- Updated:

- Published:

Brazil’s iGaming market overview: a new era of opportunity and risk

Blask’s lens on Latin America’s “Amazon of opportunity” for online gambling

Brazil’s digital gambling boom is no longer a niche story. By the spring of 2025, the country’s central bank estimated that online stakes had reached as much as 30 billion reais (about $5.1 billion) each month — several times higher than prior public estimates. Full-scale regulation took effect on January 1, 2025, but demand matured earlier: over the previous 12 months, Brazilians sent roughly 54 billion reais ($11.1 billion) to betting and online-casino sites.

The new regime launched a fresh cycle: away from “growth at any cost,” toward licensing, market share and sustainability. The stakes are high. Operators face a 12% tax on gross gaming revenue (with a move to lift it to 18% under discussion), players pay 15% on winnings, and the market itself is being pushed toward “white-market” growth and strict compliance.

Below is Blask’s deep dive: how the market works, who’s winning, where the risks lie, and which metrics actually capture the potential.

Macros and demand: a “digital powerhouse” with a taste for games

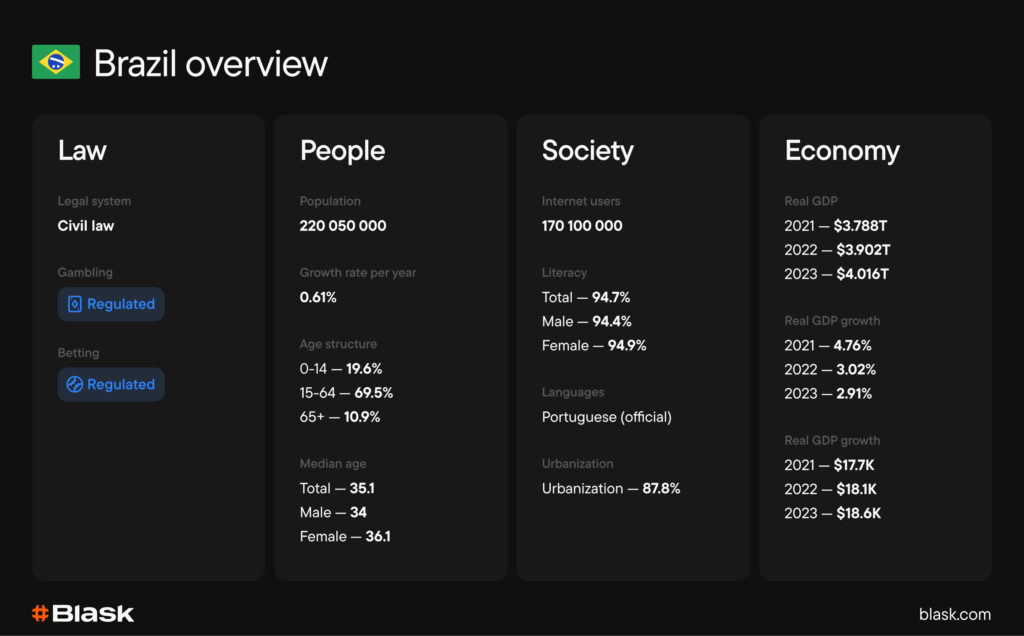

Brazil is Latin America’s largest economy, with a young, highly connected population. Penetration of mobile internet is among the region’s highest, making the country a natural home for iGaming.

In 2024–2025, Brazil emerged as a global leader by traffic to gambling sites, intensifying investor interest and speeding localization. Demand is not monolithic: industry surveys and operator disclosures show online casino steadily catching up with and in some segments surpassing sports in revenue, while “crash” games deliver outsized cash registers for certain local operators.

The rules of the game: Taxes, licensing, and the regulator’s opening moves

A brief timeline

- 2018 — The initial legal foundation for fixed-odds sports betting.

- December 2023 — Law No. 14.790 regulates online betting and casino; the Secretariat of Prizes and Bets (SPA/MF) is created.

- May 2024 — SPA/MF Ordinance No. 827 formalizes licensing requirements; the application window closes late-year.

Taxes and cost of entry

- GGR tax — 12% (a government proposal would raise this to 18% as part of a fiscal package).

- Player winnings — 15% tax.

- Concession fee — 30 million reais plus a 5 million reais reserve fund.

