Blask data analysis, October 2025

Across the global iGaming map, a handful of countries are not just dominated: they’re owned. Blask’s Brand’s Accumulated Power (BAP) and Competitive Earnings Baseline (CEB) show how, in certain nations, one brand captures virtually all visibility, traffic, and earnings potential.

In these monopoly-style markets, dominance stems from two main forces: regulation and reach. Some states legally authorize a single operator; others are unregulated, where the first brand to scale, often with a strong Acquisition Power Score (APS), simply becomes the market.

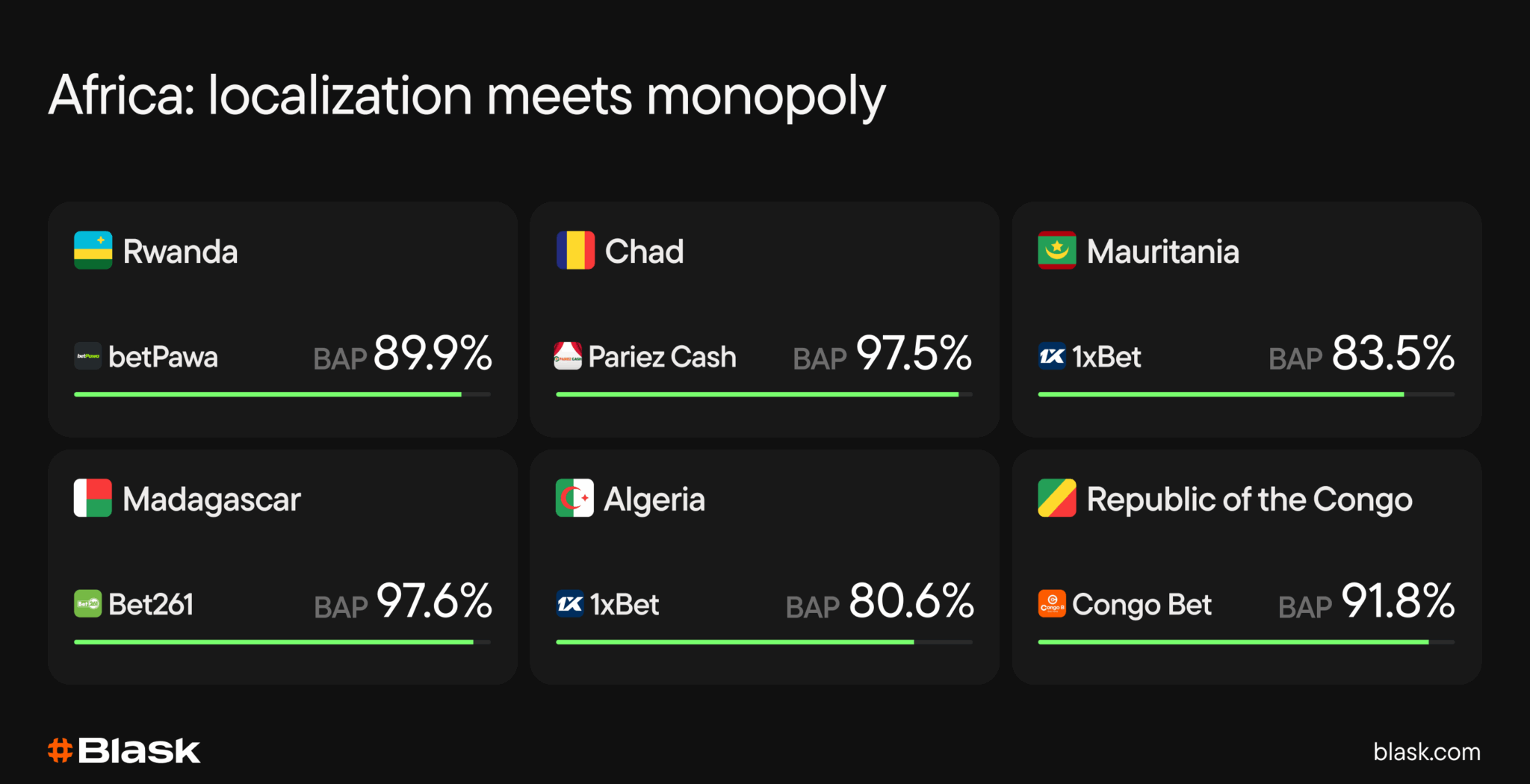

Africa: Localization meets monopoly

Africa shows the widest range of one-brand dominance: from tightly controlled local licenses to unregulated arenas where a single global operator thrives.

