- Updated:

- Published:

The top iGaming markets in 2026: what the data actually ranks

Turkey generated an estimated $8.9B in iGaming revenue in 2025, according to Blask. Every brand that captured that revenue operated without a local license.

That is the defining fact about any ranking of the top iGaming markets in 2026: the largest revenue pools and the most tightly regulated markets are not the same list. Revenue follows demand. Demand follows players. Players do not always follow the law.

The 20 countries below represent the full Blask top-20 by Competitive Earning Baseline (CEB) for the 2025 calendar year — Blask’s modeled revenue estimate derived from search demand signals. Acquisition Power Score (APS) runs alongside it: the estimated number of new players a market generates per year. The two metrics rarely tell the same story.

Read also: iGaming trends 2026 from Blask experts

How Blask ranks the Top iGaming markets for 2026

| # | Country | CEB (est., USD) | APS (est.) | Brands | YoY |

|---|---|---|---|---|---|

| 1 | United States | $80.7B | N/A* | 364 | +0.7% |

| 2 | United Kingdom | $11.5B | 19.85M | 334 | +12.4% |

| 3 | Canada | $9.7B | N/A* | 246 | +30.5% |

| 4 | Turkey | $8.9B | 27.68M | 237 | −24.2% |

| 5 | Brazil | $6.3B | 79.23M | 518 | +5.5% |

| 6 | Italy | $6.0B | 13.51M | 202 | +10.9% |

| 7 | Australia | $5.8B | N/A* | 313 | +14.4% |

| 8 | India | $5.2B | 19.14M | 462 | +0.6% |

| 9 | Indonesia | $3.9B | 3.47M | 79 | +3.9% |

| 10 | Philippines | $3.7B | 14.44M | 212 | +133.4% |

Source: Blask, Jan–Dec 2025. CEB and APS are modeled estimates with min–max confidence intervals; table shows point estimates. YoY = Blask Index change. US, Canada, and Australia APS figures are available at state/province level only — national-level APS is not reported by Blask for these geographies.

The table produces three distinct stories: a small group of regulated markets with outsized revenue density (US, UK, Canada); a large group of unregulated or partially regulated markets with outsized acquisition scale (Turkey, Brazil, Vietnam, Indonesia); and two outliers moving in opposite directions — the Philippines expanding at triple-digit speed, Japan contracting at almost the same rate.

Check the iGaming and Gambling market worldwide power ranking, updated every month

United States: revenue that dwarfs everything else

The U.S. aggregate CEB of $80.7B sits so far above every other country in this dataset that direct comparison loses meaning. The second-ranked market, the United Kingdom, generates roughly one-seventh as much.

What that figure reflects is not uniform licensed demand. Blask identifies 364 active brands in 2025, a mix of licensed sportsbooks, offshore casino operators, and tribal gaming. Blask Index grew just 0.7% YoY — nearly flat for a market of this size.

Bovada leads by Blask Index and posted 10.8% YoY growth. BetOnline grew faster at 28.9%. DraftKings and FanDuel lead the licensed operators by CEB, at an estimated $6.9B and $7.5B respectively, while their index growth was flat in the same period. The gap between offshore momentum and licensed revenue is one of the more persistent structural features of the American market.

United Kingdom and Canada: regulated depth

Any serious European iGaming market outlook 2026 has to begin with the UK, where scale, maturity, and monetization remain difficult to match. The country’s $11.5B CEB against 19.85M APS reflects a market where revenue per new player is still among the highest globally. Blask Index grew 12.4% YoY — faster than the U.S., despite representing only a fraction of its total size.

Bet365 leads with 15.2% index growth. William Hill, the historical second brand, fell 12.6%. That decline does not register as a crisis in one quarter; it registers as a structural shift over time. Ladbrokes holds third.

Canada at $9.7B CEB is the third-largest market by revenue in this dataset, with 30.5% YoY growth — the highest rate among the top five by CEB. Ontario’s regulated framework, which opened in 2022, continues to consolidate demand toward licensed operators.

Turkey: the $8.9B market that is shrinking

Turkey’s $8.9B makes it the fourth-largest iGaming market in the world by modeled revenue. The Turkish government bans online gambling entirely. There is no licensed framework, no regulated operator, and no legal path to market entry.

The Blask Index fell 24.2% YoY. Merit King leads by Blask Index but declined 38% in the same period. Nesine — a licensed sports-betting brand, the only one in the ranking — fell 13.8 percent. The contraction is broad.

