- Updated:

- Published:

iGaming market growth by region: who runs the table in 2026

Online gambling’s center of gravity is shifting. The headline figures still belong to Europe and North America, but the velocity — the places where something genuinely new is happening — is elsewhere.

The global online gambling industry crossed €90.5 billion in revenue in 2025, with a projected compound annual growth rate of 10.5% through 2030. More than 450 million players participated in some form of digital wagering last year. And yet the most instructive story of 2025 was not the total. It was the divergence — a pattern that now defines the broader conversation around iGaming industry trends 2026.

iGaming market growth by region no longer follows a single curve. It follows five or six distinct ones — shaped by regulation, mobile infrastructure, currency dynamics, and the competitive strategies of a handful of locally dominant brands. Here is what those curves looked like in 2025, and what they telegraph about 2026.

Europe: recovery beneath the compliance ceiling

Any credible European iGaming market outlook 2026 has to start with a paradox: Europe remains the world’s most mature online gambling region, yet some of its most important markets are still growing through compliance pressure rather than despite it.

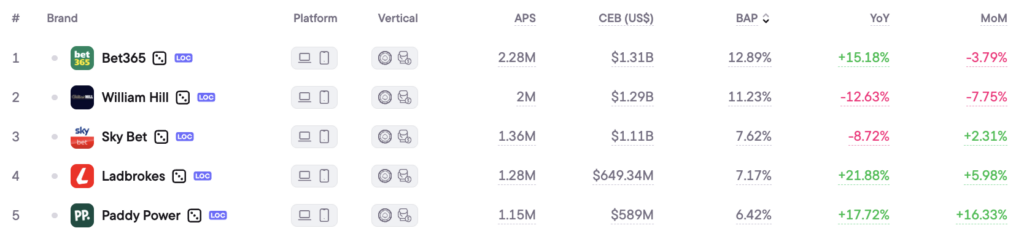

Europe generated an estimated €51 billion in online gross gaming revenue in 2025. Within that aggregate, the United Kingdom delivered a standout story of institutional resilience.

According to Blask, the UK market closed 2025 with 334 active brands, total Acquisition Power Score (APS) of 19.85M new player acquisitions, and Competitive Earning Baseline (CEB) of $11.5B — a 9.8% increase YoY.

Bet365, the market’s most closely watched brand, recorded a +15.18% YoY Blask Index gain in 2025 — a notable reversal after an 18.7% decline in 2024 . What looked like structural decay in 2024 appears, in retrospect, to have been a compliance-driven shakeout that strengthened the market’s dominant incumbents.

Germany is the year’s quieter surprise. Blask data shows German market APS surging from 5.36M in 2024 to 8.39M in 2025 — a 56.5% YoY increase — with CEB rising to $3.04B.

The 2021 Interstate Treaty, long criticized for strangling demand, appears to have created a different outcome: it concentrated licensed-market search behavior around a smaller number of regulated operators, amplifying their signal volume rather than suppressing it.

North America: the $10 billion threshold

The United States broke a symbolic barrier in 2025. According to the American Gaming Association, U.S. iGaming revenue reached $10.74 billion for the full year — a 27.6% increase over 2024 and the first time the category has crossed the $10 billion threshold. Sports betting added another $16.96 billion, up 22.8%. Total commercial gaming revenue landed at $78.72 billion, a 9.2% gain.

Blask’s full-market picture deepens the context. Total U.S. CEB across all 365 active brands reached $80.6 billion in 2025, with APS at 7.46 million.

The market leader by Blask Index remains Bovada — an offshore, unregulated operator — with a +10.78% YoY gain and estimated CEB of $9.23 billion. The gap between the regulated iGaming sector’s $10.74 billion and the total Blask-modeled CEB of $80.6 billion is not an error. It is the measure of how much U.S. demand still flows outside licensed channels.