In Rwanda, betPawa commands 89.9% BAP with an average CEB of $34.3M and +115% YoY growth, proving how hyper-localized platforms win under clear regulation.

Unregulated Chad mirrors that concentration: Pariez Cash owns 97.5% BAP with an estimated average earning of $7.4M, up +65.9% YoY, a case of branding and simplicity resonating where few alternatives exist.

In Mauritania and Somalia, 1xBet’s international infrastructure fills the vacuum. Both markets show 83.5% BAP and 91.8% BAP, respectively, with average CEB ranging from $2.2M to $5.2M. Weak regulation and mobile penetration give the brand almost total control.

Madagascar is a hybrid case: unregulated gambling but licensed betting. Bet261 holds 97.6% BAP with $9.1M average CEB, doubling its performance year-on-year (+100.8%).

Further north, Algeria’s unregulated ecosystem has become a 1xBet stronghold with 80.6% BAP. With $96.4M average CEB and an eye-catching +149.8% YoY growth, it’s among Africa’s fastest-expanding markets.

Even in regulated systems, monopolies persist. In the Republic of the Congo, Congo Bet captures 91.8% BAP, $48.2M average CEB, and +35.4% YoY, suggesting that local licensing, not competition, defines success.

This statement is only partly true (that it’s not worth entering a market dominated by a single brand).

In Nigeria, it’s indeed true that just a few operators currently dominate the market, often setting conditions that are unfavorable for SEO teams. That’s logical, since they can rely on cheaper and more efficient player acquisition sources.

However, the market is far from being limited to these operators and remains quite interesting, especially during major events, primarily due to its scale and player activity, even if the average deposits are very low.

If you don’t treat it as a gold mine but instead aim for a satisfactory outcome by your own standards, the market can be viable at least on a seasonal basis. In the medium and long term, much depends on the actions of the regulator and the government.

African markets will gradually gain momentum. A current monopoly doesn’t mean the landscape will stay static. Even under present conditions, there’s still room to maneuver, though not as much as one might wish.