Licensing and enforcement

The application window closed with 113 companies — a robust show of interest in the “white” market. The Ministry of Finance has kept publishing and updating lists of authorized and suspended operators, including targeted blocks and temporary bans for violations. Meanwhile, the state began mass blocking of non-licensable domains—more than 2,000 sites—in 2024 and 2025 as the new regime came online.

How many operators are active now?

Blask identifies 501 active brands in Brazil; 136 already hold local licenses. By vertical: 388 offer combined betting + casino, 14 are sports-only, and 99 are casino-only.

Where Brazil ranks globally: CEB, APS and Latin America’s leader

Blask views markets through an off-ledger lens—potential revenue and statistically attainable acquisition at current brand strength.

For January–October 2025:

- CEB (avg) — Brazil ranks No. 3 worldwide at $5.07B, trailing only the United Kingdom and Turkey; Italy and Indonesia follow.

- APS (avg) — Brazil ranks No. 1 globally at 63.66M, ahead of Turkey, Bangladesh, South Africa and Vietnam.

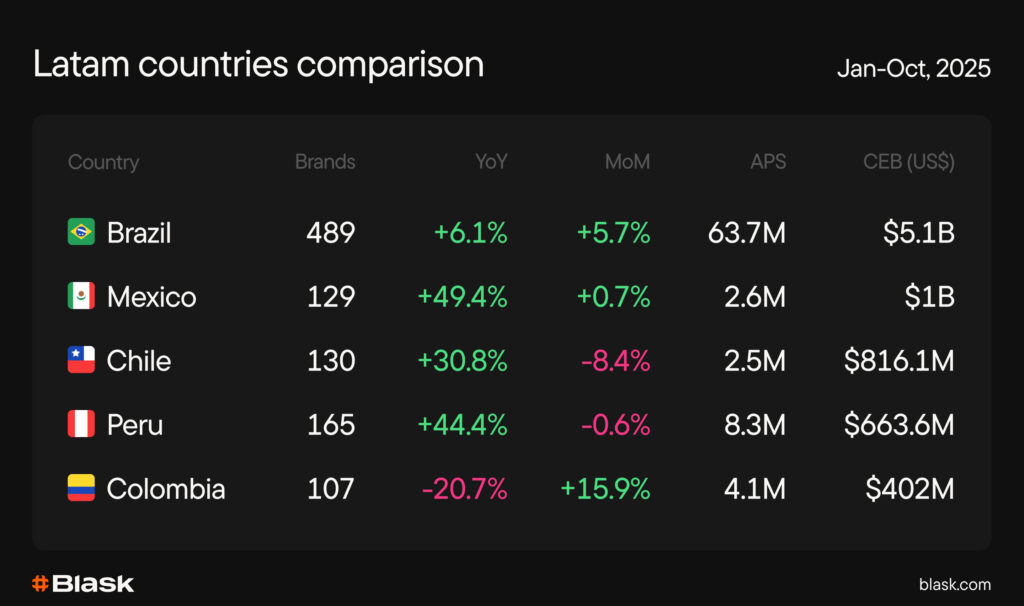

Inside LATAM, Brazil is a consistent No. 1; Mexico, Chile, Peru and Colombia follow.

Notes: Rankings reference 107 countries available in Blask as of Nov. 9.

Context from public sources reinforces the picture: lawmakers accelerated regulation, enforcement tightened, and authorities continued to refine the tax framework, with fiscal leaders signaling higher rates for the sector.

CEB and APS — what they mean

CEB (Competitive Earning Baseline)

An external, market-based revenue baseline in USD for a brand (or the country’s brand total): how much an operator should be earning at current brand strength and competitive intensity. It’s not your GGR ledger and not a guess; it’s a monthly interval forecast built from behavioral market signals (search interest, brand visibility), competitive anchors and a model that connects brand equity to financial outcomes. Leaders see a range (min/base–avg–max), not a point.

APS (Acquisition Power Score)

An external, market-based baseline for new-customer acquisition (for a brand or country total): how many new users an operator should be bringing in, given brand strength and competition. It’s not your FTD/registration tally; it’s a monthly interval forecast built from external behavioral signals and competitive anchors.