What the numbers describe is a market under sustained enforcement pressure. The offshore brands that built the Turkish demand signal are losing ground as payment blocking and domain seizures compound. The market is large. It is also getting smaller every year.

Loss aversion shapes operator behavior here in a predictable way: businesses that built CEB projections on Turkish offshore numbers in 2023 are holding those positions longer than the data warrants. When an APS-heavy market reverses this sharply, the rational response is to reweight — not to wait for recovery.

Brazil: 79M players, one-thirteenth the U.S. revenue

Brazil’s 79.23M APS is the largest acquisition signal in this dataset by a significant margin. At $6.3B CEB, it ranks fifth by revenue.

The ratio is instructive. A market with roughly ten times the U.S. acquisition volume earns one-thirteenth the U.S. revenue. That gap reflects currency, formal licensing lag, and the proportion of demand that flows through brands with no local payment integration.

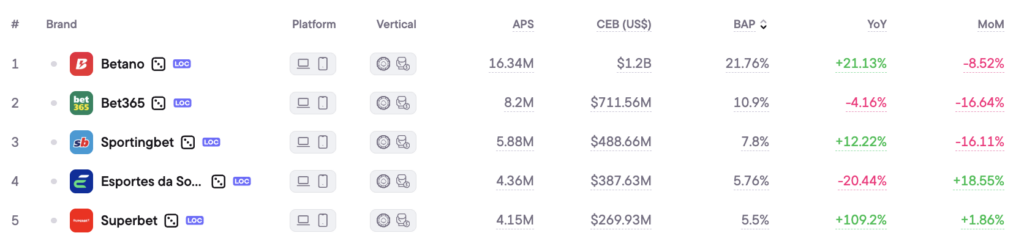

Betano leads by both APS and Blask Index, with 21.1% YoY growth. Bet365, second, fell 4.2%. The overall market index grew just 5.5% — slow for a market at this acquisition scale, and likely a sign of post-regulation normalization after Brazil’s formal licensing framework became operational in 2025.

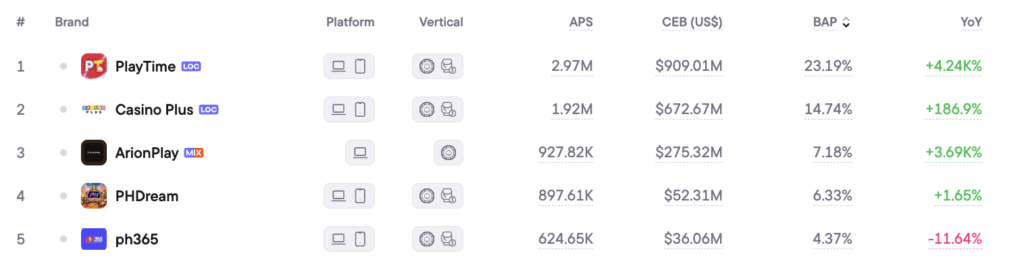

The Philippines: the fastest-growing market in the Top 10

The Philippines grew 133.4% by Blask Index YoY — the highest rate in the top 10 by a substantial margin, making it one of the fastest growing online casino markets in the current global dataset.

PlayTime, the leading brand, grew 4,237% YoY That figure is not a typo. Casino Plus, second, grew 186.9%. ArionPlay, launched in June 2024, already holds third in the market.

The growth dynamic here is structural, not cyclical. PAGCOR, the Philippines gaming regulator, has aggressively consolidated the offshore remote gaming operator (POGO) sector since 2024 while simultaneously licensing new domestic operators.

The brands gaining share are largely compliant with that framework. The Blask Index growth reflects genuine demand expansion, not a reshuffling of existing players between operators.

At $3.7B CEB and 14.44M APS, the Philippines is now a mid-tier market by scale. At 133.4% growth, it is the most significant trajectory story in the dataset.

Japan: high revenue, collapsing demand

Japan generated an estimated $3.4B CEB in 2025 against 618,000 APS. The ratio of revenue to acquisition is the highest in the top 20 by a wide margin — each modeled new player corresponds to roughly $5,500 in estimated annual revenue.

The market is also falling off a cliff. The Blask Index declined 45.8% YoY. Stake, the leading brand, fell 24.7%. Yuugado fell 24.3%. Every top brand declined.

Japan has no legal online gambling framework other than state-operated lottery and horse racing. The offshore brands in this ranking are operating into a market that is actively restricting payment access and advertising.

The CEB number reflects historical depth; the YoY number reflects the direction of travel.

Germany: the regulated rebound

Germany’s Blask Index grew 58.7% YoY — the fastest growth rate among established regulated European markets in this dataset.