Nikita Pugachev

Head of Affiliates, Already Media

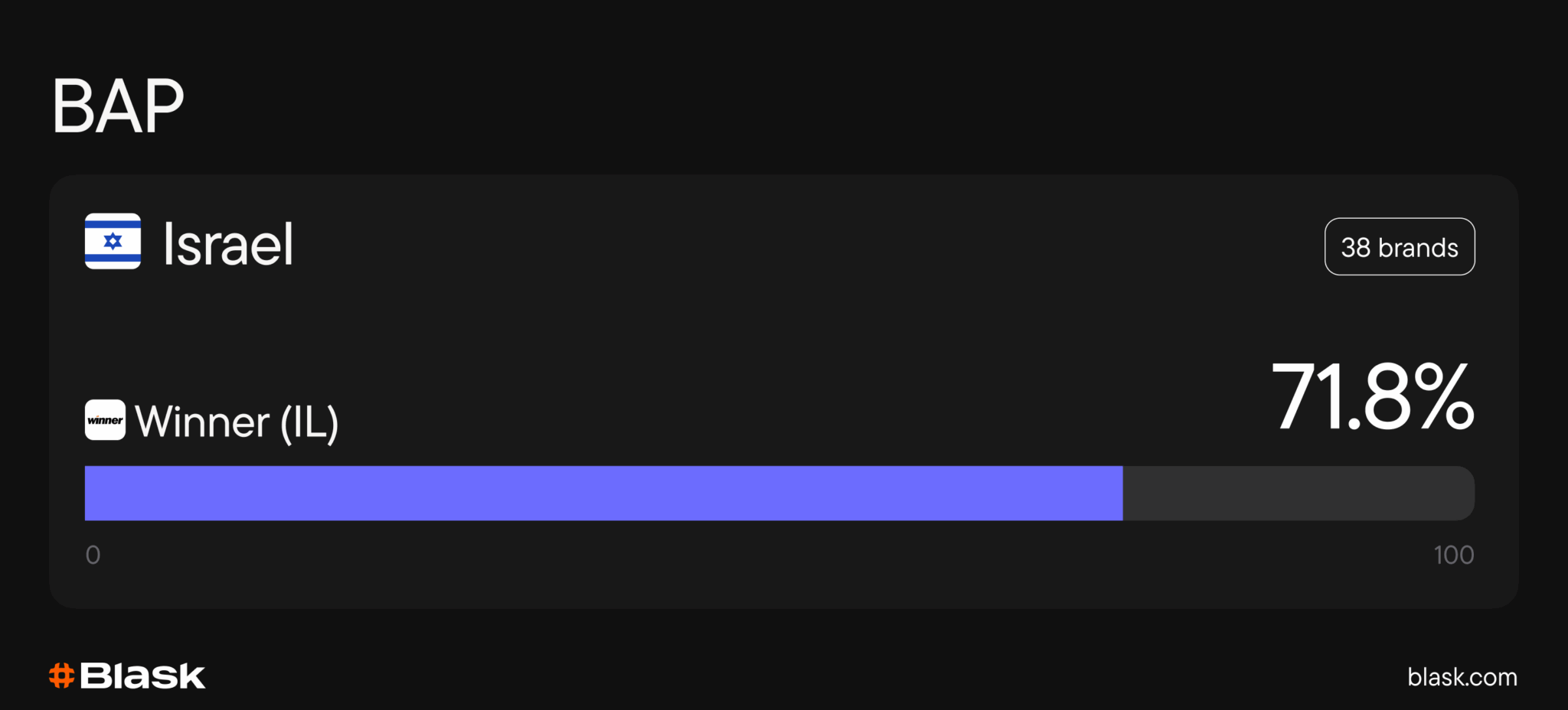

Middle East: State control, almost nonexistent competition

In Israel, the online betting scene revolves entirely around the national operator Winner (IL). With 71.8% BAP and a $283.9M Average CEB, it is one of the clearest examples of a legal monopoly. The brand’s slight –3.6% YoY dip reflects market maturity rather than vulnerability: the model leaves no room for private challengers.

