- Updated:

- Published:

UK iGaming market Q1 2026: brands, demand, and what changed

Demand grew 7% and revenue 12% year-over-year, but the real story was how sharply the UK’s competitive order rearranged beneath those headline numbers.

The UK iGaming market entered 2026 under pressure from every direction: affordability checks rolling out in real time, online slots stake limits already nine months in, and a 40% Remote Gaming Duty increase looming in April. Despite all that, the market grew — 7.1% in consumer demand and 12.4% in estimated revenue year-over-year. The gap between those two numbers matters.

What changed underneath was more significant. William Hill lost close to 4 percentage points of demand share. Sky Bet shed over 2. Bet365 extended its hold on the top spot. And Entain’s paired brands — Ladbrokes and Coral — each posted over 20% demand growth, together reclaiming territory from the operators squeezed by tax and strategy pivots.

Three forces drove Q1 2026: Evoke’s structural retreat from its UK retail estate, the ongoing consolidation of demand around the strongest brands, and a regulatory environment that cost operators millions before it fully landed.

About the data: Blask Index measures consumer search demand for iGaming brands, derived from Google Keyword Planner and Google Trends. BAP (Brand Accumulated Power) shows each brand’s share of total market demand. CEB (Competitive Earning Baseline) estimates market-based revenue from brand strength and competitive positioning — not operator-reported financials. APS (Acquisition Power Score) benchmarks new customer volumes a brand’s position should deliver. All figures for the United Kingdom, Q1 2026 (January–March).

Market demand in Q1 2026

Total consumer demand in the UK — measured by Blask Index across all tracked operators — reached 145.8 million for the quarter, up 7.1% from Q1 2025’s 136.1 million.

Compared to Q4 2025 (156.4 million), Q1 came in 6.8% lower. That seasonal dip is expected: Q4 carries the football season’s peak, Champions League group stages, and the pre-Christmas betting surge. Q1 historically runs cooler.

The 7.1% year-over-year growth is solid for a market of this size and maturity. The UK is one of Europe’s oldest licensed online gambling markets. Sustained single-digit annual demand growth here is not a weak signal — it’s what stable, regulated expansion looks like.

The number to remember: 23 more active brands in Q1 2026 (349) versus Q1 2025 (326), despite a tightening regulatory environment. New entrants kept coming in.

Track UK demand in real time at blask.com/market/united-kingdom.

Local vs international: how the market splits

The UK is one of the most tightly regulated iGaming markets in the world, and the demand split between locally licensed (Onshore) and international/offshore operators reflects that.

In Q1 2026, onshore brands held 97.0% of demand (Blask Index), with offshore accounting for the remaining 3.0% — up from 2.85% in Q1 2025. A small but consistent shift.

The revenue picture is more asymmetric:

| Q1 2025 | Q1 2026 | Change | |

|---|---|---|---|

| Blask Index — local share | 97.15% | 97.0% | –0.15 pp |

| Blask Index — international share | 2.85% | 3.0% | +0.15 pp |

| CEB — local (avg/month) | $829M (89.0%) | $927M (88.4%) | +11.7% |

| CEB — international (avg/month) | $103M (11.0%) | $121M (11.6%) | +18.0% |

Offshore operators hold 3% of demand but capture 11.6% of estimated revenue — a 3.87x efficiency premium over their locally licensed peers. That gap was 3.86x in Q1 2025. Essentially flat.

Offshore CEB grew faster (+18%) than offshore demand (+5.3%). The UK’s regulatory machine is running hard, but the offshore revenue premium hasn’t narrowed meaningfully. Each offshore demand unit still yields roughly four times more revenue than a local one. For the Gambling Commission’s affordability check rollout now underway, this ratio is worth watching — friction imposed on licensed operators without equivalent enforcement against offshore alternatives widens it further.