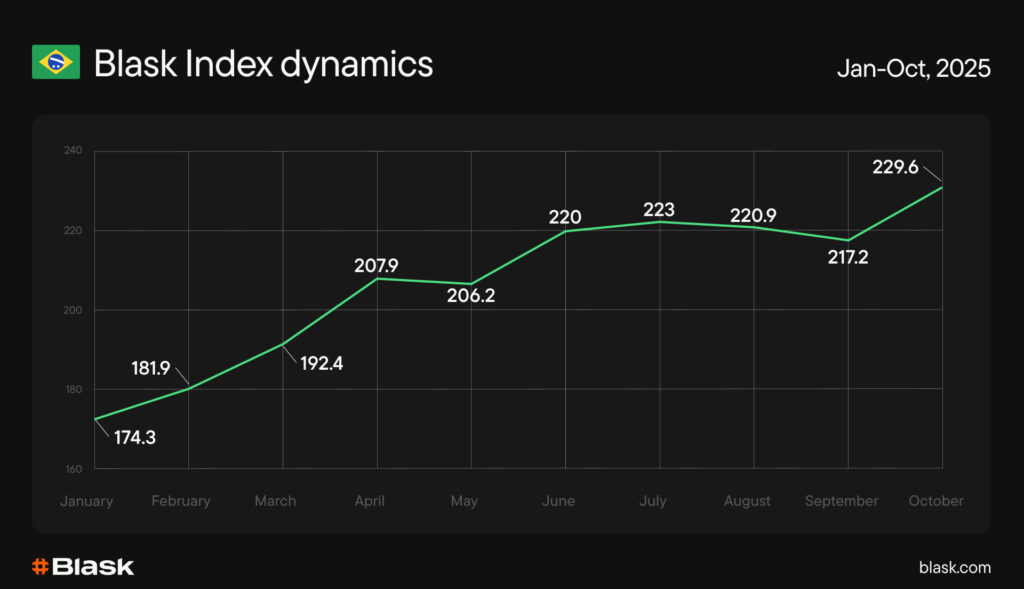

Blask Index: The market has snapped back

After a January dip around the regulatory launch, the market rebounded quickly and resumed an upward line by autumn. On Blask’s 2025 chart: 174.3M in January → 229.6M in October (about +32% over ten months), with a routine seasonal soft patch in Q1 and a rotation higher thereafter. The headline: demand returned and held into year-end.

2025 by month (Blask Index, M):

Jan 174.3 • Feb 181.9 • Mar 192.4 • Apr 207.9 • May 206.2 • Jun 220.0 • Jul 223.0 • Aug 220.9 • Sep 217.2 • Oct 229.6

At the same time, the longer series shows a touch lower plateau than the hottest stretches of 2023–2024. In other words: the market has normalized at a higher, regulated base, not overheated—consistent with stricter rules, heavier taxes and more disciplined promotional spend.

Read also: iGaming Brazil 2026: Behind the Scenes of Top LatAm Market

Market structure and share shifts: The fight for leadership

Of the 501 active operators (with 136 licensed locally), only the top 15 hold more than 1% BAP each. Consolidation is visible in 2025: in January, brands outside the top ten together accounted for nearly 11%; by October their combined BAP had slipped to 6.44%.

Leader movements in 2025 (Blask BAP):

- Betano widened its lead: 17.28% → 25.52% (Jan → Oct).

- Bet365 gained: 8.49% → 12.63%.

- Sportingbet held a steady top-three slot (~8–8.5%).

- Superbet climbed (4.28% → 6.62%).

- Esportes da Sorte drifted lower into year-end.

Global heavyweights are stepping in through partnerships and M&A. The regulator continues to refresh its “white list” as checks are completed, while SPA/MF suspends those out of compliance. This is the “year of consolidation”: thin-margin and gray-market models exit; capitalized, compliant brands gain share.

Public reporting also points to aggressive go-to-market post-launch—BetMGM, for instance, flagged Brazil as a priority while accepting heavier marketing losses to build share.