Asia: Monopolies by law

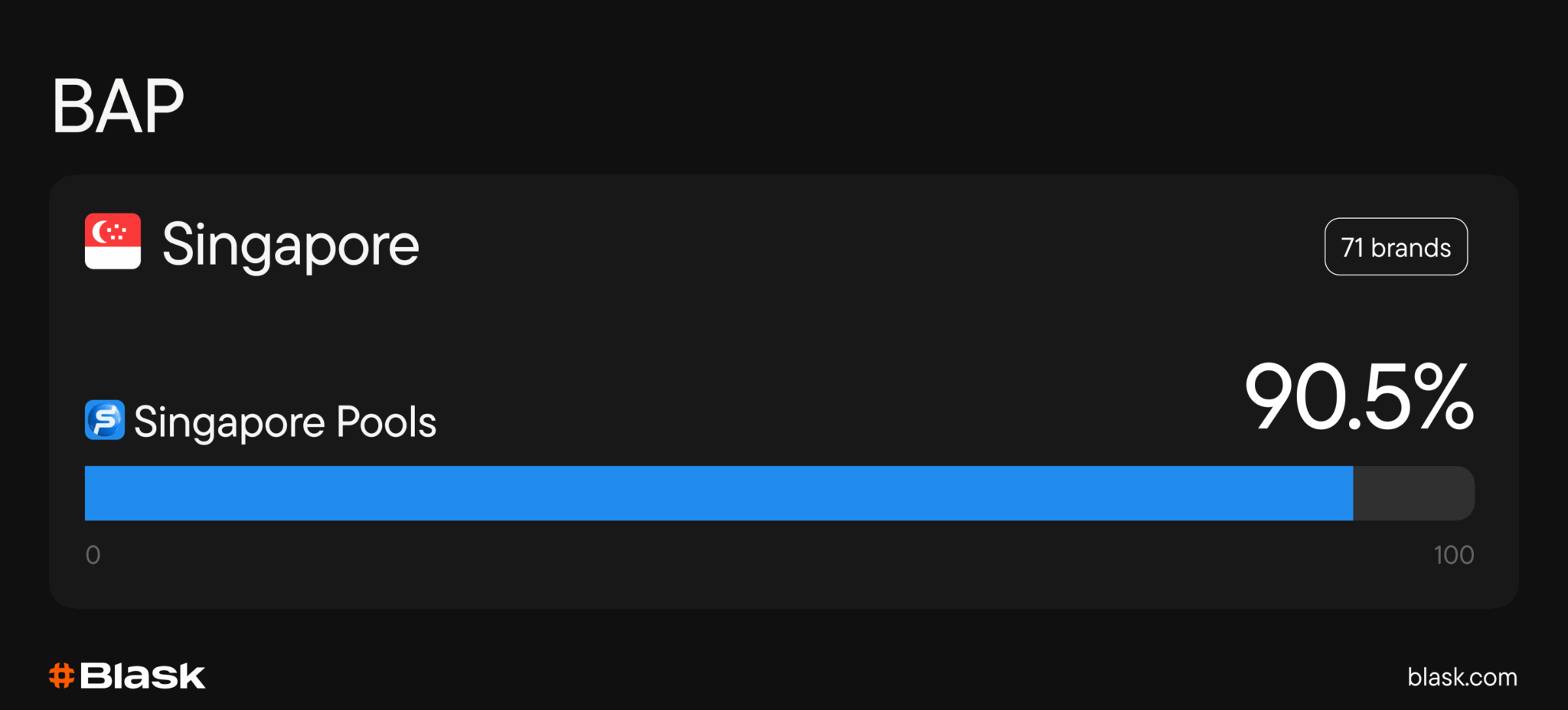

In Singapore, Singapore Pools continues to hold a near-absolute monopoly: 90.5% BAP and a remarkable $1.1B Average CEB, with a +2.1% YoY growth. The brand’s grip remains ironclad thanks to decades-old legislation that excludes foreign sportsbooks and casinos.

Europe: National lotteries dominate

Europe’s monopolies are largely by design, structured through exclusive concessions rather than competition.