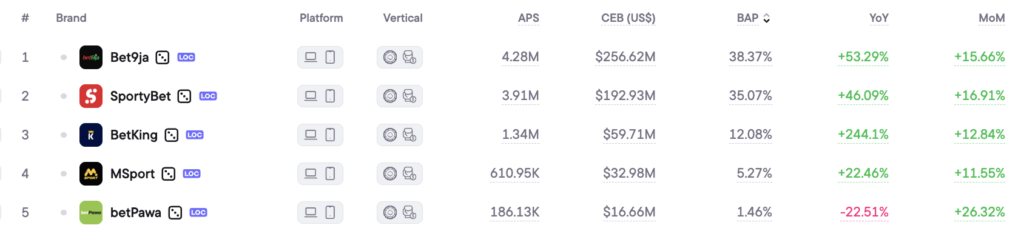

Africa: acceleration, not a forecast

Anyone asking which iGaming markets are growing fastest should be looking closely at Sub-Saharan Africa. In 2024, the region generated a great deal of commentary about its future potential. In 2025, it began producing numbers that made even the optimistic version of that commentary look conservative.

Nigeria’s total Blask APS reached 11.59 million in 2025 — a 44.3% increase from 2024’s 8.03 million — while market CEB climbed to $633.6 million, up 26.7%.

Bet9ja, the market’s dominant brand, posted a +53.29% year-over-year Blask Index gain, with APS approaching 4.3 million on its own. SportyBet, its closest competitor, added 3.9 million APS in the same period.

The revenue-per-acquisition ratio remains far below European or North American benchmarks — Nigeria’s $633 million CEB across 11.6 million APS implies revenue well under $60 per acquired player. But that number is a function of purchasing power and payment infrastructure, both of which are improving. The player volume is already there.

Latin America: the paradox of regulated disruption

Brazil entered 2025 as the hemisphere’s most anticipated regulated market. Federal licensing, which came into force at the start of the year, was expected to unlock a wave of formalized revenue.

Blask data shows a more complicated picture. Total Brazilian APS remained stable at 79.2 million in 2025 — essentially flat against 2024’s 76.8 million. But CEB fell from $7.2 billion to $5.08 billion. More players, less modeled revenue.

The likely mechanism: federal licensing required operators to restructure affiliate agreements, payment flows, and bonus structures, compressing effective yield per player in the short term while the regulated ecosystem recalibrated. Brazil had 17.7 million active bettors in the first half of 2025 alone. The volume is not in question. The monetization structure is still being built.

Read also: Online gambling market forecast 2026 — what the numbers actually say

Who to watch?

The data from 2025 suggests that most consequential movements will unfold in four top iGaming markets 2026:

- Germany is the regulated market with the clearest momentum. A 56% APS surge in a single year, driven by structural consolidation rather than population growth or new device penetration, signals that licensed operators are systematically capturing search demand that was previously absorbed by offshore alternatives.

- Nigeria is the emerging market running out of patience for its own “emerging” label. Bet9ja’s 53% Blask Index growth is not noise — it reflects genuine demand acceleration, driven by mobile penetration and sports culture that was already mature before formal regulation arrived.

- Brazil’s regulated shakeout will produce its first wave of clear winners in 2026, as operators who absorbed 2025’s licensing costs start to convert their compliance infrastructure into competitive moats. Italy faces a similar dynamic: its 2026 licensing cycle effectively resets competitive positioning in one of Europe’s most valuable markets.

- The United States will cross another threshold. Seven iGaming states generated $10.74 billion in 2025 across a fraction of the addressable population. As additional states cross the legalization threshold — and as regulated operators tighten their grip on demand that currently flows offshore — the distance between Blask’s $80.6 billion total CEB estimate and the regulated sector’s reported revenue will narrow in ways that will reshape the competitive landscape significantly.

The global iGaming market is expected to grow 8–10% year-over-year in 2026, with mobile accounting for more than 70% of all online gambling sessions. The structural opportunity is not in question. What 2025 established — definitively — is that the returns accrue to operators who understand the specific regulatory and cultural grammar of each region, not to those applying a single global playbook.