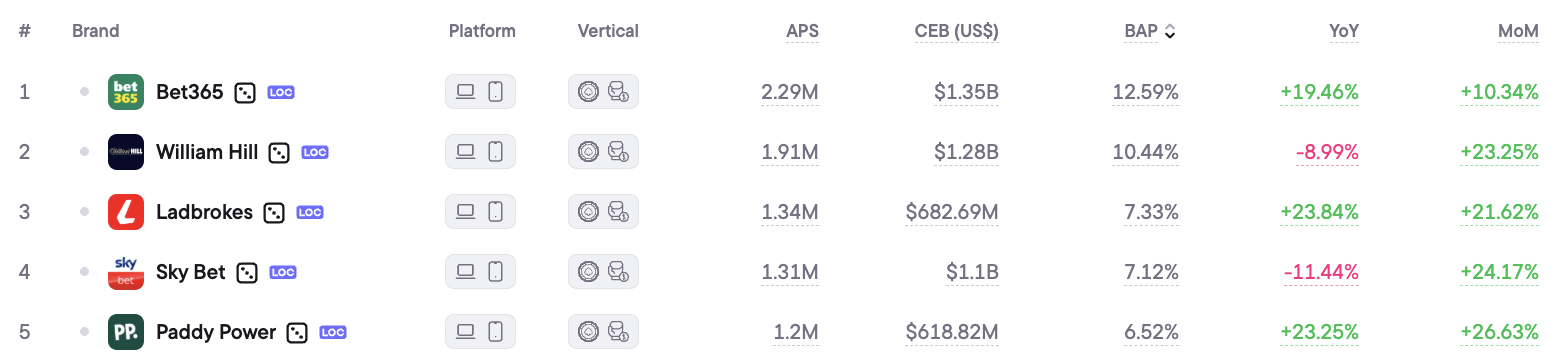

Top brands in Q1 2026

The top 10 ranking held the same names as Q1 2025. What shifted dramatically was who grew and who contracted.

| Brand | BAP share (approx.) | YoY demand change |

|---|---|---|

| Bet365 | ~11.0% | +19.5% ↑ |

| William Hill | ~8.5% | –9.0% ↓ |

| Ladbrokes | ~8.0% | +23.8% ↑ |

| Paddy Power | ~7.1% | +23.3% ↑ |

| Sky Bet | ~7.1% | –11.4% ↓ |

| Coral | ~7.2% | +21.7% ↑ |

| Betfred | ~4.9% | +30.1% ↑ |

| Gala Bingo | ~4.5% | +16.0% ↑ |

| Sky Vegas | ~2.6% | +16.4% ↑ |

| Betfair | ~2.4% | +11.9% ↑ |

BAP shares are approximated from Blask Index monthly data. YoY figures are Blask year-over-year demand change, Q1 2026 vs Q1 2025.

Bet365 had a strong quarter — up 19.5% YoY, extending its position as the UK’s most demanded iGaming brand. Its CEB for Q1 2026 reached $336M quarterly ($252M–$589M range), meaning Blask estimates the brand should generate between $84M and $196M per month based on its current market position. The APS benchmark puts Bet365 at 487K new customer acquisitions per quarter (366K–853K range).

William Hill was the quarter’s biggest loser in share terms. Demand fell 9% YoY — and compared to Q1 2025, when William Hill was closer to parity with Bet365 in demand, the gap has widened sharply. The brand’s BAP share dropped by close to 4 percentage points over the year. Parent company Evoke’s structural difficulties — betting shop closures, debt load, and strategic review — filtered directly into search demand metrics.

Ladbrokes and Coral (both Entain) grew 23.8% and 21.7% respectively. Together, Entain’s two UK brands added roughly 1.7 percentage points of combined demand share. It’s the clearest evidence in the data that Entain’s UK brand strategy is executing, particularly in a market where competitors are pulling back.

Betfred posted the strongest single-brand growth in the top 10 at +30.1%. The independent bookmaker — which Fred Done publicly warned would close shops if taxes rose — evidently redirected energy into online, where its demand growth outpaced every rival.

Sky Bet fell 11.4%. Within Flutter’s portfolio, Paddy Power took share that Sky Bet gave up — the two brands pulled in opposite directions, suggesting deliberate portfolio prioritisation rather than market-wide headwinds.