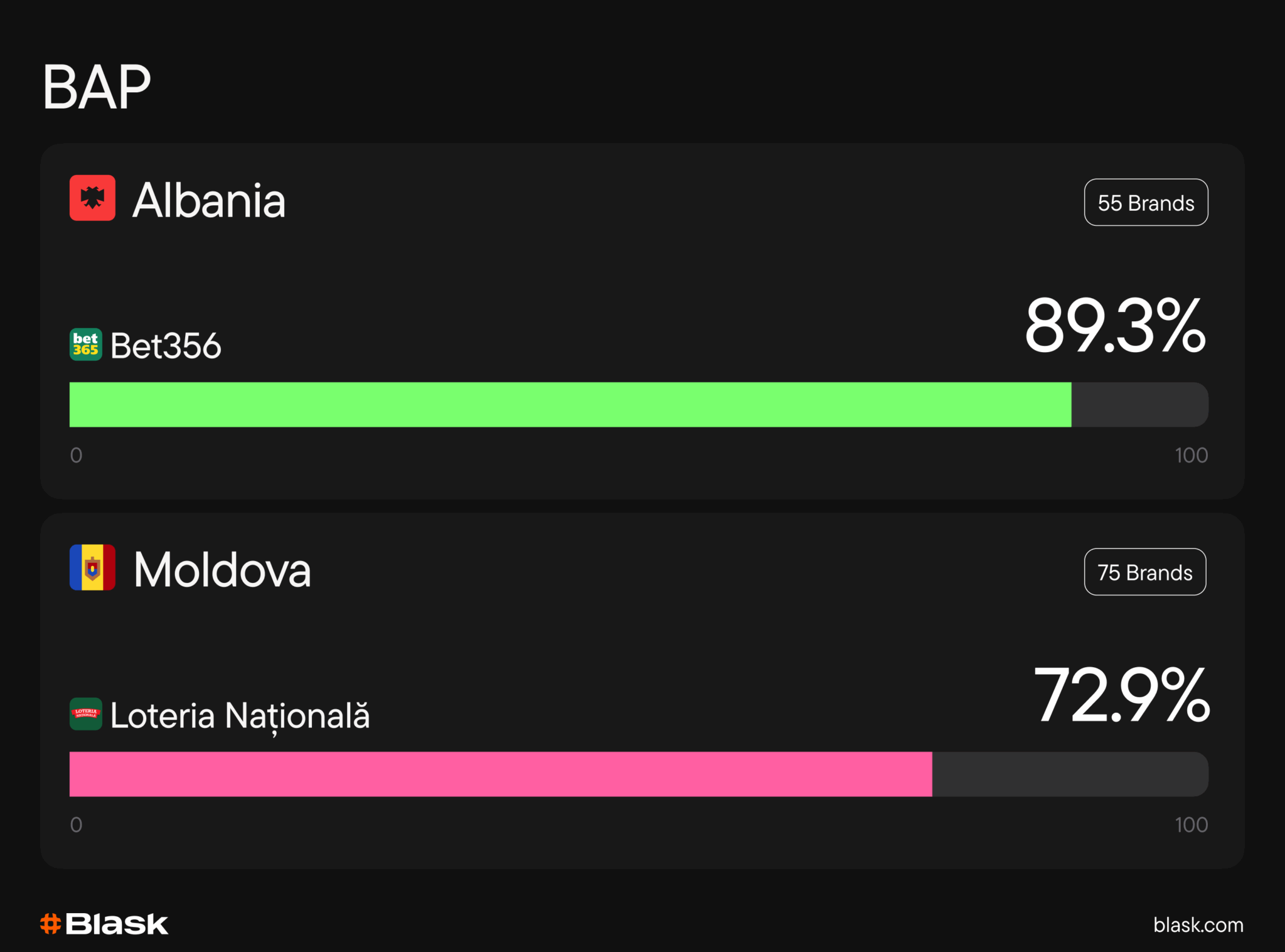

Albania’s betting market belongs to Bet365: 89.3% BAP, $41.4M Average CEB, though slightly down –10.3% YoY. Its global brand recognition and local licensing leave no space for domestic rivals.

Moldova presents a textbook state monopoly. Loteria Națională holds 72.9% BAP, $128.1M Average CEB, and –0.4% YoY. By law, it operates the country’s entire regulated iGaming sector: an arrangement that’s stable but slow-growing.