Read also: Brazil’s betting seasons, explained

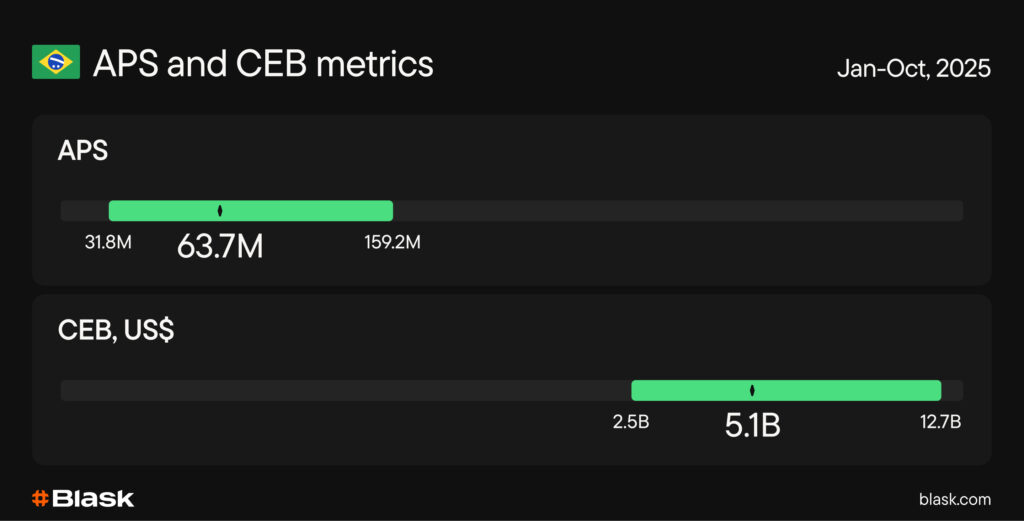

APS and CEB in 2025: Momentum and potential

Across January–October 2025, Blask panels show:

- APS: Min 31.83M / Avg 63.66M / Max 159.15M

- CEB: Min $2.53B / Avg $5.07B / Max $12.66B

The year opened from a modest base, pressured by the regulatory reset in January–February. Spring brought a measured recovery in interest and marketing activity. Summer saw a steady climb on the sports calendar and as operators adapted to new rules. A brief late-summer air pocket reflected cooler promo and channel rebalancing. By October, both acquisition (APS) and potential revenue (CEB) were back on an upward track.

On a trailing basis, Blask Index is up +6.11% year-over-year, consistent with the narrative of “low start after regulation, recovery into autumn.” The practical read-through: at a portfolio level, the average ability to acquire (APS) and the market revenue baseline (CEB) are growing again. If Blask Index keeps rising, the financial baselines typically follow with a short lag.

Seasonality and the weekly “prime time”

Brazilian iGaming breathes seasonally. The attention peak is December (230.2M on Blask panels), followed by October, with July rounding out the top three.

Weekly, the country has a clear prime time: Saturday 05:00 UTC. In Brazilian time zones, that is the early-morning window when live action and long sessions reliably lift conversion:

- BRT (UTC–3, ~93% of the population): 02:00 Saturday

- AMT (UTC–4): 01:00 Saturday

- ACT (UTC–5): 00:00 Saturday

- FNT (UTC–2, Fernando de Noronha): 03:00 Saturday

Operator playbook: sprint toward December, sustain longer campaigns through October, and lean into the Saturday pre-dawn slots—a proven sweet spot for deposits, live support and high-intent promos.