That expansion follows the phased implementation of the Glücksspielstaatsvertrag 2021 framework, which legalized online slots for the first time and set licensing standards. Three years in, the market is still absorbing the compliance-driven consolidation that followed.

Tipico, the leading brand, grew 2.6% by Blask Index — modest for the market leader. NV Casino, launched in November 2024, already holds second place by APS, an indication of how much unmet demand persists even in a country with 348 active brands.

At $3.0B CEB and 8.39M APS, Germany sits in the middle of the European field — considerably below Italy ($6.0B) but growing faster than any comparable market in the region.

Read also: Germany iGaming market 2026: $3B, 347 brands, and a regulatory war nobody is winning

Africa and Southeast Asia: the acquisition tier

For anyone asking which iGaming markets are growing fastest in 2026, Africa and Southeast Asia offer some of the clearest answers — not always in terms of current monetization, but in sheer acquisition potential.

Three markets in the top 20 combine high APS with sub-$3 billion CEB in ways that suggest structural upside rather than fully matured revenue depth.

South Africa posts 24.0M APS against $3.0B CEB, with 15.4 percent index growth. Betway leads with 27.1% YoY growth and holds roughly 46% of the market’s APS. Hollywoodbets, the domestic incumbent, fell 4.3%. The competitive dynamics are shifting toward international operators.

Vietnam posts 21.98M APS against $3.0B CEB — nearly identical revenue to South Africa with higher acquisition volume. The market is fully unregulated. Online gambling is prohibited; the brands in the ranking are offshore. That structure limits monetization and exposes the market to the same enforcement risk that is contracting Turkey.

Indonesia at $3.9B CEB with only 3.47M APS and 79 brands is the inverse: high revenue concentration across a very small licensed competitive set. The market is also fully unregulated; Indonesia’s prohibitions on online gambling are among the most strictly enforced in Southeast Asia.

Growth by region

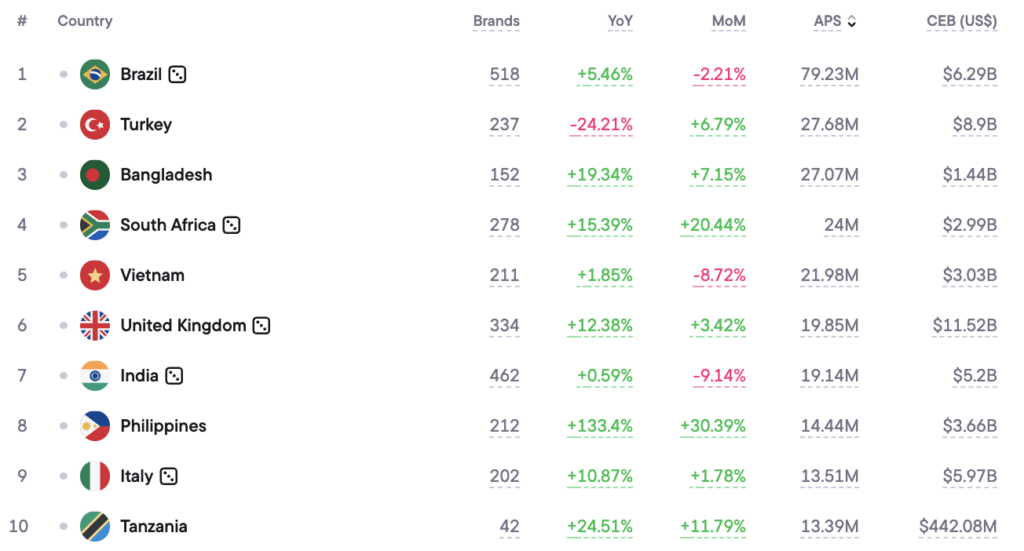

The table at the top of this article is sorted by CEB. Sort by APS instead and the ranking changes completely: Brazil moves to first, South Africa and Vietnam enter the top five, Turkey holds its position, the U.S. disappears from the top ten entirely.

Neither sort is wrong. They answer different questions. CEB answers where modeled revenue is concentrated. APS answers where player demand is concentrated. The two diverge most sharply in unregulated markets — where players exist but monetization infrastructure does not — and in high-income regulated markets, where the opposite is true.

The markets gaining ground in both dimensions simultaneously — the UK, Canada, the Philippines, South Africa — are the ones where the regulatory settlement and the demand signal are moving in the same direction.

Regulators set the calendar. Blask models the demand. They are not the same source.