Americas: Between state exclusivity and offshore dominance

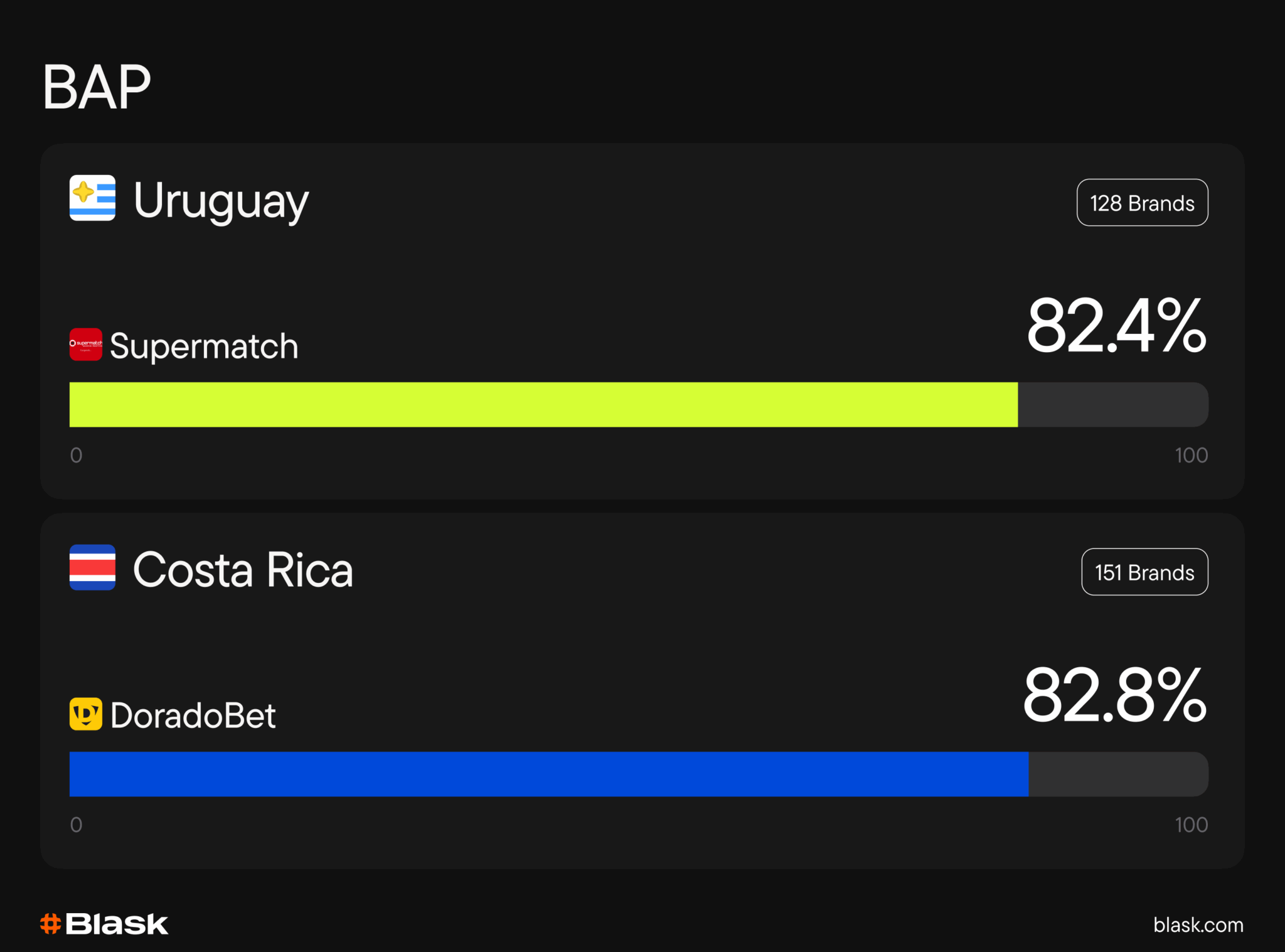

In Uruguay, the government-run Supermatch holds 82.4% BAP, $224.6M Average CEB, and a modest +9.6% YoY rise: a reflection of a mature, controlled market with steady engagement.

In contrast, Costa Rica’s unregulated environment fuels explosive private growth. DoradoBet, with 82.8% BAP, generates $9.3M Average CEB and an astonishing +174% YoY surge: the reward for early market capture and aggressive digital expansion.

Patterns: How monopolies form and endure

Two dominant models emerge from Blask’s cross-market data:

- Regulated monopolies: State-authorized operators like Singapore Pools or Loteria Națională operate under exclusive licenses, ensuring predictable revenue but minimal innovation.

- Market monopolies: In unregulated or underdeveloped markets, first movers like 1xBet or Pariez Cash dominate via brand familiarity, simplified payment options, and superior reach (high APS).

These markets may differ in structure, but their outcomes converge: over 90% of total visibility and earnings consolidated under one brand.

🚀 Discover: 30 Ways Blask Games empowers iGaming professionals

Market entry outlook: What operators should know

While monopolies might look impenetrable, they reveal strategic entry windows for emerging or expanding brands:

- In regulated monopolies (Singapore, Moldova, Uruguay), partnerships or B2B licensing with the existing operator are the only viable paths. These are stable but slow-moving environments: ideal for suppliers, not new sportsbooks.

- In transitioning or hybrid markets (Madagascar, Albania, Cameroon), operators can position themselves ahead of future liberalization. Building localized brand awareness and compliance readiness early can yield first-mover advantage once regulations open.

- In unregulated monopolies (Chad, Mauritania, Algeria), gray-market competition is fierce but fluid. Market entrants must differentiate through mobile-first UX, lightweight KYC, and localized payment systems rather than pure visibility.

- Across Africa, mobile betting infrastructure and brand localization remain the critical differentiators. Operators focusing on multi-language interfaces, micro-betting, and local payment rails stand the best chance of eroding single-brand dominance.

In short: monopolies mark both barriers and beacons. Where one operator controls the board today, the next wave of entrants can study what built that dominance, regulation, trust, or timing, and prepare to exploit its eventual limits.