What drove the quarter

Evoke’s retreat reshaped William Hill’s market position. In January 2026, Evoke confirmed it would close a number of William Hill betting shops, citing the increase in online gaming duty announced in Chancellor Rachel Reeves’ Autumn Budget 2025. The closures weren’t just a retail story — the Evoke strategic review launched in December 2025 signalled a company in repositioning mode, and that uncertainty has a measurable effect on brand search demand. When operators pull back marketing and sponsorships, consumer interest follows.

Affordability checks began rolling out in Q1 2026. The Gambling Commission confirmed that its mandatory affordability check framework started deployment across all licensed online casino operators at the start of Q1 2026, following a 12-month pilot. The two-tier model — frictionless checks via credit reference agencies for the majority of players, enhanced documentary checks for higher spenders — introduces new friction at the acquisition stage. Early pilot data showed 95% of Stage 1 checks resolving without player disruption, but the industry’s concern about leakage to offshore markets is one reason the Offshore CEB share quietly grew this quarter.

Tax pressure reached operating decisions. In March 2026, Bet365 announced it would end sponsorships of the Craven Meeting and the July Festival at Newmarket, plus long-running partnerships at Haydock Park — citing the same tax and regulatory cost environment Evoke invoked for its shop closures. Even the market’s strongest operator is rerouting marketing spend ahead of April 2026’s Remote Gaming Duty increase to 40%.

Q1 2026 vs Q1 2025: year-over-year shift

| Metric | Q1 2025 | Q1 2026 | Change |

|---|---|---|---|

| Total Blask Index | 136.1M | 145.8M | +7.1% |

| Blask Index — local share | 97.15% | 97.0% | –0.15 pp |

| Blask Index — international share | 2.85% | 3.0% | +0.15 pp |

| Market leader | Bet365 | Bet365 | — |

| APS avg/month | 1.56M (1.15M–2.78M) | 1.66M (1.22M–2.97M) | +6.6% |

| CEB avg/month | $932M ($673M–$1.71B) | $1.05B ($755M–$1.92B) | +12.4% |

| CEB — local share | 89.0% | 88.4% | –0.6 pp |

| CEB — international share | 11.0% | 11.6% | +0.6 pp |

| Active brands | 326 | 349 | +23 |

The structural story in this table: revenue grew faster than demand (+12.4% vs +7.1%). That gap is either market monetisation improving, or the mix of active players shifting toward higher-value segments — or both. With 23 more active brands in Q1 2026, competition for the same consumer pool intensified, yet CEB expanded. The UK market is extracting more revenue per unit of consumer attention than it was a year ago.

What this means for operators

The UK in Q1 2026 is not a market where growth comes easy, but it is a market where it still comes. CEB growth of 12.4% in a heavily regulated, highly mature environment is meaningful. But the distribution of that growth is lopsided — it flowed to brands with strong positioning (Bet365, Entain), not to operators managing cost and regulatory pressure from a weaker foundation.

For any operator evaluating UK entry or expansion in 2026: the affordability check rollout creates short-term friction at acquisition, and the April 2026 Remote Gaming Duty increase will compress margins immediately. But the 349 active brands in this market and the +23 new entrants since Q1 2025 suggest operators are still coming in. The window for gaining share from retreating incumbents — particularly William Hill — is open but likely not for long.

Watch Sky Bet in Q2. A second consecutive quarter of double-digit demand decline from a top-5 brand would confirm Flutter’s UK portfolio strategy is more than a seasonal blip.

Conclusion

Q1 2026 confirmed the UK’s iGaming market is growing through regulatory pressure, not despite it — at least at the aggregate level. The 7% demand increase and 12% CEB expansion suggest the market is healthy. But health at the macro level is masking significant turbulence below. William Hill’s -9% and Sky Bet’s -11.4% are not small corrections. They represent operators ceding meaningful ground to rivals who are better positioned to absorb the costs of compliance and higher taxation.

The Q2 2026 question: does the April Remote Gaming Duty increase at 40% compress CEB across the board, or does demand resilience hold and the market simply redistribute margin from weaker to stronger operators?