforms, while the share of players using unregulated sites exclusively fell from 16.3% to 8.9% over the year.

The Ontario iGaming offshore market share depends on how channelization is measured. Blask shows a more conservative picture: 81% of Ontario’s online CEB goes to regulated brands — 19% to offshore. The discrepancy is methodological: Ipsos counts any player who has used a legal site at least once, while Blask tracks how demand is distributed across all brands.

Ontario accelerated channelization by letting former gray-market operators get licensed without leaving the market. Alberta is starting from a harder position: Stake, Rainbet and Roobet did not apply for AGLC licenses and already hold substantial demand in the province.

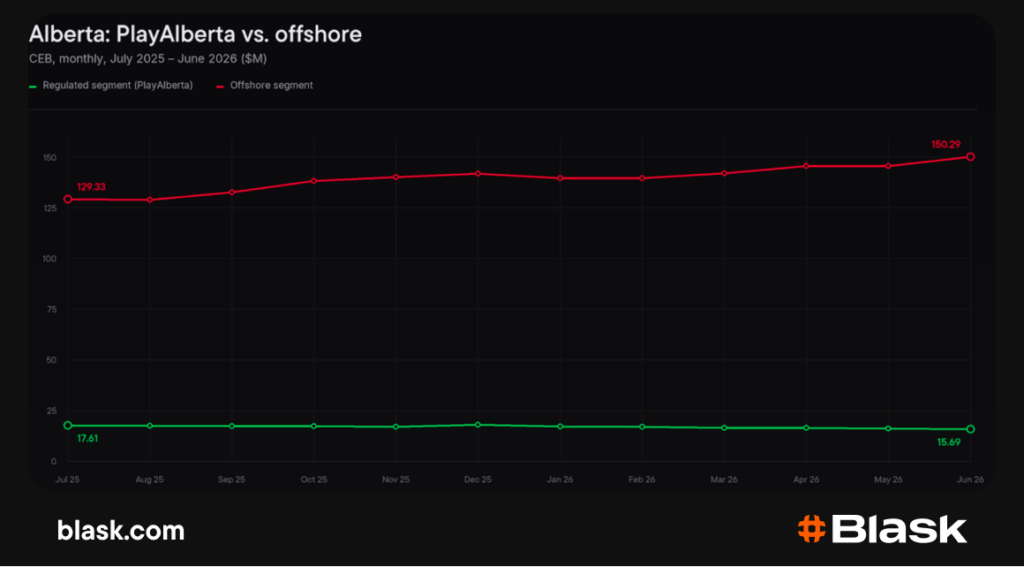

Blask data: offshore holds 89% of CEB in Alberta, and the share isn’t shrinking

Alberta regulated market offshore competition began from a heavily uneven position. Until July 13, PlayAlberta remained the province’s only licensed operator. Over the past 12 months, Alberta’s total CEB reached $1.88B. Of that, $203.1M, or 10.8%, went to the regulated segment, and $1.67B, or 89.2%, to offshore brands.

That ratio has been worsening: from July 2025 to June 2026, the regulated segment’s CEB fell from $17.61M to $15.69M a month (–10.9%), while offshore CEB grew from $129.33M to $150.29M (+16.2%).

The gap widened over the 12-month period rather than closing — a troubling signal for a market about to test channelization. PlayAlberta ranked only third, behind JackpotCity and Stake, while its CEB fell 15.93% YoY.

A single launch won’t solve the offshore problem

Canada provinces online gambling regulation remains fragmented, with competitive licensing in Ontario and Alberta and monopoly models across most of the country. The real measure of Alberta’s success isn’t the number of licenses at launch, but how demand redistributes after July 13. Blask will track three signals: a decline in offshore CEB share, growth in licensed brands’ BAP, and their appearance in the province’s top 10.