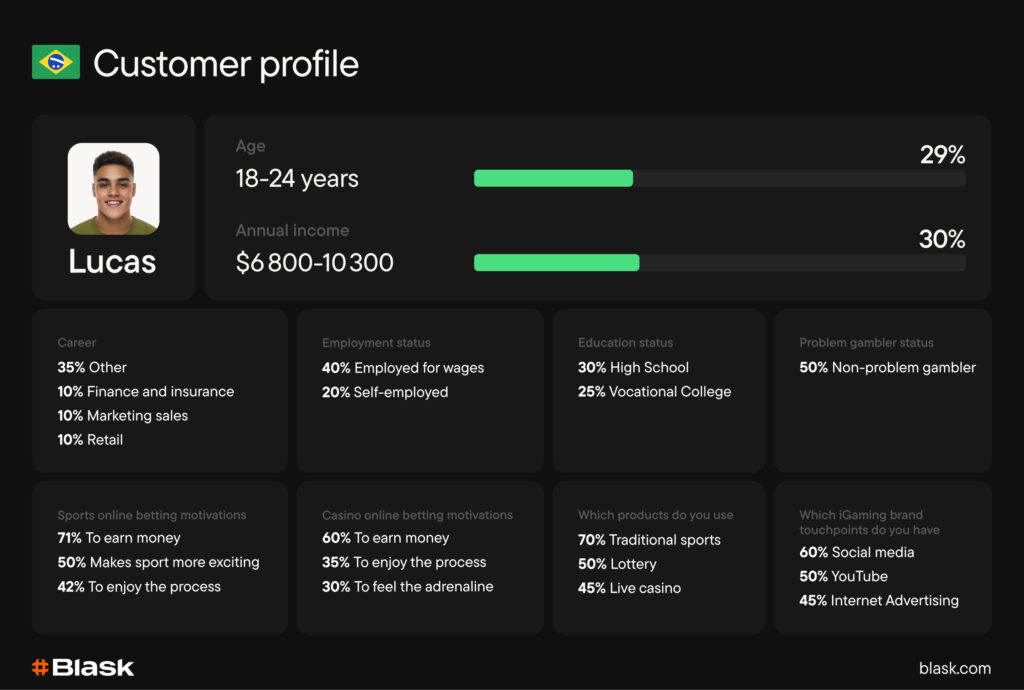

The Brazilian consumer: Youth, income and motivation

The iGaming customer here is young and pragmatically value-seeking. Blask’s Customer Profile shows:

- Age: Core 18–24 (29%).

- Income: 30% earn $6,800–$10,300 annually.

- Education & employment: 30% high-school, 25% vocational/technical; 40% employed for wages, 20% self-employed.

- Motivation — Sports: “to make money” (71%), “make sports more exciting” (50%), “enjoy the process” (42%).

- Motivation — Casino: “to make money” (60%), “process” (35%), “adrenaline” (30%).

- Products used: traditional sports (70%), lottery (50%), live casino (45%).

- Touchpoints: social media (60%), YouTube (50%), online advertising (45%).

- Responsible gambling: 50% non-problem gamblers, but public-health signals warrant attention—authorities have tied the boom to pressure on household finances and have even considered restricting welfare-funded betting.

What to do with this: design onboarding and funnels for a mobile-first, night-and-weekend audience that pairs “adrenaline” with “a chance to win.” Keep limits visible, embed RG by design, and tune media to social + YouTube.

Navigating Brazil’s “golden age” of iGaming

The market is back — this time as a grown-up.

Demand recovered from the January reset and reached a new local high by autumn 2025. The lesson: clear rules don’t kill interest; they trim noise and channel the industry into managed growth.

Appetite is real; the bar to entry is higher.

The licensing window drew 113 applicants—more than many expected—showing that “white-market” demand exists despite fees and technical hurdles. Translation: capital and compliance are now core competencies.

Taxes are the price of predictability.

Heavier fiscal take is the trade-off for a stable regime. Strong brands and patient capital will stay; thin, promotion-only models will wash out.

Competition will get heavyweight.

Top brands are entrenching via partnerships and deals. Expect share reallocation in 2025–2026. Without scale, tech, localization and payments access, operators will struggle.

Brazil is a global asset—with regulated risk.

Systematic pressure on the gray segment (thousands of blocks, tighter ad/KYC rules) lowers regulatory risk for licensees while raising the bar for “quick-hit” tactics

What to do now

- Investors: back licensed local leaders and multinationals with a record of operating under heavy regulation. Expect synergies and scale efficiencies.

- Operators: rebuild unit economics for the new normal (taxes/fees/compliance). Prioritize retention and product differentiation (fast formats, local payments, weekend & late-night live). Marketing: less spray, more precision—with robust RG. (Seasonal peaks: December > October > July; weekly prime time: early Saturday morning local.)

- Affiliates/partners: the market is getting top-heavy. The long tail will keep losing share; focus on the top 10–15 for better yield.

Bottom line: Brazil has passed through regulatory turbulence and returned to growth. Audience interest has normalized at a higher base, licensing has clarified the rules, and momentum is shifting toward capitalized, tech-forward, compliant operators. What comes next is gradual institutionalization: less noise, more predictability — and a higher cost of mistakes. That’s the environment where strong players win.

Blask metrics, in one page

CEB (Competitive Earning Baseline) — an external, interval revenue benchmark (min–avg–max) in USD for a brand or country: what an operator should be earning given brand strength and today’s competition. Updated monthly.

APS (Acquisition Power Score) — an external, interval new-customer benchmark (min–avg–max): how many new users an operator should be acquiring at current brand strength and competitive intensity. Updated monthly.

Blask Index — a “stock-market index” of iGaming interest: total demand and how it’s shared among brands, built on the Share-of-Search relationship and cleansed for cross-country, cross-period comparisons. Updated hourly.BAP (Brand’s Accumulated Power) — a percentage measure of brand strength as a share of category power, stable across swings in absolute market size, designed for cross-country and cross-period comparisons. Updated hourly.